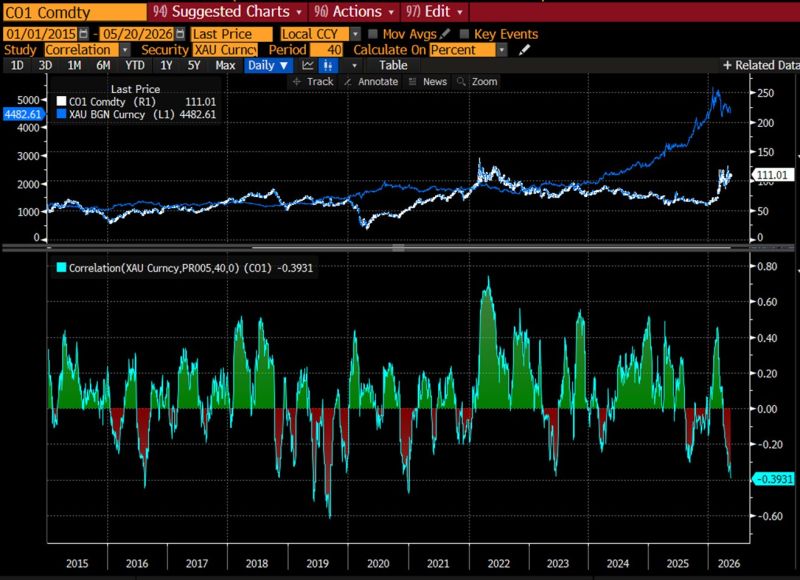

Since the start of the war, gold has been negatively correlated to oil. Oil up, gold down. Why? Because the marginal gold buyer is not the West, it is EM Asia and Turkey.

Higher oil prices crush import-dependent economies like India: Oil ↑ → Growth ↓ → Currency ↓ → Import costs ↑ → Gold demand ↓. That’s why gold has been weak despite geopolitical chaos. India is curbing gold imports to defend the Rupee. Turkey already burned reserves. China is temporarily balancing the system by cutting crude imports. The real story isn’t “gold vs fear.” It’s commodities, FX, and EM liquidity transmission. Mental flexibility > rigid macro views. Source: Alexander Stahel on X Bloomberg

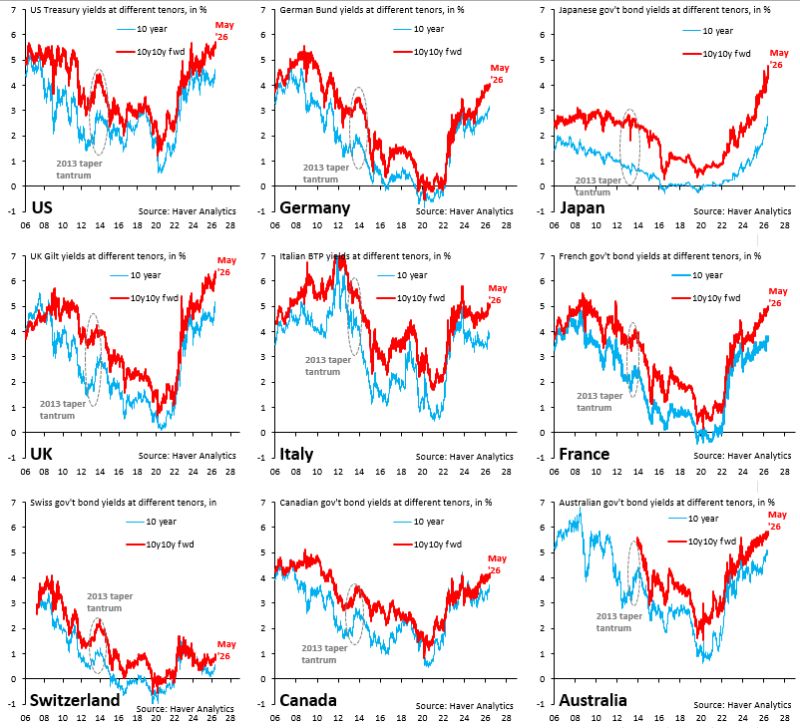

We've officially reached the "brutal" stage in the global bond market sell-off. The 10y10y forward yield (red) is making new highs all over the place.

Japan's 10y10y forward has risen 30 basis points in just a few days. Even Swiss 10y10y forward is rising. Source: Robin Brooks

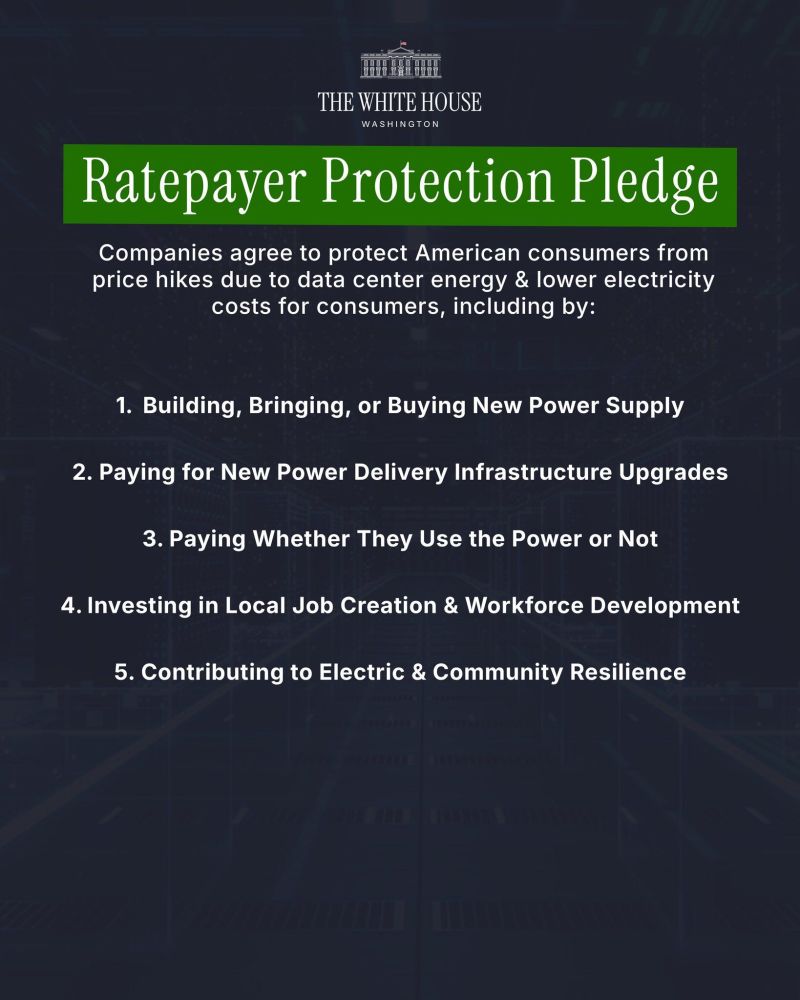

President Trump called on AI companies to build, bring, or buy 100% of the energy needed for their data centers as part of his “Ratepayer Protection Pledge.”

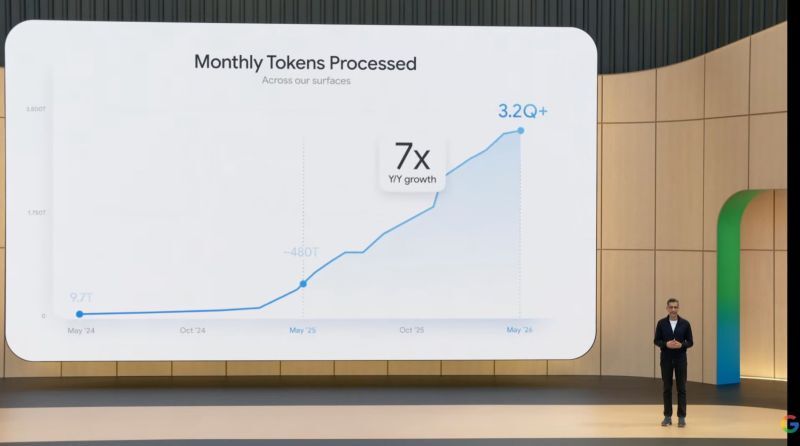

Monthly tokens processed across Google surfaces: May 2024: 9.7T May 2025: ~480T May 2026: 3.2Q+ That is 7x Y/Y growth. Source: Wall St Engine

GOOGLE JUST SHOWED HOW INSANE AI DEMAND HAS GOTTEN

Monthly tokens processed across Google surfaces: May 2024: 9.7T May 2025: ~480T May 2026: 3.2Q+ That is 7x Y/Y growth. Source: Wall St Engine

Stop using Claude like it's 2024.

Here are the 19 rules I follow when I use Claude: Source: AI evolution

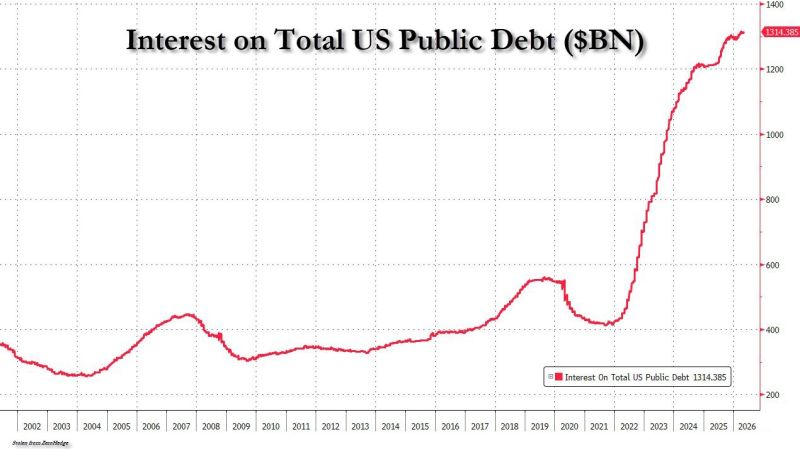

Here's why soaring yields do matter. Annual US interest expense is currently $1.3 trillion.

For context, the largest US government outlay is Social Security. It is $1.6 trillion. Source: zerohedge

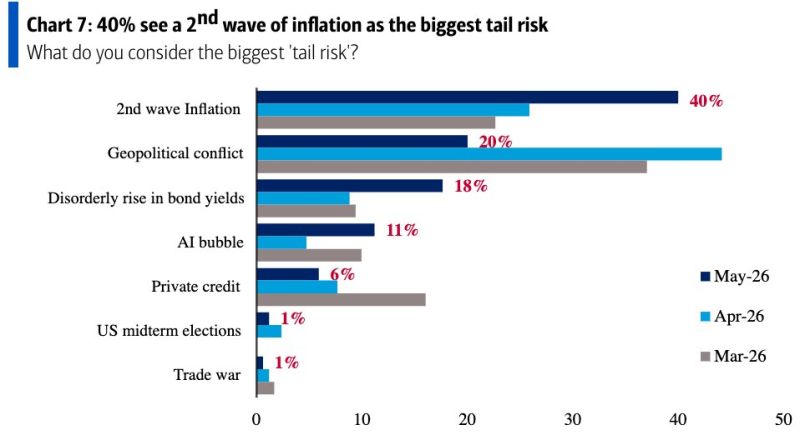

According to BofA fund manager survey, the biggest risk to stocks is a "second wave" of inflation.

Source: BofA

The "ultimate" hedge?

Gold followed the surge in Japanese rates throughout 2025. Gold started the year by materially overshooting the Japan 10-year, but we have since seen the Japanese long end explode higher and overshoot gold instead. Could this divergence finally trigger another squeeze higher in gold? Source: TME, LSEG