The electrification theme in 4 charts

Platinum, palladium, copper, uranium. Four key metals in the electrification of everything. As highlighted by @DimitryFarberov on X, their quarterly charts are starting to come alive. • Copper just broke out of a 15+ year base • Platinum finally cleared its downtrend • Palladium trying to bottom at major support • Uranium still in its handle, consolidating after a huge move Different charts, same theme.

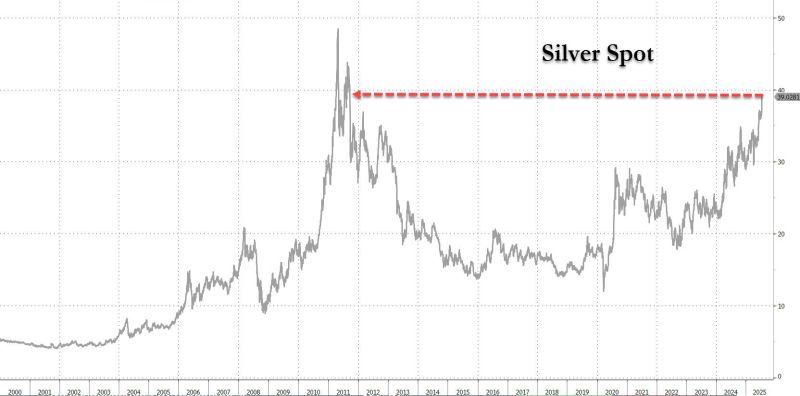

Silver surges above $39 for the first time since the first US downgrade in Aug 2011

Source: zerohedge

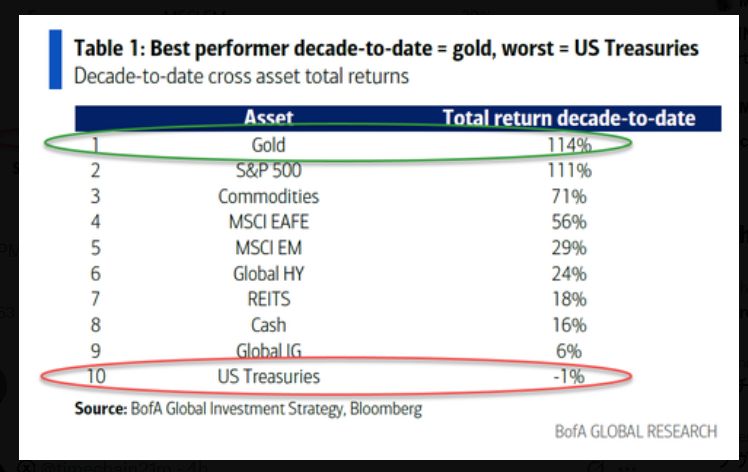

BofA forgot to include bitcoin in their "best performing asset of the decade" table.

Bitcoin $BTC is up almost 1600% this decade 📈📈

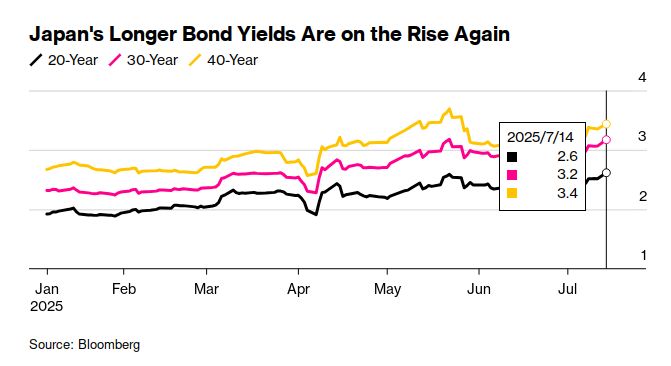

Yield on Japanese government hashtag#bonds are back to the highs they reached in May.

Japan was always held up by the MMT (Modern Monetary Theory) crowd as an example for how debt doesn't matter because governments can always cap yields. That view needs to be retired along with MMT. Fiscal space seems to be finite. Not infinite. Source: Robin Brooks, Bloomberg

Federal Reserve just issued a joint statement with 2 regulators confirming that banks can offer Bitcoin and crypto custody.

Source: Bitcoin archive

Oops... Jim Cramer just coined a new acronym PARC

Palantir $PLTR AppLovin $APP Robinhood $HOOD Coinbase $COIN Is it the end of the party for these 4 high flying stocks? Source: Evan on X

Gold now outperforming the U.S. Stock Market (dividends included) over the last 25 years.

Incredible! Source: Barchart

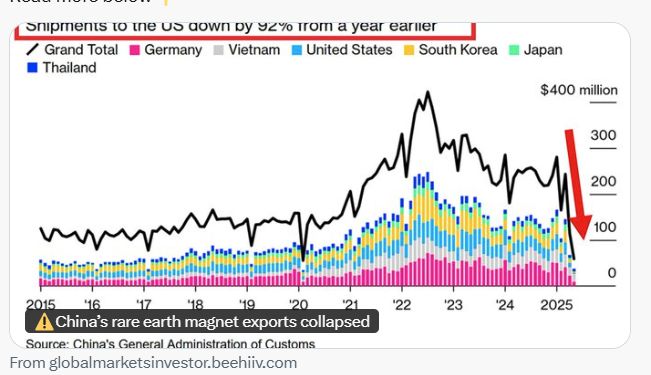

🚨China’s rare earth magnet exports COLLAPSED

Total shipments FELL 76% YoY in May, to 1,238 tons, the least since February 2020. Exports to the US FELL 92% YoY to 46 tons, and LESS than 1/10 of what was recorded in March. Source: Global Markets Investors