😱Yesterday's China equity market performance in one chart !!!

Below is a heat map of today's returns of the 2,230 stocks which belong to the Shanghai Composite index... Not a single one was down (the worst one was actually flat). And 10 stocks gained more than 20%... Source: Oktay Kavrak, CFA

STILL BREAKING 🚨 China Short Sellers

This just got exponentially worse for Hedge Funds shorting Chinese stocks! Source: Barchart

Fed Chair Jerome Powell just said the recent 50BPs interest rate cut shouldn’t be interpreted as a sign that future moves will be as aggressive - CNBC

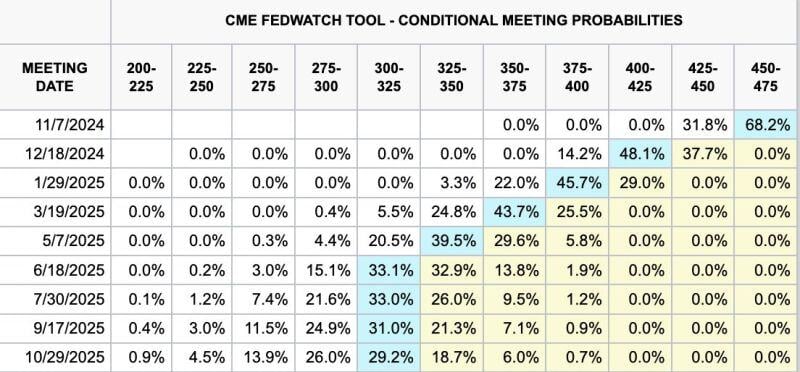

“Looking forward, if the economy evolves broadly as expected, policy will move over time toward a more neutral stance. But we are not on any preset course,” he told the National Association for Business Economics in prepared remarks. “The risks are two-sided, and we will continue to make our decisions meeting by meeting” The market currently thinks there's a 68.2% chance Jerome Powell and the Fed cut rates by 25BPs at the next FOMC meeting Source: CME FedWatch Tool

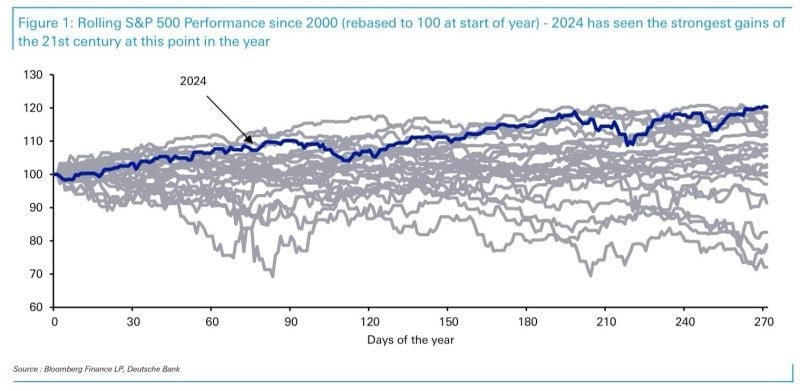

Deutsche: S&P 500 has seen its biggest YTD advance of the 21st century so far after 271 days of the year.

Equity markets continue to be carried on by a "magic combo": resilient earnings, a weak dollar, weak oil prices, lower bond yields, favorable macro background (growth surprising on the upside / inflation surprising on the downside), a dovish central bank pivot, and now fresh stimulus out of China. This helps the market "climbing the wall of worry", i.e US elections uncertainty,, Middle East tensions, yen carrytrade unwinding, etc. October is historically a volatile month. Let see if the sp500 can continue to rise in a straight line. Source chart: DB

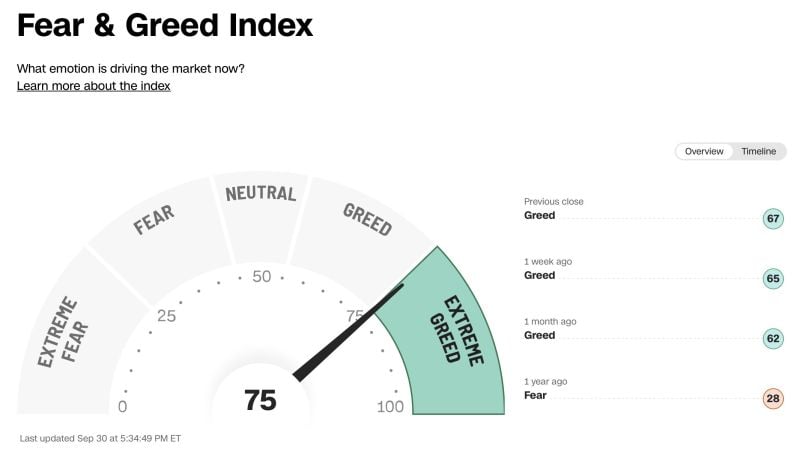

JUST IN 🚨 : Extreme Greed returns to the Stock Market for the first time since March 🤑 🤑🤑

Source: Barchart, CNN

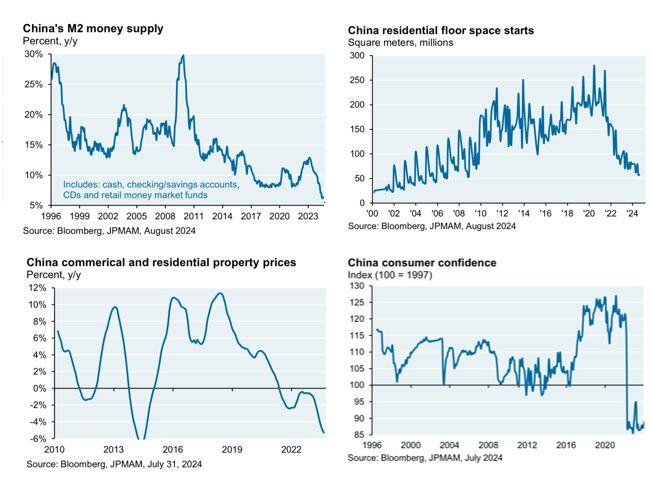

JPMORGAN, on China stimulus:

“.. I don’t think it’s an exaggeration to say that China is acting somewhat out of desperation given the severity of the declines shown in the charts below.” [Cembalest] This is very close to our thesis >>> We view this stimulus package as an emergency policy adjustment designed to halt the downward trend, NOT to engineer a higher level of economic growth going forward. The package addresses short-term risks, but medium- and long-term challenges remain: Unfavorable demographic dynamics Households’ sentiment has been hit hard in the past four years and will need time to recover durably, a necessary condition for higher domestic consumption Business and investors’ sentiment has equally been damaged by the succession of regulatory crackdowns and anti-bribery campaigns. The latest announcements are an encouraging sign for domestic and foreign equity investors, but only a small first step in rebuilding the confidence toward Chinese listed companies. Trade barriers have already increased for China’s exports to the US and Europe and this trend is unlikely to reverse, especially if Donald Trump is elected Source: Carl Quintanilla on X

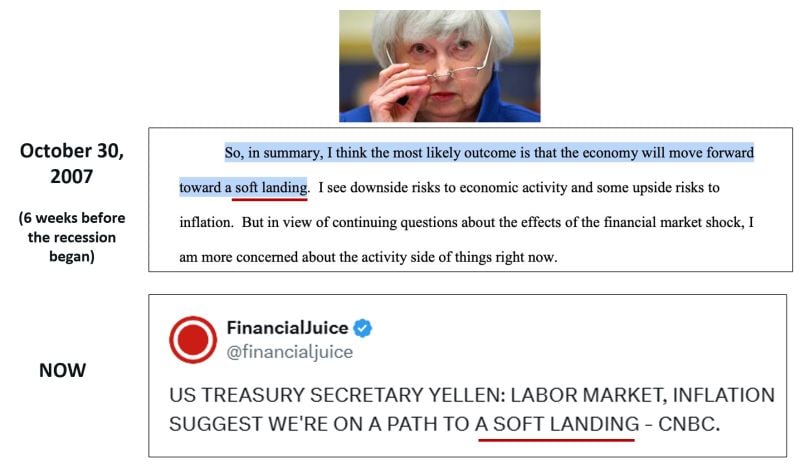

A soft landing of the US economy is our CORE scenario.

But we are well aware of the tail risk (hard landing and no landing). As a remainder, in 2007, Yellen talked about a soft landing 6 weeks before the recession began...

It's a bull market baby...

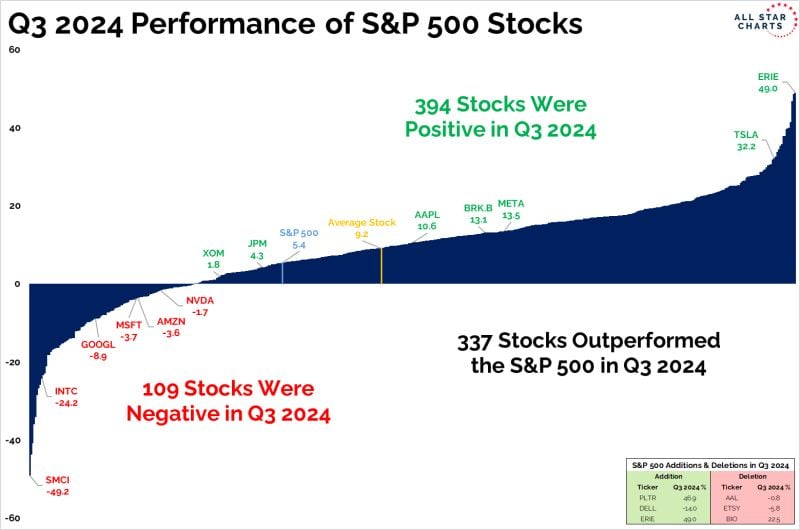

Some amazing statistics for the sp500 Q3 performance as highlighted by Grant Hawkridge on X 👉 S&P 500 closed Q3 at 5.4% 👉The average stock in Q3 was 9.2% 👉394 stocks were positive in Q3 👉109 stocks were negative in Q3 👉337 stocks outperformed the S&P 500 in Q3 These are the things you tend to see during bull markets...