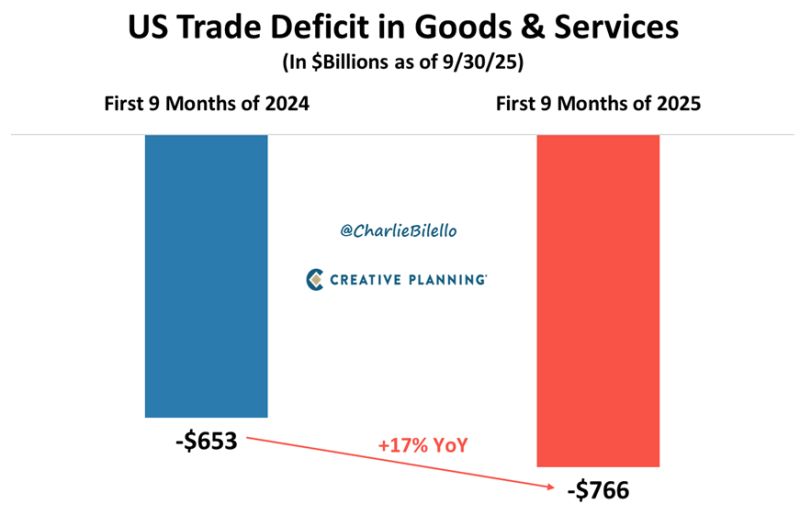

US Trade Deficit in Goods & Services...

First 9 months of 2024: –$653 billion deficit. First 9 months of 2025: –$766 billion deficit. +17% YoY 🚨 Record high. Source: Charlie Bilello

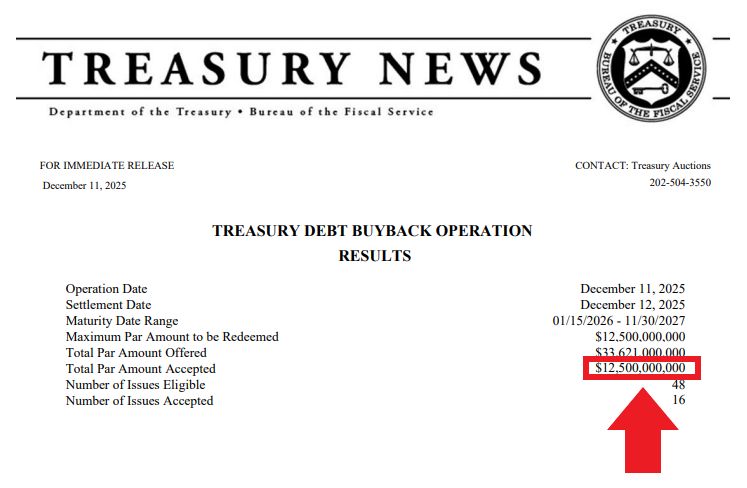

JUST IN 🚨: U.S. Treasury just bought back $12.5 billion of their own debt, equaling their largest buyback in history (which happened last week) 🤯👀

Source: Barchart

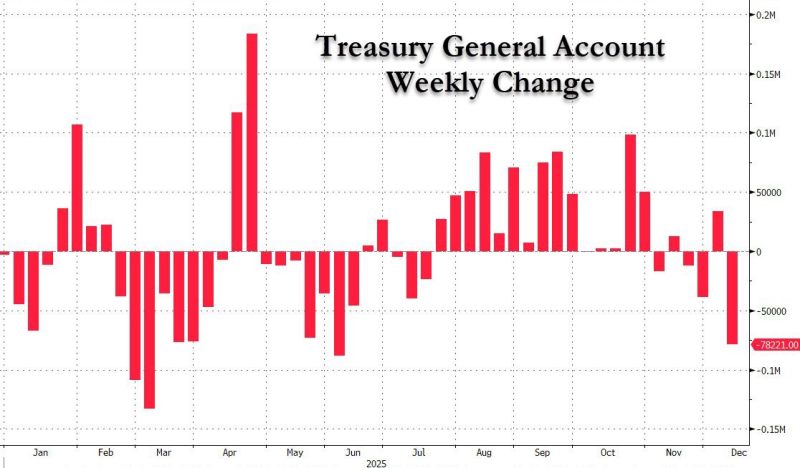

1) Repo fixed ✔️ : Fed launches Reserve Management Purchases (liquidity injections)

2) Treasury cash flood begins ✔️ : TGA balance down $78BN in one week (3rd biggest liquidity injection of 2025) 3) Meltup ✔️: stocks close at all time high Source: zerohedge

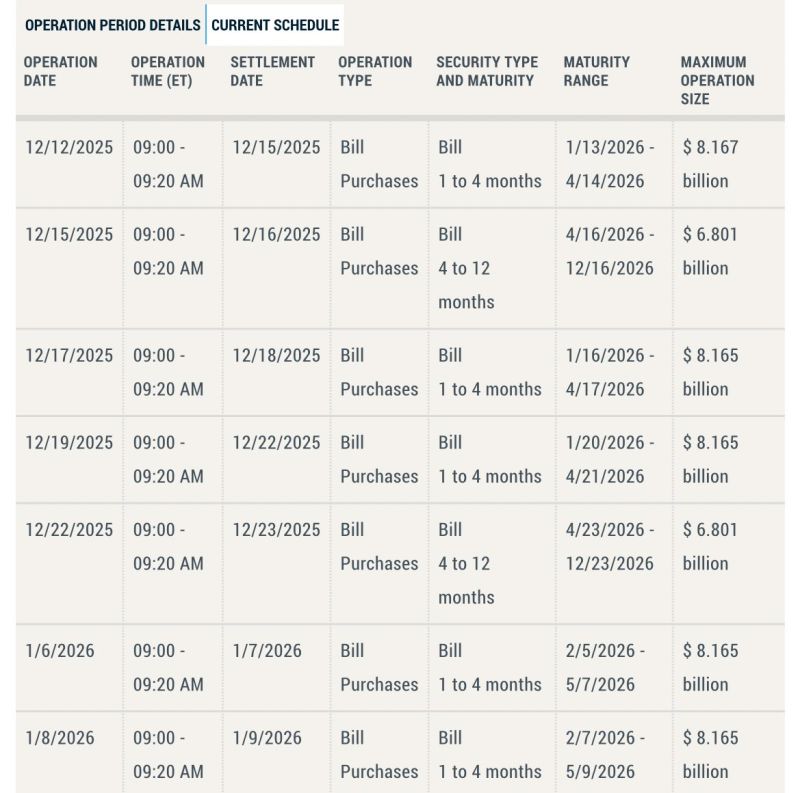

Here it is…

Fed’s first month of T-Bill purchases. $40 BILLION over the next month. Starts today at 9am.

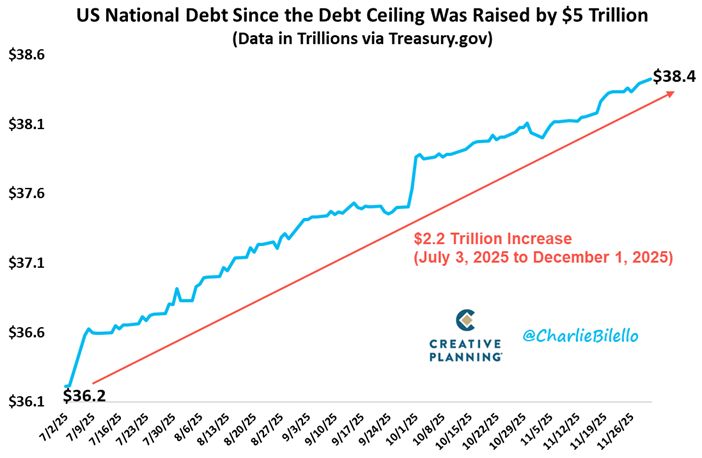

The US National Debt has now increased by $2.2 trillion since the Debt Ceiling was raised back in July.

Source: Charlie Bilello

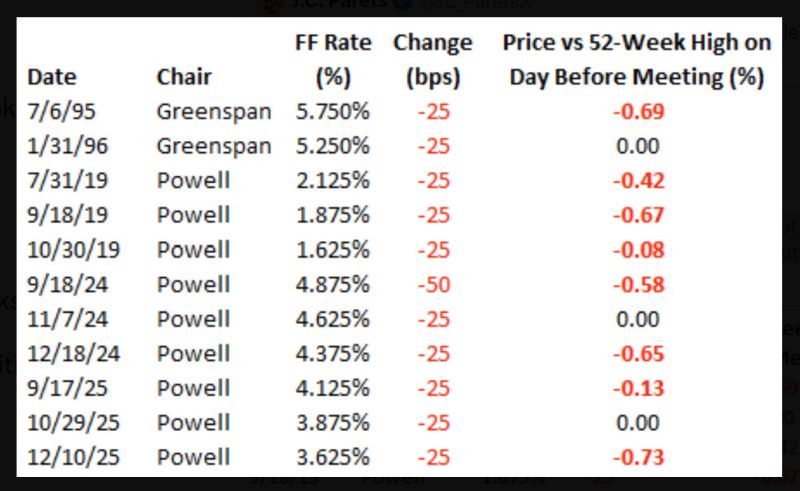

Powell the Provider.

Today was the 11th time since 1994 that the Federal Reserve cut rates when the S&P 500 was within 1% of a 52-week high. Nine of those cuts have occurred under Powell. Source: Bespoke @bespokeinvest

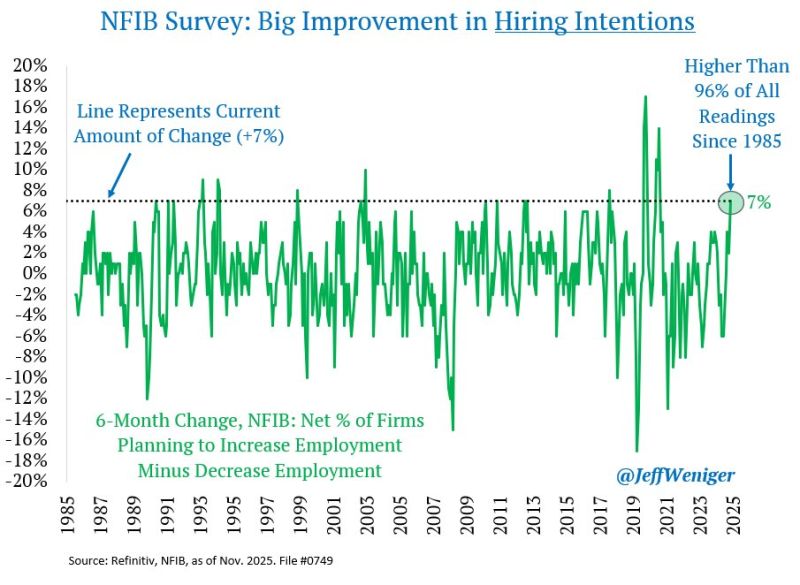

Here's a chart that shows the US labor market is improving - and not deteriorating.

The NFIB Small Business Optimism survey saw a rise in the number of firms who plan to increase employment versus decrease employment. Over the last 6 months, the rate-of-change exceeds 96% of all periods since 1985. Source: Jeff Weniger

"Low hire, low fire... low quitting"

In the US, number of quits plunges to 5 years low, as hiring slide accelerates Source: zerohedge