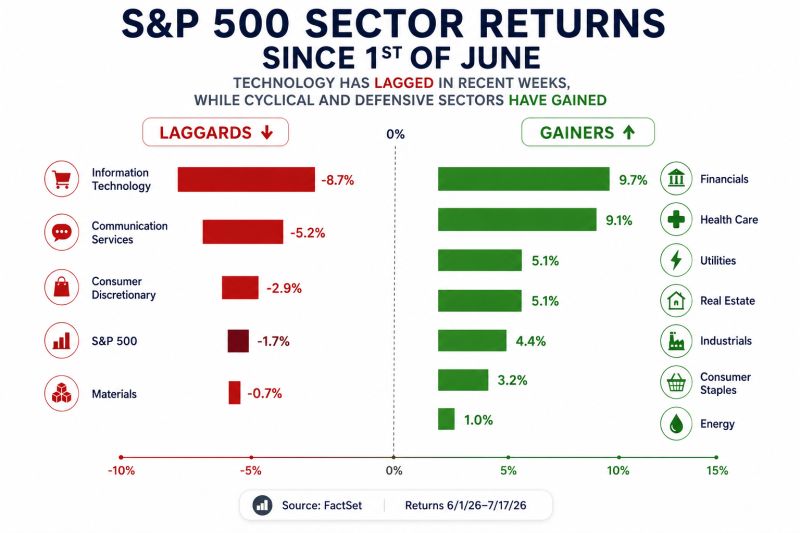

After gaining nearly 11% this year, the S&P 500 paused this week, slipping more than 1%.

But beneath the headline move, a broader rotation is underway, both across sectors and within them. Since early June, AI-driven sectors such as Technology have lost momentum, while cyclical and defensive sectors have steadily outperformed. The shift extends well beyond this week's pullback, suggesting investors are broadening exposure rather than simply reducing overall market risk. Source: Edward Jones

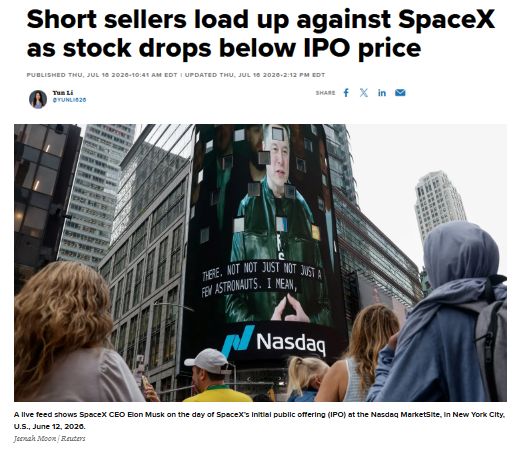

SpaceX $SPCX short sellers have now built a position equal to roughly one third of the company's public float, worth about $25 Billion

Source: Barchart

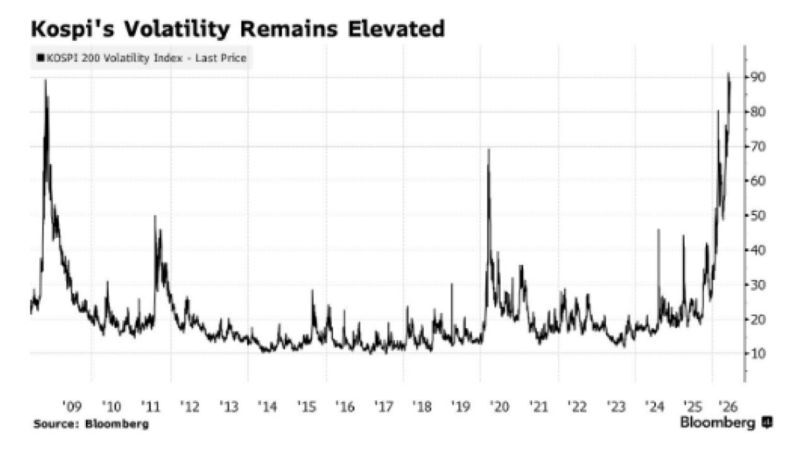

South Korea Stock Market volatility hits highest level in history, surpassing the Global Financial Crisis

Source: Barchart, Bloomberg

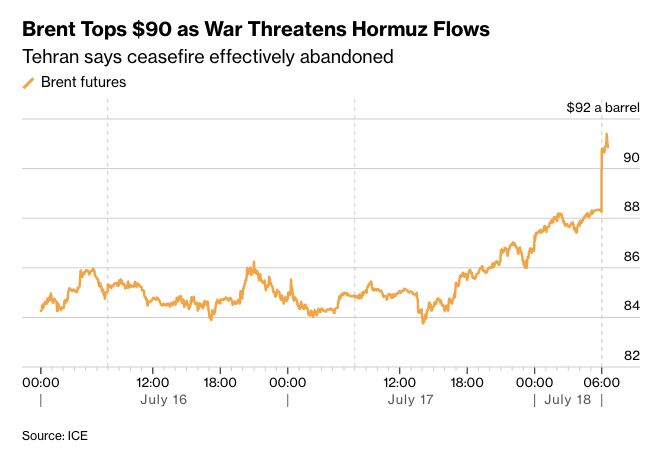

BRENT CRUDE OIL JUST JUMPED BACK OVER $90 PER BARREL

Source: Evan @StockMKTNewz Bloomberg

Hedge Funds going long oil at the fastest pace in a decade

Source: Barchart

BIGGER THAN GOLD: WHEN INNOVATION OUTVALUES THE WORLD’S MOST HISTORIC STORE OF WEALTH

Source: Investorsight

America isn't retiring anymore. It's working longer than ever.

One in three Americans aged 55 and older is still working or looking for work, and that share has been climbing for nearly 40 years. The biggest change is among older workers: • Ages 65–69: participation has nearly doubled since the late 1980s, now above 30%. • Ages 70–74: from under 10% to almost 19%. • Ages 75+: participation has doubled to roughly 8%. The numbers are striking. Nearly 11.9 million Americans aged 65+ were employed last year, more than double the level of three decades ago. Between 2015 and 2024, the 65+ workforce expanded 33%, while the overall labor force grew by less than 9%. Longer life expectancy is part of the story. But so are disappearing pensions, rising living costs, and Social Security benefits that no longer stretch as far. Retirement is increasingly becoming a luxury rather than the default. Source: hedgeye

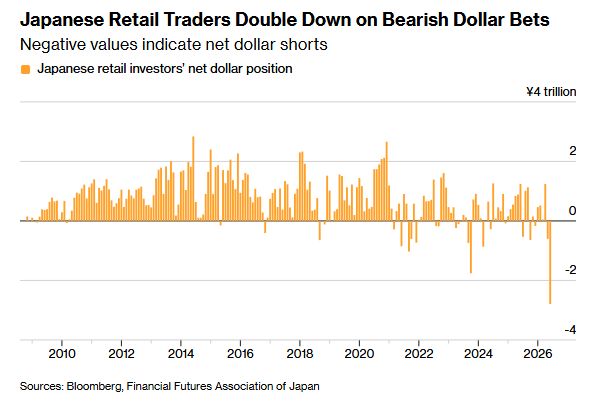

Japanese Retail Traders have now built the largest U.S. Dollar short position since the Global Financial Crisis

Source: Barchart