Yesterday, Elon Musk's net worth rose by $165 billion in one day, more than Bill Gates' entire net worth.

Elon is now worth $1.3 trillion. Source: Watcher Guru

Here are the reported terms of the US-Iran peace deal MOU:

1. Immediate and permanent end to war on all fronts, including Lebanon 2. US naval blockade on Iranian ports lifted immediately 3. Strait of Hormuz to reopen within 30 days 4. US oil and petrochemical sanctions on Iran suspended 5. $24 billion in frozen Iranian assets released during 60-day negotiation period, $12 billion before talks even start 6. 60-day negotiation period for Iran's nuclear programme and full sanctions relief 7. Final signing in Geneva on June 19. JD Vance expected to attend The US disputes point 5, saying no funds will be released without Iran fulfilling commitments first.

If you were looking for cross-assets correlation... Below chart is Hyperscalers vs token prices...

Source: Bloomberg, zerohedge

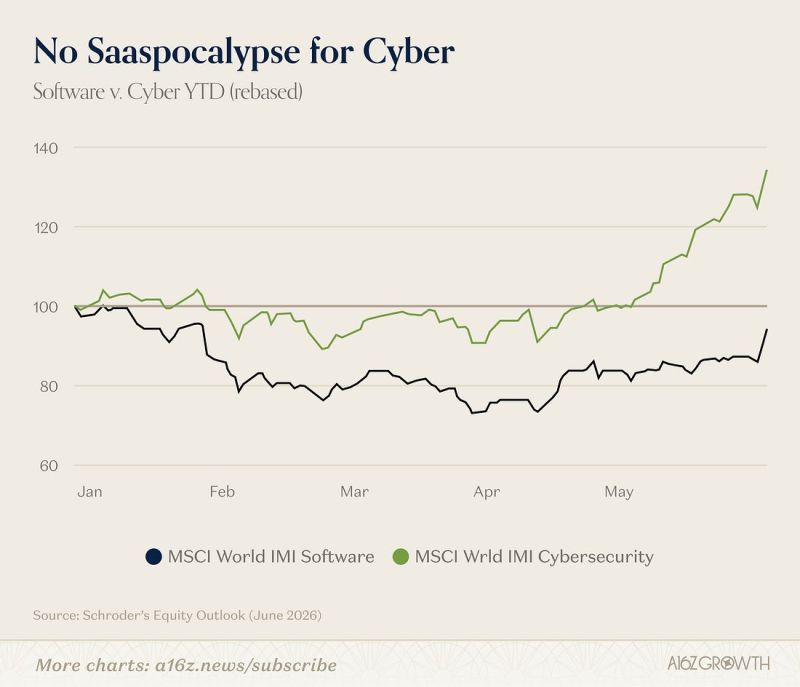

Cybersecurity stocks are up +29.5% YTD while software has barely broken even

Source: Hedgeye

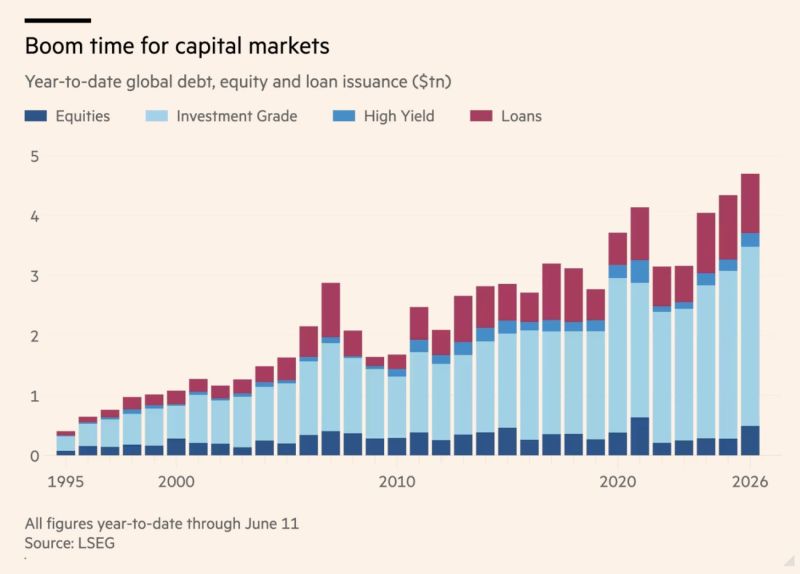

Wall Street digests record fundraising haul as AI race intensifies.

Companies have raised roughly $4.7tn across global equity, debt and bank loan markets this year, a record pace, according to data provider LSEG. That figure, up 7% YoY, does not include the spurt of activity in investment-grade private credit markets, which are increasingly being tapped to finance data centres, chips and power plants feeding the AI boom. That included a $35bn debt package cobbled together by Apollo and Blackstone this week for Anthropic. Source: FT, HolgerZ

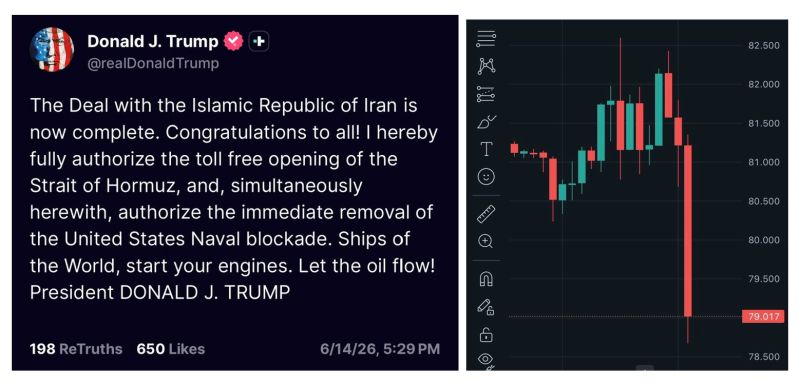

Trump: "The deal is complete (...) Let the oil flow!" Crude oil $WTI is plummeting on Hyperliquid in pre-market open!

After 107 days of war, the US and Iran have now officially reached a peace deal, with the signing set for June 19th in Switzerland.

Pakistan’s prime minister said the US and Iran have finalised a deal to extend a ceasefire and reopen the Strait of Hormuz, with the warring parties to officially sign the agreement on Friday.

Shehbaz Sharif said both sides have declared the immediate and permanent termination of military operations on all fronts, adding that the signing ceremony would take place in Switzerland. “Following intensive talks, we are pleased to announce that the Peace Deal between the United States of America and Islamic Republic of Iran has been REACHED,” he said on X. “With the agreement now in place, mediators will facilitate a series of meetings this week. These pre-implementation discussions will lay the foundation for the technical talks and the official signing ceremony.” Source: FT

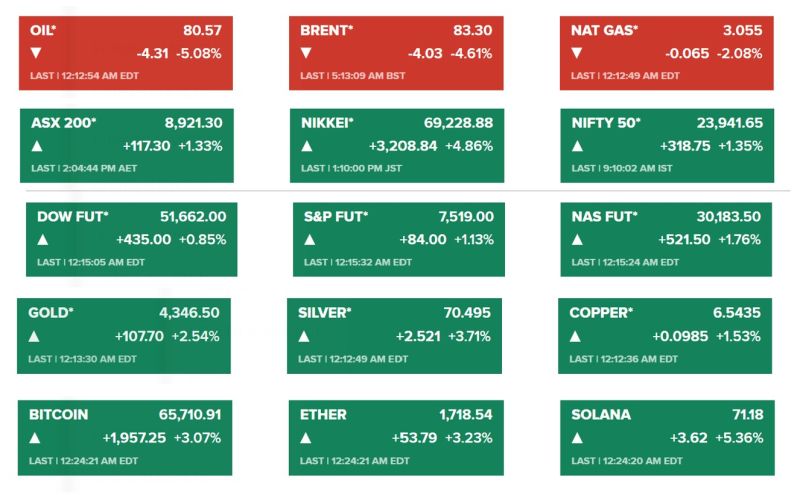

The Iran-US peace deal has immediate effects on markets:

- Oil is tumbling, as the Hormuz Risk Premium unwinds. Oil fell to its lowest level since March - Nikkei 225 surges and hit 69,000 for the 1st time ever - Nasdaq futures are up +1.8% - Precious metals and cryptos soar - US 10 year yield drops 5bps to 4.42%