From checkout lanes to blockchain?

Walmart, Amazon, and Expedia exploring stablecoins? Major retailers are looking into issuing or using stablecoins to streamline payments, cut fees, and accelerate settlement—especially across borders according to the WSJ. Their next move may hinge on the Genius Act, a bill aiming to create a clear U.S. regulatory framework for stablecoins. Source : wsj

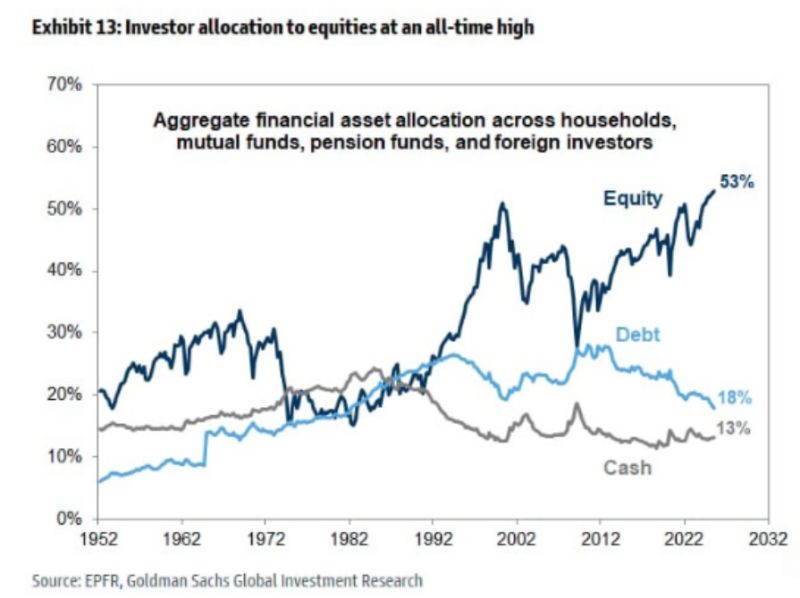

Investors are now “all-in” on equities — with the highest stock allocation on record.

The only time it came close? Right before the Dot-Com bubble burst. 👀 source : goldman sachs, barchart

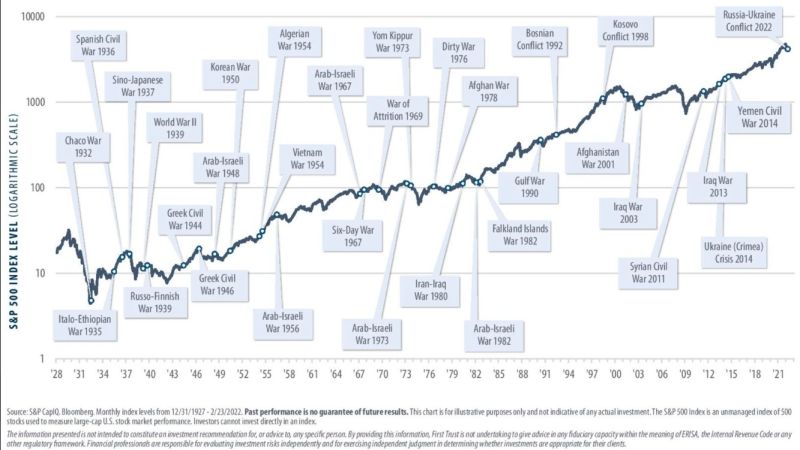

The long-term story of the S&P 500 — through the war, the fear, the crisis

source : s&p, bloomberg

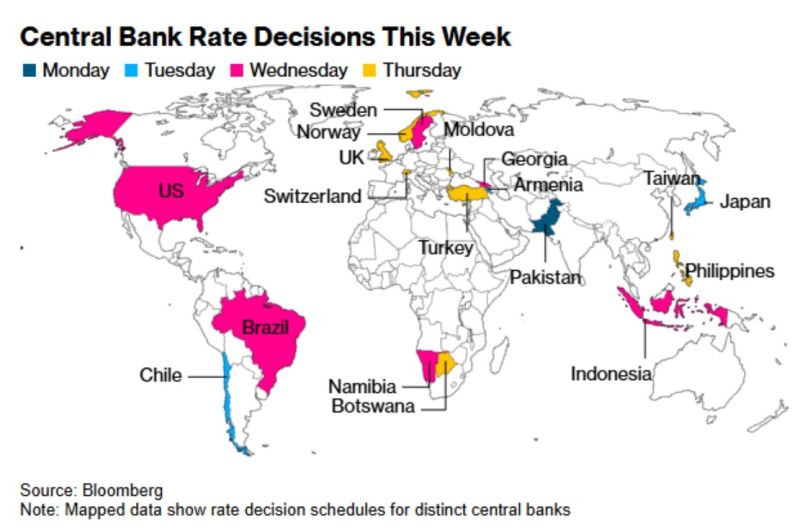

Central Bank Rate Decisions This Week

source : Bloomberg

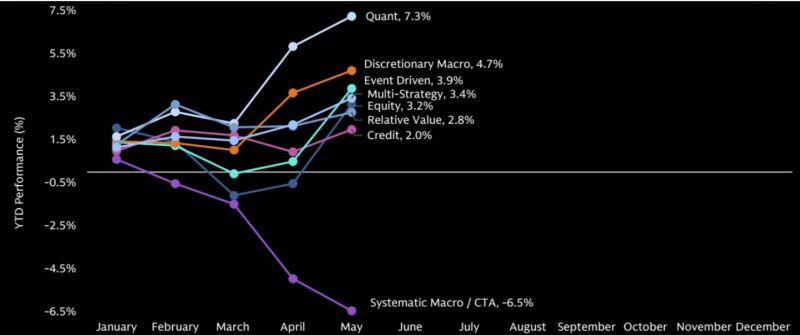

Year-to-date performance by Hedge Fund strategy

source : tme, GS prime brokerage

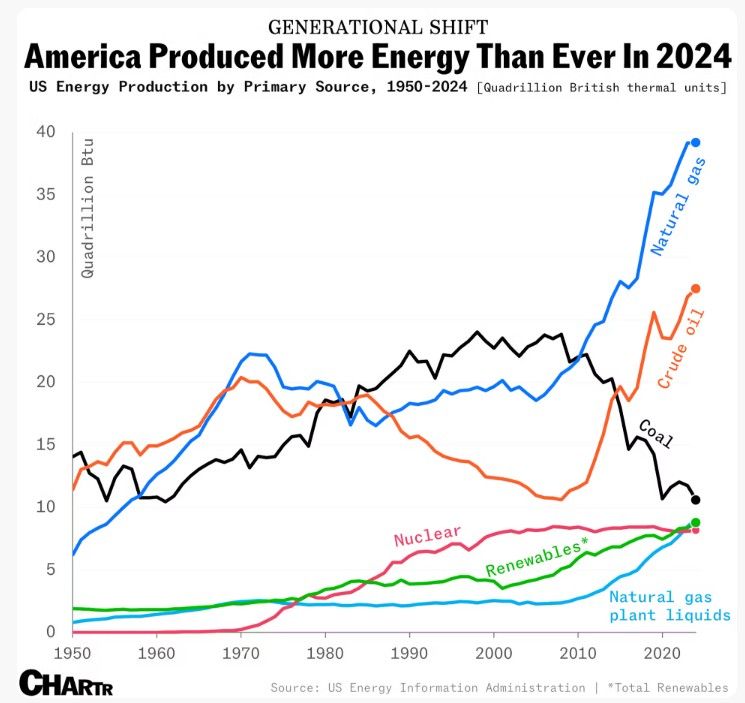

US energy production hits new record high

The United States just hit a new all-time high in energy production, reaching 103 quadrillion BTUs in 2024. This record was driven by strong growth in renewables — with solar up 25%, wind up 8%, and biofuels up 6%. Crude oil output also reached a record 13.2 million barrels per day, keeping the U.S. as the world’s top producer. Natural gas remained the largest energy source, while coal production fell to a 60-year low. Source : chartr

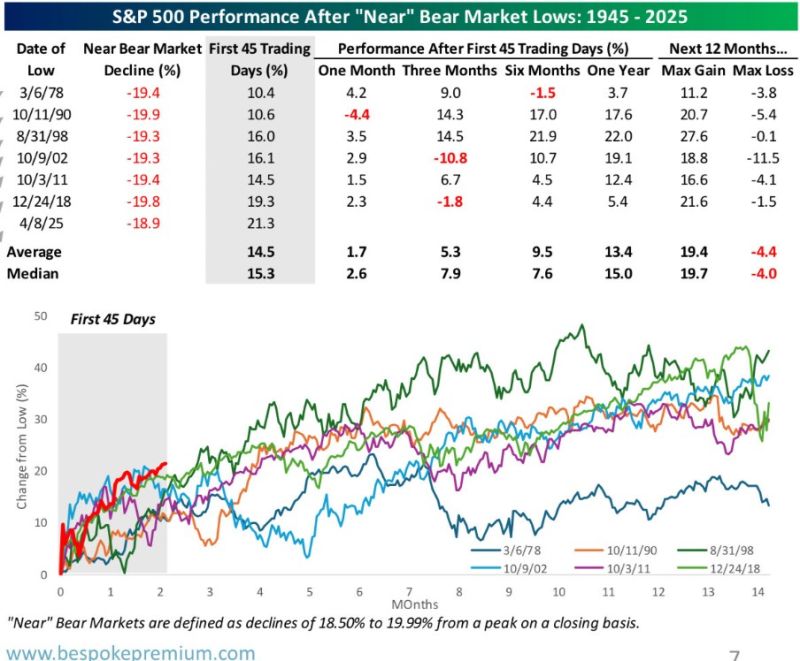

The S&P 500 recently saw its 7th “near” bear market since WWII, dropping 18.9%.

Historically, after the previous six similar declines, the market rebounded every time — with an average gain of 13.4% over the following year. History doesn’t repeat, but it often rhymes… source : bespoke

The market cap of the S&P 500 is now at $53.7 Trillion

Source: econovisuals