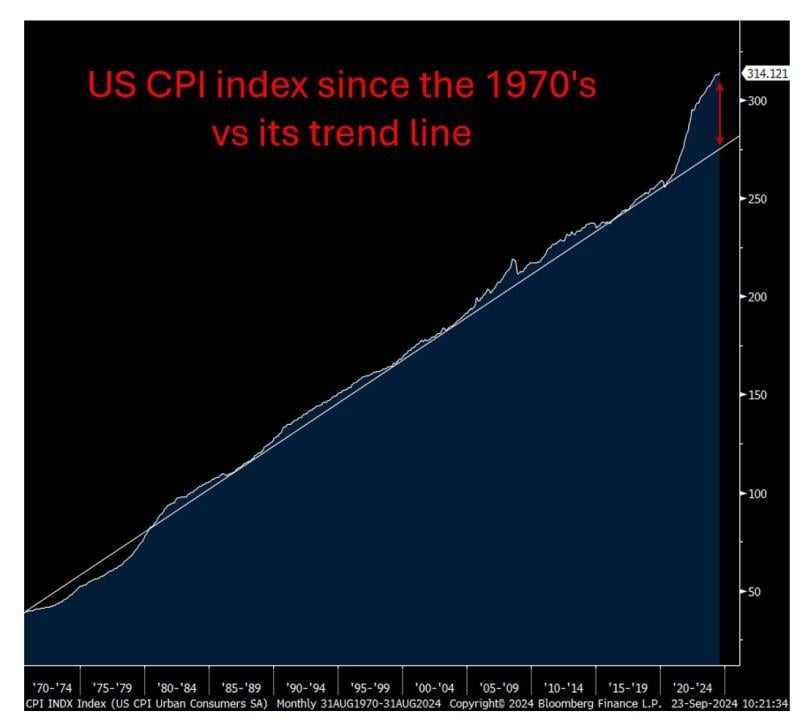

😱 The "shocking chart" of the day !!! 😱 US CPI index since the 1970's vs its trend line.

In order to 'average' out the recent period of high inflation at 2%, the fed would have to tolerate a period of time of deflation. But can they really afford deflation with $33T of debt and persistently high budget deficit? As mentioned by Peter Boockvar on X, once purchasing power is lost, it is lost forever because central bankers won't let you get it back... Last week, Federal Reserve Governor Chris Waller inadvertently made that perfectly clear when he spoke on Friday. He told CNBC in an interview that "What's got me a little more concerned is inflation is running softer than I thought."... Bottom-line: It is very unlikely that inflation will come back to trend line in the foreseeable future. Perhaps the jumbo rate cut was also about making sure that the US economy doesn't fall into a deflationary trap... Welcome to the era of fiscal dominance Source chart: Bloomberg

Prosus : Will It Be Able to Breakout This Time?

Prosus (PRX NA) has reached the major resistance zone between 35-37 for the 7th time since July 2021. Will it be able to breakout this time? Keep an eye out! Source: Bloomberg

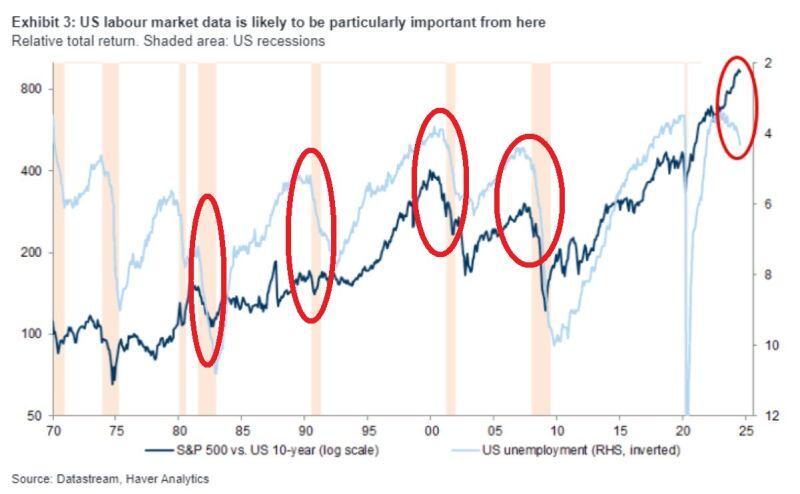

🚨US UNEMPLOYMENT RATE USUALLY RISES BEFORE THE S&P 500 CORRECTION🚨

US jobless rate rose from 3.4% in April 2023 to 4.2% in August near the highest in 3 years. In the past, when the unemployment rate was rising, the S&P 500 index saw significant declines. The us jobs reports in the coming weeks will be key... Source. Global Markets Investor

Don't stop. Keep going.

Source: Markets & Mayhem

Contrarian Investment

Source: The Investing for Beginners Podcast @IFB_podcast

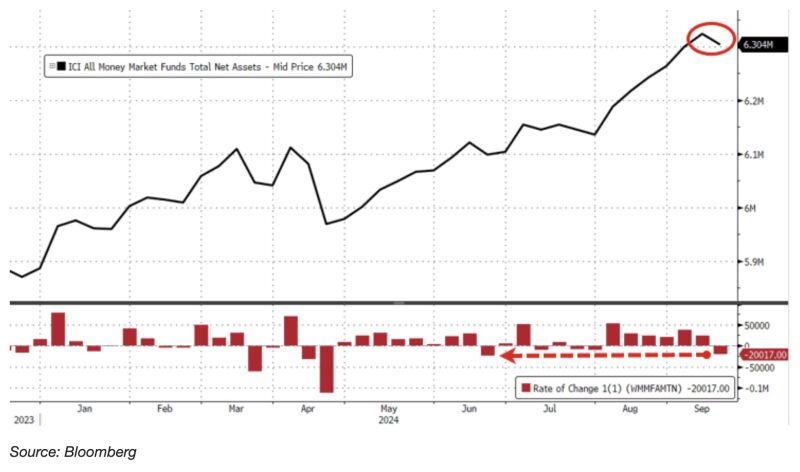

Money Market Funds saw a weekly outflow of $20 billion, the largest weekly outflow since June

Source: Barchart, Bloomberg

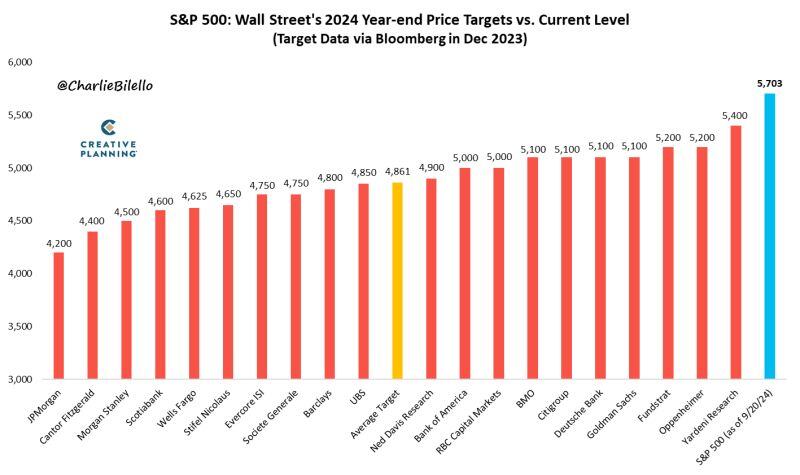

At 5,703, the S&P 500 is now over 300 points above above the highest 2024 year-end price target from Wall Street strategists and 17% above the average target (4,861).

And there's still 3 months to go in the year. $SPX Source: Charlie Bilello

How are the 'Magnificent 7' Tech stocks doing so far this year?

🟢 Nvidia Is Up +134.2% $NVDA 🟢 Meta Is Up +58.6% $META 🟢 Amazon Is Up +26.1% $AMZN 🟢 Apple Is Up +18.5% $AAPL 🟢 Alphabet Is Up +16.8% $GOOGL 🟢 Microsoft Is Up +15.7% $MSFT 🔴 Tesla Is Down -4.1% $TSLA Note that S&P 500 and Nasdaq are both up +19.6% YTD