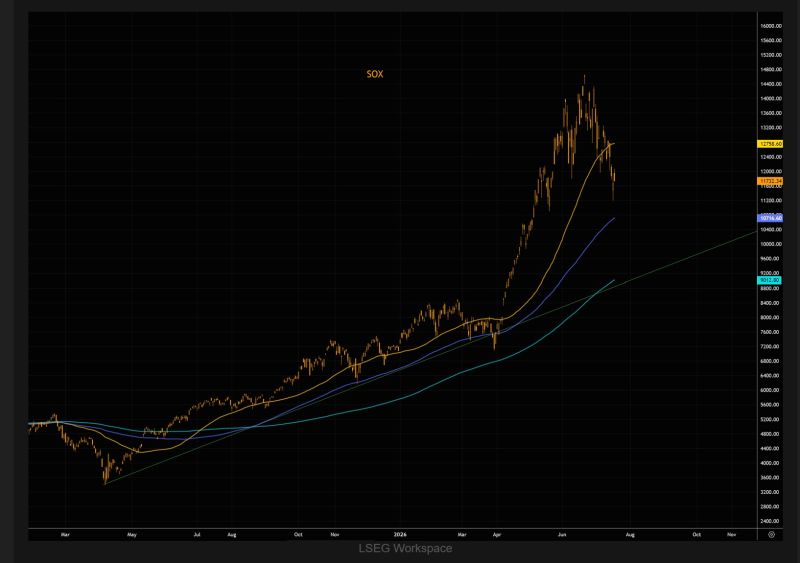

The SOX semiconductors index has posted just three positive sessions over the past 13 trading days.

While the index is well below its 50-day moving average, it still sits comfortably above the 100-day moving average. The 200-day moving average coincides with the longer-term uptrend, creating an important technical support zone. Until positioning is further reset, expect elevated volatility and erratic price action. Source: TME

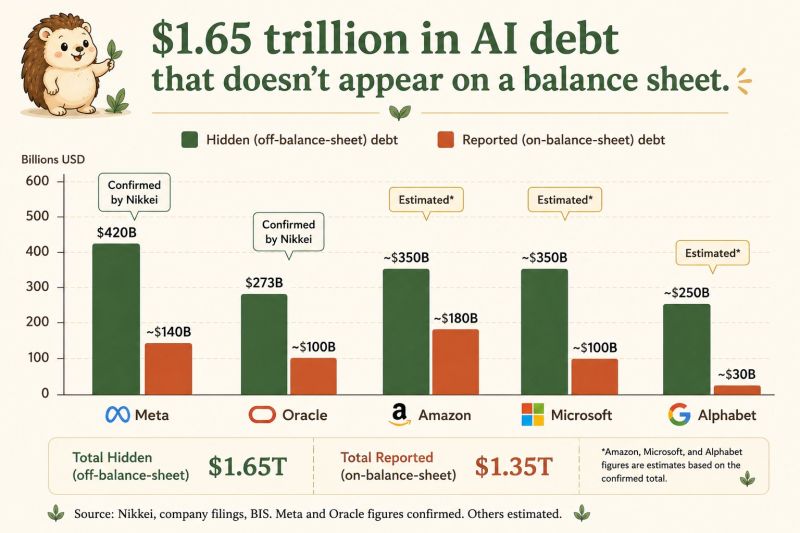

Bi Tech's AI debt may be far larger than investors realize.

A Nikkei investigation found that Alphabet, Microsoft, Amazon, Meta, and Oracle have $1.65 trillion of off-balance-sheet obligations, exceeding the $1.35 trillion of debt they officially report. These commitments—GPU contracts, data center leases, and joint ventures—remain largely invisible under current accounting rules until facilities become operational. Meta alone reportedly has $420 billion in hidden obligations, while Oracle's exposure has exploded over the past four years. The key risk? Investors focusing on earnings may be seeing only part of the picture. As AI infrastructure comes online, these commitments will gradually move onto balance sheets. If AI demand falls short of expectations, expensive assets could face write-downs, with losses ultimately flowing to shareholders and the private credit investors who financed the AI buildout. Source: Hedgie

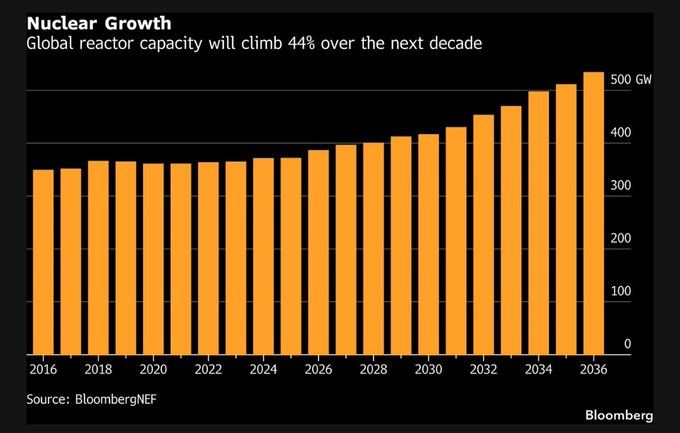

The uranium supply story is becoming impossible to ignore

Global nuclear reactor capacity is projected to grow 44% over the next decade. Every new 1 GW reactor requires: ~400 tonnes of uranium for its initial core load. ~160 tonnes per year thereafter to keep operating. Here's the catch: The first core loads alone for the reactors currently planned would consume uranium equivalent to nearly 90% of today's annual global mine production. That's before a single kilowatt-hour of electricity is produced. The market isn't just facing rising annual demand. It must first fill an enormous pipeline of initial fuel requirements. This is why many investors believe the structural bull case for uranium is still in its early stages. Source: Bloomberg, Lukas Ekwueme @ekwufinance

USD/JPY is back at 162.7

That's the same danger zone Japan has spent months trying to escape. Since April, policymakers have thrown almost everything at the yen: • ¥11.73 trillion ($73.5B) in record FX intervention. • A BOJ rate hike to 1%, the highest since 1995. • Signals that GPIF, the world's largest pension fund, could shift more capital back into Japanese assets. Each move strengthened the yen... briefly. Each move ultimately failed. Now USD/JPY is right back where it started. This isn't just a currency story. A weaker yen makes every barrel of imported oil and every shipment of food more expensive, adding inflationary pressure while squeezing household purchasing power. Exporters may benefit, but Japanese consumers pay the price. When direct intervention, higher interest rates, and portfolio reallocation all fail to change the trend, markets are sending a clear message. Japan isn't just fighting a weak currency anymore. It's fighting the limits of its own policy tools. Source: Bull Theory

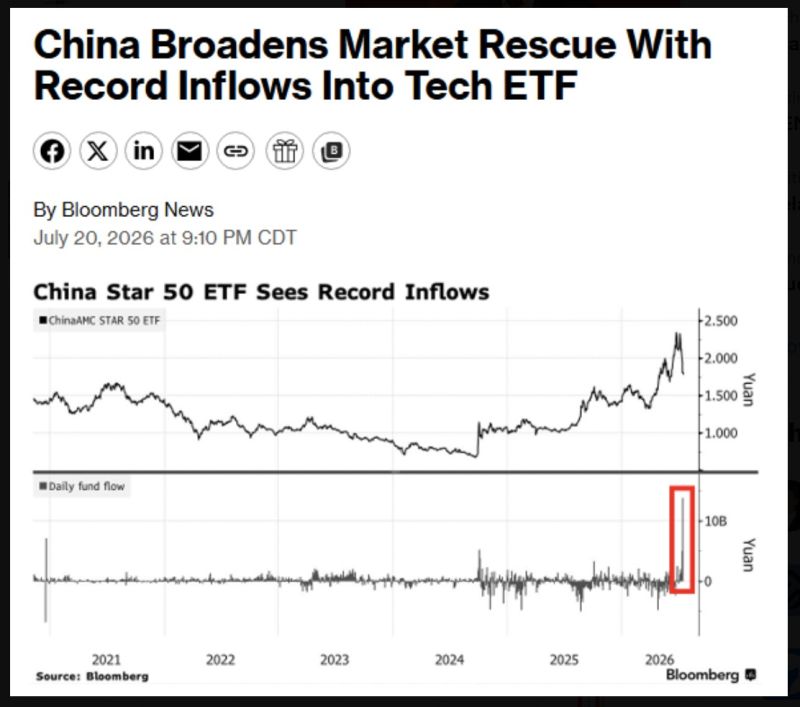

China's government just pumped 13.8 Billion Yuan ($2 Billion USD) into their largest ETF tracking semiconductor stocks, the fund's largest inflow in history

Bloomberg, Barchart

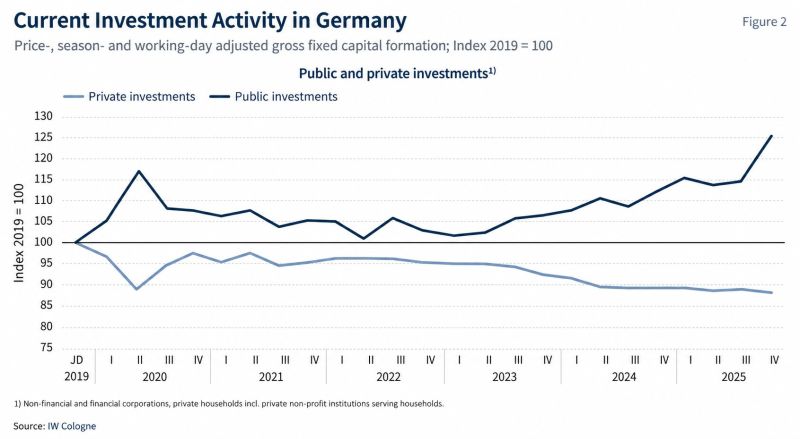

In Germany, the state is investing, but companies still aren’t.

Public investment has surged to 125% of its 2019 level, while private investment has fallen to 88%. One year after “Made for Germany,” corporate spending is rising, but far too slowly to hit the €631bn target by 2028. Germany is becoming more expensive without becoming more attractive. (HT CEO Table) Source: HolgerZ

Iraq just signed 48 DEALS with US companies, including with USA oil giants to bypass the Strait of Hormuz via a new pipeline

Total deals are worth over $60 BILLION, per Reuters. Chevron, ExxonMobil, Shell and more are also involved They also involved other industries, including healthcare, communications and infrastructure. It’s not clear when the oil deals will be able to create viable alternatives to the Strait of Hormuz, through which about a fifth of the world’s oil flows. Goldman Sachs estimates that pipelines in just one country take at least two and a half years to build, and these pipelines would travel through two or more nations. Iran has sought to close the Strait repeatedly since the U.S.-Iran war began Feb. 28, causing sharp gyrations in oil and gas prices. Alternatives routes for oil will weaken Iran's main bargaining power. Will China be the big loser here? Source: AP, Al Jazeera

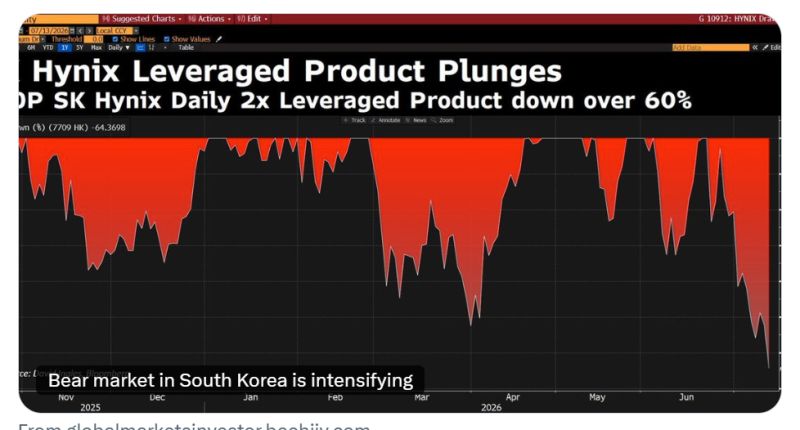

THIS IS HOW EXCESSIVE LEVERAGE AND SPECULATION END:

The SK Hynix long 2x Leveraged ETF, listed in Hong Kong, is down -64% from its June peak. SK Hynix shares have fallen more than -35% from their June peak. Source: Global Markets Investor