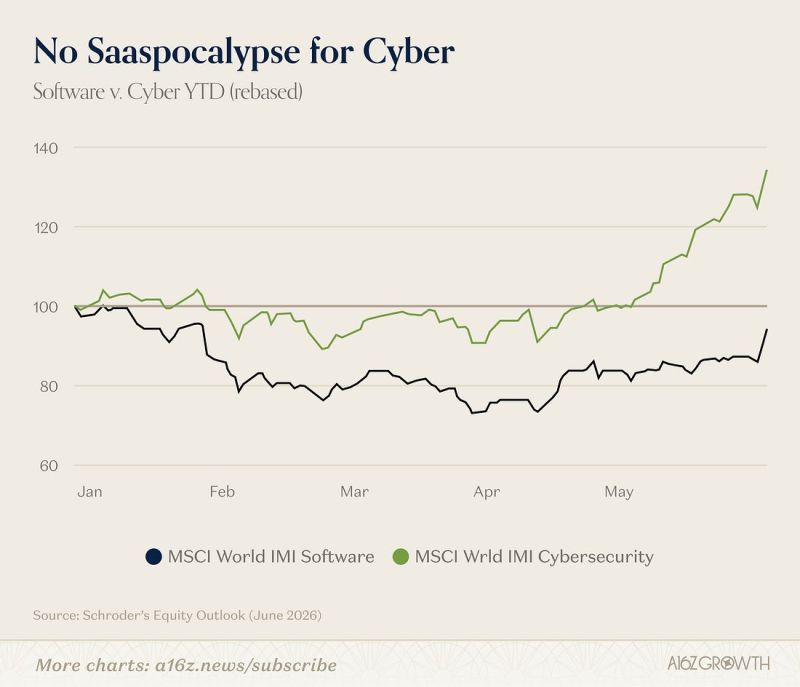

Cybersecurity stocks are up +29.5% YTD while software has barely broken even

Source: Hedgeye

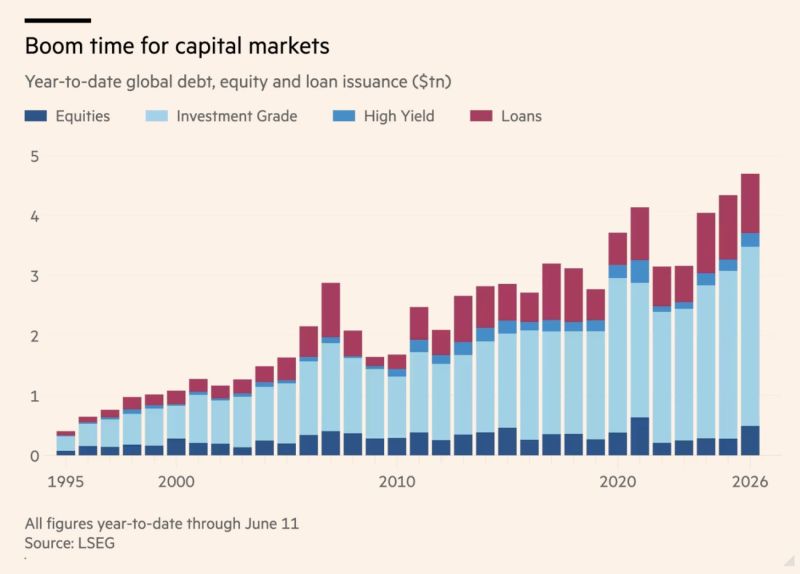

Wall Street digests record fundraising haul as AI race intensifies.

Companies have raised roughly $4.7tn across global equity, debt and bank loan markets this year, a record pace, according to data provider LSEG. That figure, up 7% YoY, does not include the spurt of activity in investment-grade private credit markets, which are increasingly being tapped to finance data centres, chips and power plants feeding the AI boom. That included a $35bn debt package cobbled together by Apollo and Blackstone this week for Anthropic. Source: FT, HolgerZ

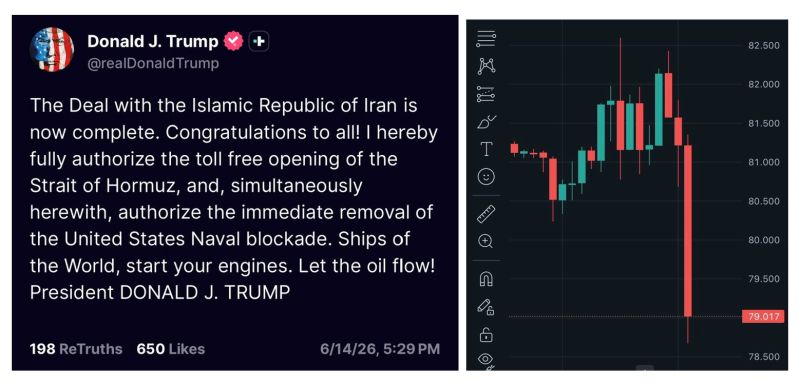

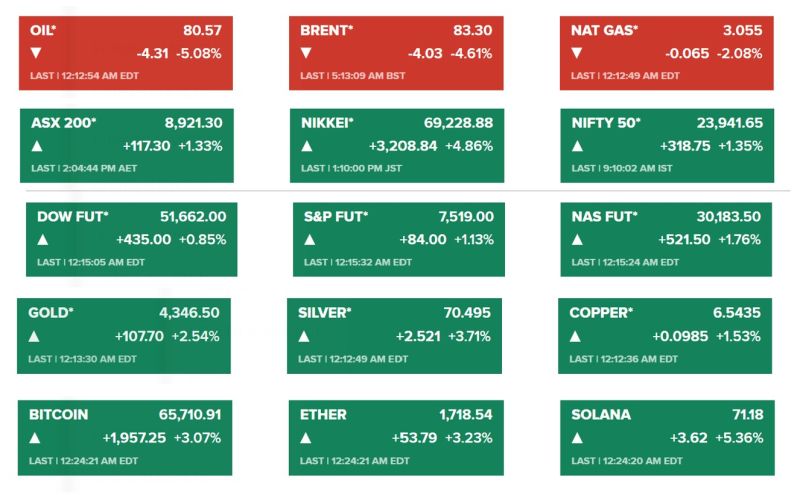

Trump: "The deal is complete (...) Let the oil flow!" Crude oil $WTI is plummeting on Hyperliquid in pre-market open!

After 107 days of war, the US and Iran have now officially reached a peace deal, with the signing set for June 19th in Switzerland.

Pakistan’s prime minister said the US and Iran have finalised a deal to extend a ceasefire and reopen the Strait of Hormuz, with the warring parties to officially sign the agreement on Friday.

Shehbaz Sharif said both sides have declared the immediate and permanent termination of military operations on all fronts, adding that the signing ceremony would take place in Switzerland. “Following intensive talks, we are pleased to announce that the Peace Deal between the United States of America and Islamic Republic of Iran has been REACHED,” he said on X. “With the agreement now in place, mediators will facilitate a series of meetings this week. These pre-implementation discussions will lay the foundation for the technical talks and the official signing ceremony.” Source: FT

The Iran-US peace deal has immediate effects on markets:

- Oil is tumbling, as the Hormuz Risk Premium unwinds. Oil fell to its lowest level since March - Nikkei 225 surges and hit 69,000 for the 1st time ever - Nasdaq futures are up +1.8% - Precious metals and cryptos soar - US 10 year yield drops 5bps to 4.42%

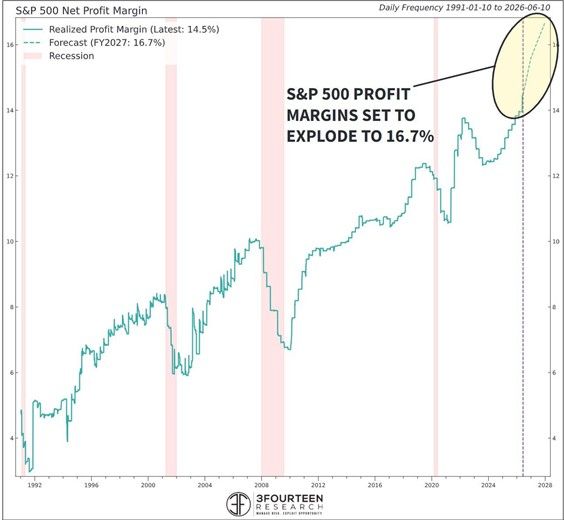

Tough to be bearish when you see such a chart...

Of course, these are estimates and they need to be met. Source: 3fourteeenresearch

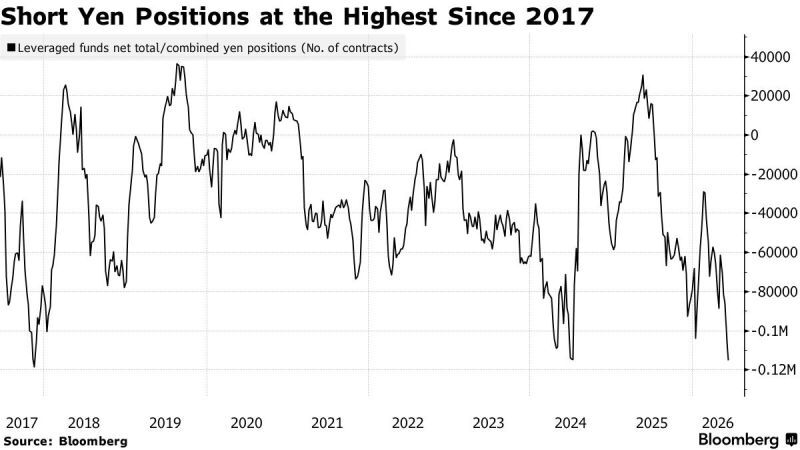

The market is massively rebuilding one of the most powerful, but also one of the riskiest trades out there: shorting the yen

📉 Many investors are once again betting on further yen weakness, even as the currency trades near a very sensitive level around 160 against the dollar, and have built their largest bearish positions on the yen since 2017. ⚠️ Market now seems to see these risks as largely priced in. A BoJ rate hike is no longer a real surprise, neither is intervention from the Ministry of Finance. The yen can still weaken gradually from here but the risk of a brutal squeeze rises as bearish positioning keeps building. Source: Christophe Barraud, Bloomberg

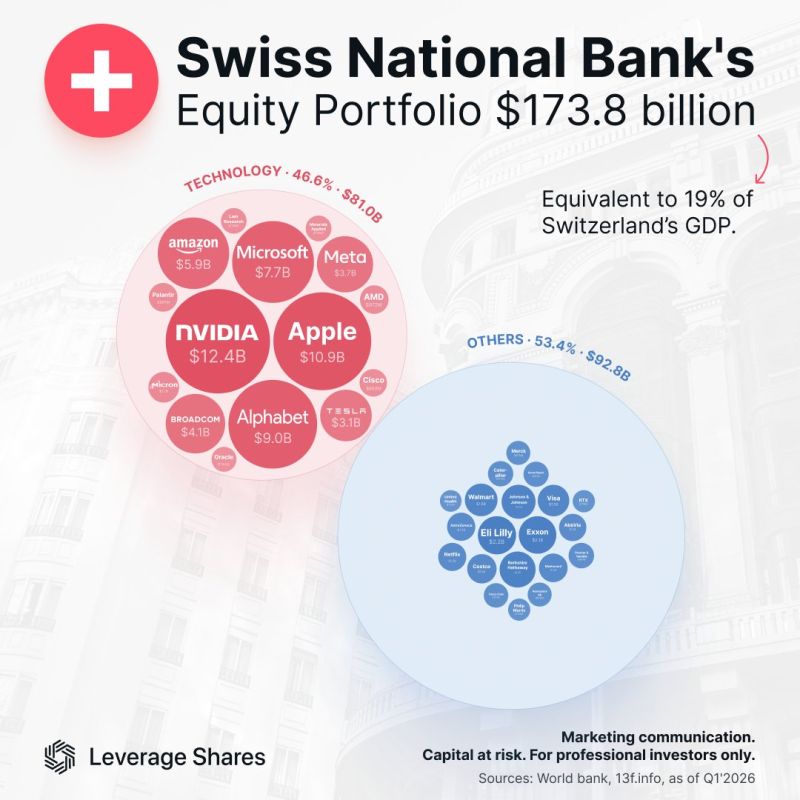

Swiss National Bank's $173B Portfolio

Source: The Market Mind