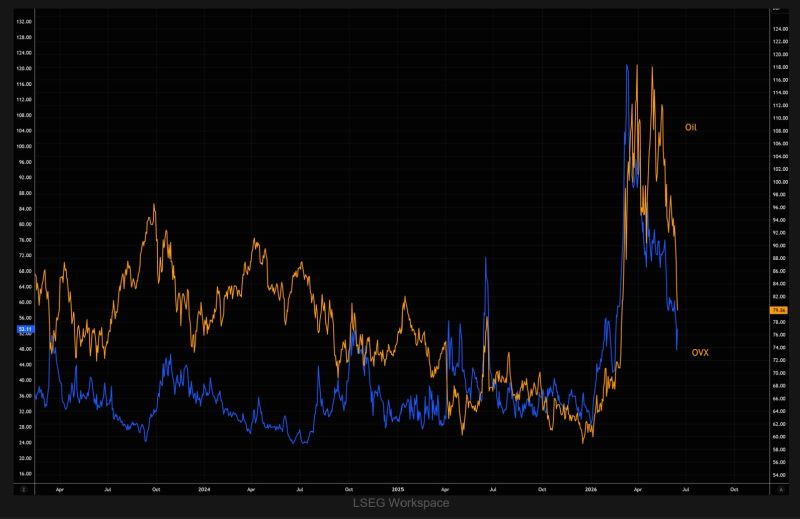

OVX (the VIX equivalent for Oil) has almost completely round-tripped the war spike, trading back near pre-conflict levels.

Markets have aggressively removed geopolitical risk premium, even though the region remains far from calm. Volatility is not screamingly cheap, but it offers a relatively inexpensive way to express a directional oil view or simply own gamma should tensions escalate again Source: TME

The number of ETFs that held SpaceX went from 4 to 40 to now 120 in a couple days (few billion total).

These are all active ETFs choosing to buy, not indexes (they coming later). Here's a look at the list sorted by new buy, $JEPQ (the 2nd largest active ETF in world) at the top. Looks like a lot of JPM funds bought. Source: Eric Balchunas, Bloomberg

Michael Burry wants to short SpaceX $SPCX, but the options are too expensive

Source: Yun Li

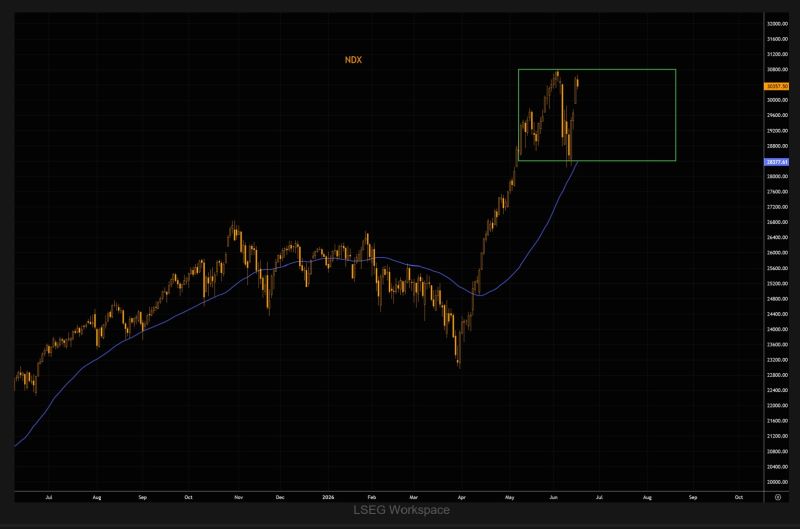

NASDAQ bounced on range lows and the 50-day moving average, only to reverse near range highs.

Massive moves, but no new direction. In a market like this, chasing breakouts has been one of the most expensive trades around. Source: TME

The World's Trillion Dollar Stock Markets

🇺🇸 U.S. — $52.6T 🇨🇳 China — $11.5T 🇯🇵 Japan — $6.5T 🇮🇳 India — $4.4T 🇫🇷 France — $3.2T 🇬🇧 UK — $3.1T 🇸🇦 KSA — $2.9T 🇨🇦 Canada — $2.6T 🇩🇪 Germany — $2.2T 🇹🇼 Taiwan — $2.0T Source: The Market Mind @Market_Mind_

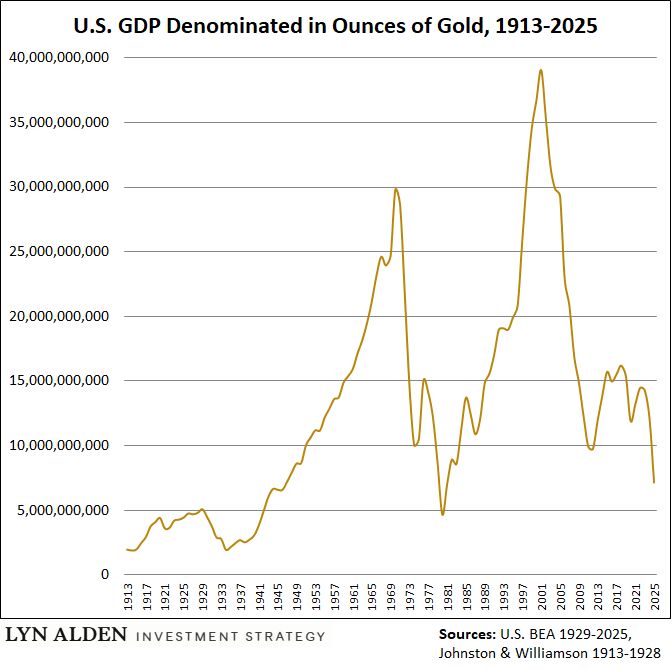

If you denominate US GDP in gold instead of dollars, the chart is wild.

Source: Lyn Alden

The U.S. Department of Justice (DOJ) has intervened in a lawsuit against Elon Musk's AI company, xAI, arguing that its Colossus 2 data center is critical to U.S. national security.

The NAACP sued xAI in April 2026 under the Clean Air Act, alleging the company was operating gas turbines without the necessary permits to power its AI facility. The turbines are located in Southaven, Mississippi, near the data center in Memphis, Tennessee. According to the lawsuit, the number of turbines has increased from 27 to 57 since the case was filed. xAI maintains that the turbines are exempt from Mississippi permitting requirements because they are mounted on trailers and classified as temporary mobile equipment. On Monday, the DOJ filed court documents arguing that shutting down the turbines could harm U.S. national, economic, and energy security. The department stated that the facility supports military AI capabilities. A declaration from the Defense Department's Chief Digital and AI Officer, Cameron Stanley, said Grok is one of only four AI models approved for mission-critical use on classified U.S. government networks and has been utilized in recent military operations involving Iran. The DOJ, xAI, and the State of Mississippi are jointly seeking dismissal of the lawsuit. Source: Bull Theory

“These forecasts have been abysmal. My dots wouldn’t be perfect either, so I wouldn’t give them.”

Fed Chairman Kevin Warsh has spent 15 years arguing the central bank says too much. Wednesday is his first meeting. My story on the quiet revolution he wants: Source: Nick Timiraos @NickTimiraos