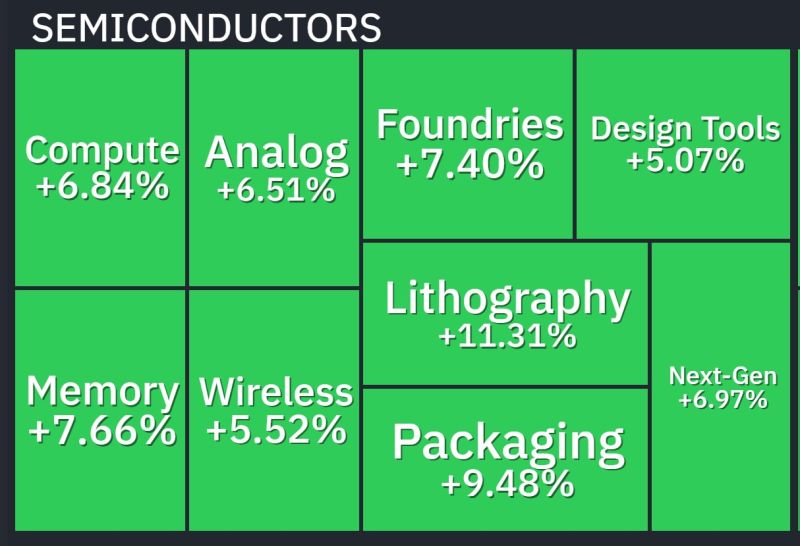

What a day for semiconductors

Source: Finviz

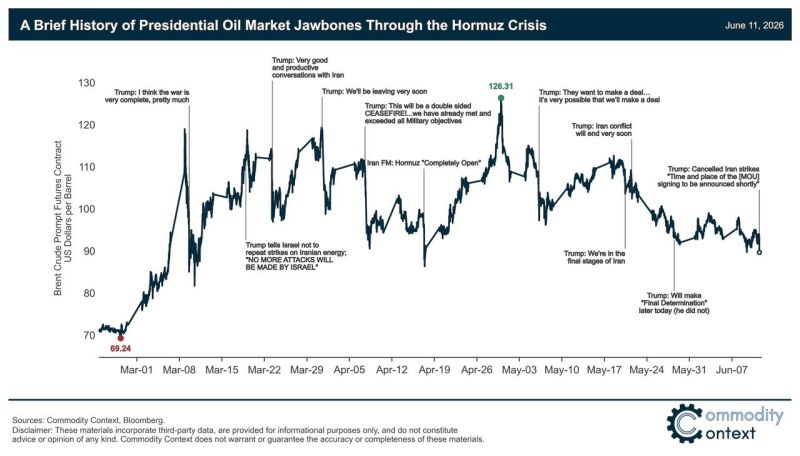

Yesterday was a "TACO-Thursday", with Trump's rhetoric intraday-flipping from 'blowing the sh*t out of Iran' to a 'no strikes

Deal pretty much wrapped up' sparking a plunge in oil (ignoring denials), spike in stocks, and big drop in yields (shrugging off hot headline PPI and ECB rate-hikes). CNN reports that this is the 38th time that President Trump has declared a peace deal is imminent... Source: zerohedge

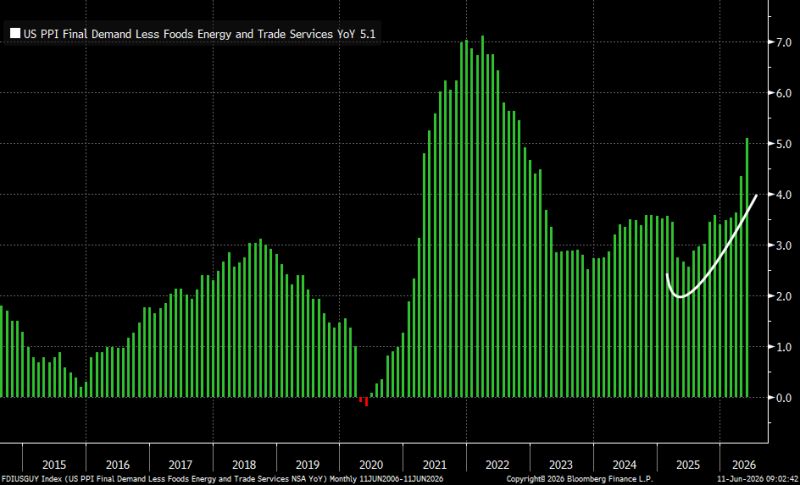

The SuperCore PPI (i.e., no food, energy or trade) has been accelerating for 11 months.

Source: Bernstein Advisors

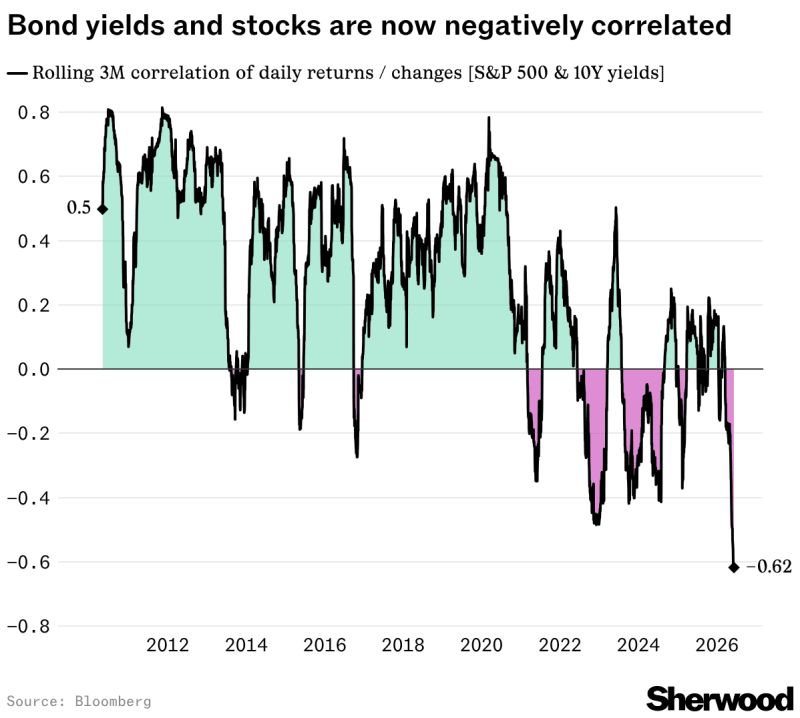

"The relationship between what the US government's debt is doing and stock prices has flipped in a big way. In fact, this is the most extreme yields-stocks relationship this entire market cycle."

Source: Daily Chartbook

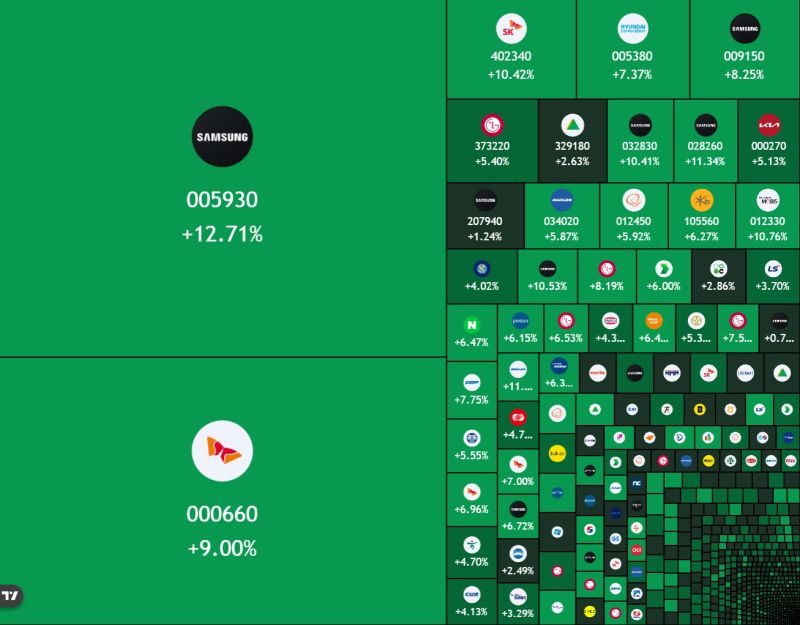

South Korea’s KOSPI just exploded almost +8%, making it one of the biggest rallies in the index’s history.

Over ₩600,000,000,000,000 ($400+ BILLION) was added to South Korea's stock market on hopes for an end to the Middle East conflict. A buy-side sidecar was triggered shortly after the market opened. Source: Bull Theory

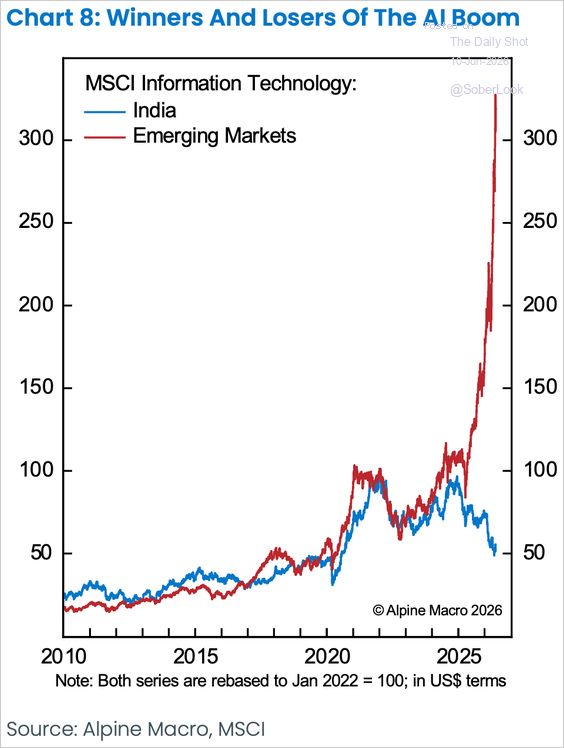

While AI has fueled a surge in EM technology stocks, India’s IT sector has been left behind.

Source: Alpine Macro

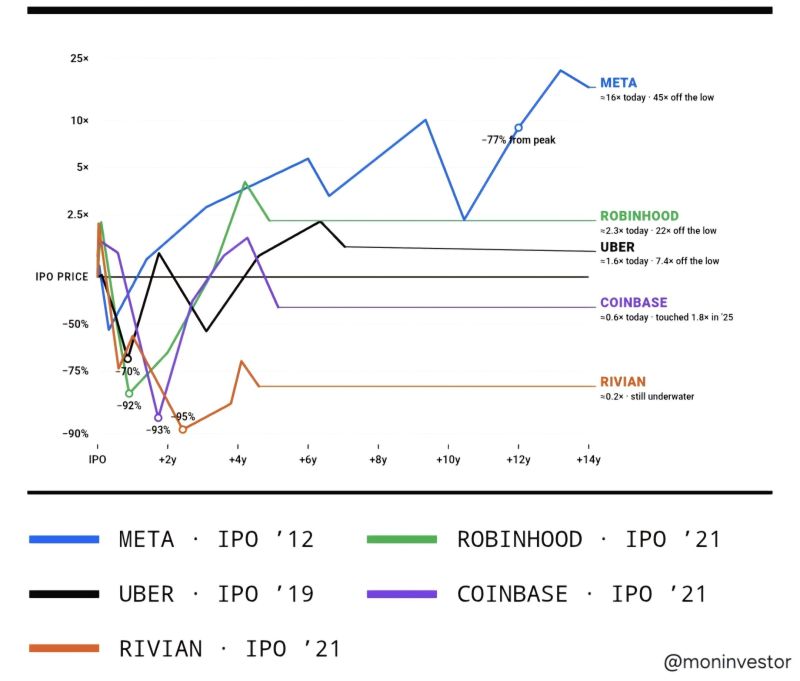

This chart is why you should be careful with the SpaceX IPO.

Five of the most hyped IPOs of the last 15 years, and every single one collapsed after listing. - UBER lost 70% of its IPO price. - META crashed 77% from its peak. - Robin Hood fell 92%. - Coinbase fell 93%. - Rivian fell 95%. The hype is often priced in on day one. And the people who bought the hype got crushed. But look at where the real money was made. At the bottom, when nobody wanted these stocks. Robinhood went up 22x from its low. Meta went up 45x. Uber 7x. Patience beat hype. Although Rivian reminds us that even patience doesn't save every company... SpaceX will be the most hyped IPO of the decade. History tells me I don't need to be there on day one. If it's a great business, there will be a better price later. First they fall. Then they fly. Source: @moninvestor

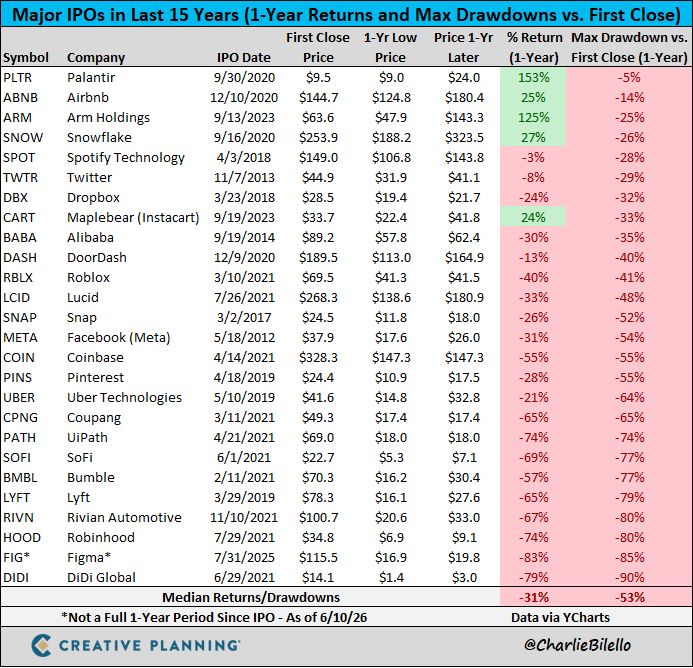

With unprecedented investor demand for the largest IPO in history (SpaceX), it's worth remembering a simple lesson:

A great company doesn't always make for a great investment at any price. The median major IPO lost 31% in its first year & suffered a 53% drawdown along the way. Source: Charlie Bilello