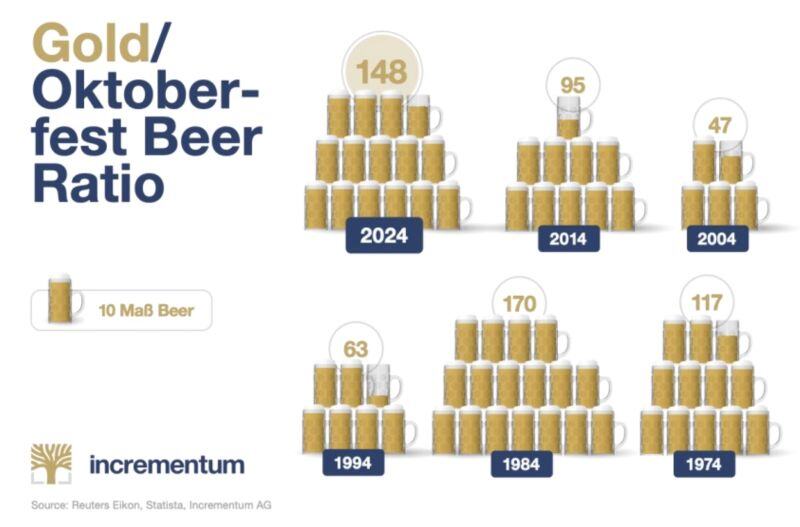

Ahead of Oktoberfest... Life is all about liquidity!

Source: Ronald-Peter Stoeferle, CMT, CFTe, MSTA, Incrementum AG

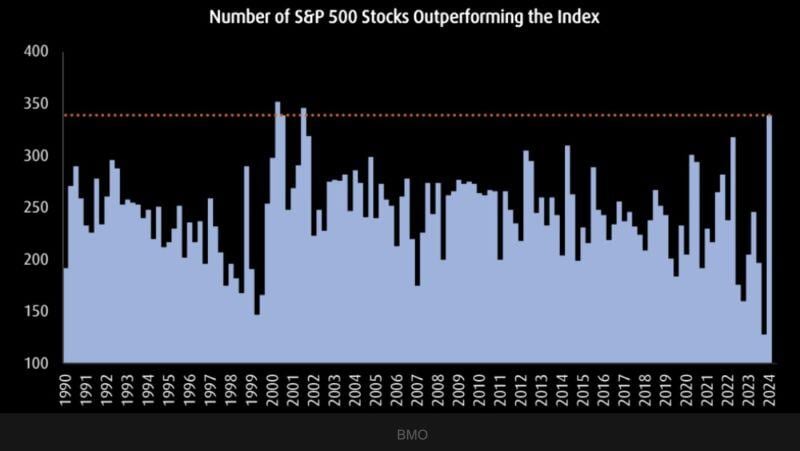

The number of sp500 stocks outperforming the index is the highest since 2002.

Source: Barchart, BMO

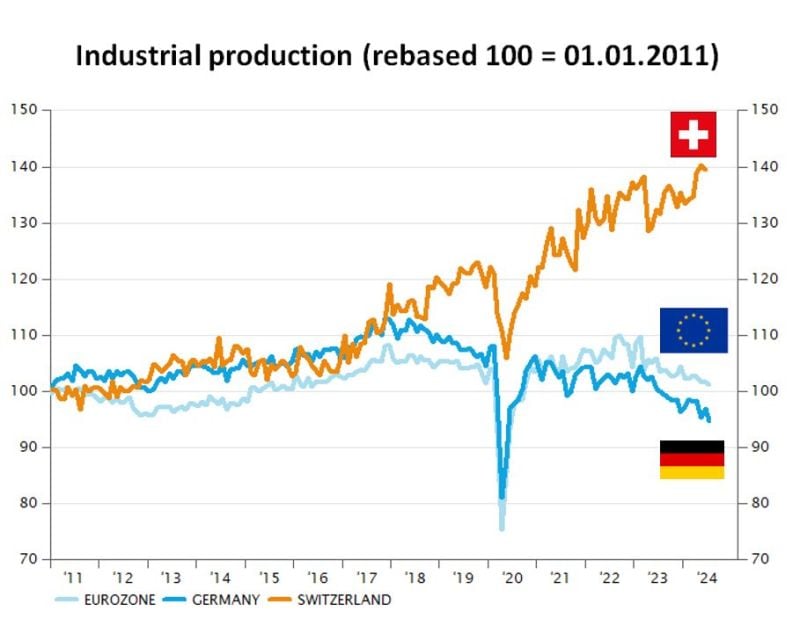

😱 The "shocking chart" of the day !!! 😱

Since 2011, the swissie is up more than 25% against euro. Despite this, industrial production growth in switzerland has INCREASED by 40% while it has DECREASED by 5% in germany and is roughly flat in the eurozone. Note the huge trend divergence since covid... HOP SCHWEIZ ! Source: Syz research

Gold has shown a remarkable surge, nearly quadrupling from $600 to $2,000 per ounce in just six years following the Fed's easing in 2007.

On the chart below, the green line is representing the Fed Funds rate - INVERTED, and the yellow line is depicting gold price. Additionally, the white line comparing Gold vs. S&P 500 indicates a potential turnaround after a prolonged period of underperformance. Could the recent outperformance by gold signify the start of a new trend? Source: Bloomberg, Garret Goggin

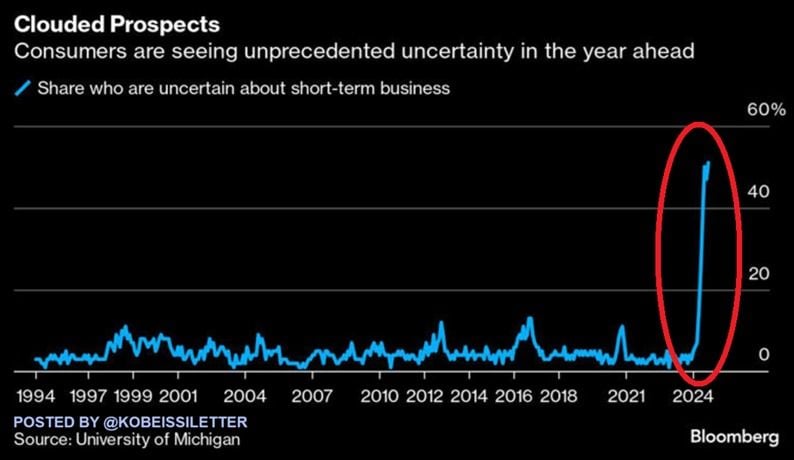

Americans have never been so worried about the year ahead:

The share of consumers uncertain about business conditions over the next year spiked to 51% in September, the most on record. The percentage has DOUBLED in 4 months. Over the last 30 years, the share of consumers concerned about short-term business prospects has never been so high. Americans have been hit by historically high costs of living, elevated borrowing costs, and the deteriorating job market. US households are struggling. Source: The Kobeissi Letter

US yieldcurve keeps steepening...

Source: Bloomberg, HolgerZ

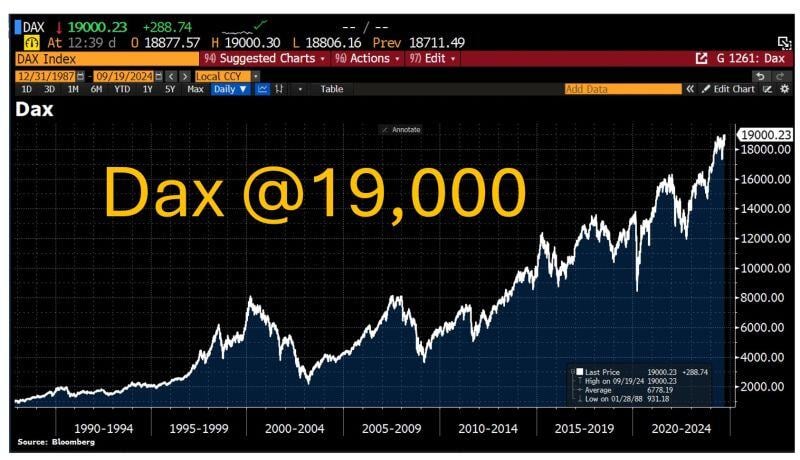

In case you missed it... While the german economy is struggling, the stock market doesn't care...

Germany's blue-chip index Dax jumped >19,000 points for the first time after Fed's jumbo rate cut. Source: HolgerZ, Bloomberg

BlackRock Reveals It’s Quietly Preparing For A $35 Trillion Federal Reserve Dollar Crisis With Bitcoin—Predicted To Spark A Sudden Price Boom

As fears swirl the U.S. dollar is on "the verge of a total collapse," the world's largest asset manager BlackRock has warned of "growing concerns" around the spiraling $35 trillion U.S. debt pile that's predicted to drive "institutional interest in bitcoin." "The growing concerns in the U.S. and abroad over the state of U.S. federal deficits and debt has increased the appeal of potential alternative reserve assets as a potential hedge against possible future events affecting the U.S. dollar," BlackRock's exchange-traded fund (ETF) chief investment officer, its head of crypto and its head of fixed income global macro wrote in a paper outlining the investment case for bitcoin. "This dynamic appears to be also taking hold in other countries where debt accumulation has been significant," the authors of the BlackRock paper added. "In our experience with clients to date, this explains a substantial portion of the recent broadening institutional interest in bitcoin." BlackRock, which has around $10 trillion in assets under management, described bitcoin as a "unique diversifier" to hedge against economic and political risk. "While bitcoin has shown instances of short-term co-movements with equities and other 'risk assets,' over the longer term its fundamental drivers are starkly different, and in many cases inverted, versus most traditional investment assets," the paper concluded. Source: Forbes Digital Assets >>> https://lnkd.in/ePufVM9J