🚨WHAT? US stocks fell after a 0.50% rate cut?🚨

Markets were very mixed after the Fed 'Jumbo' reduction. Big cuts are not usually a good sign BUT... Day 1 is usually not the REAL reaction. We need to wait 2 more trading sessions to see what's really going on. Market performance today: S&P 500 -0.3% Nasdaq -0.3% Russell 2000 +0.0% Dow Jones -0.3% Bitcoin +0.1% Bank Index +0.4% VIX +4%, front month futures VIX -1% Gold -0.6% WTI Crude Oil -1.3% Source. Global Markets Investor

Live look at JP Morgan after being the only ones who correctly predicted a 50bps cut:

Source: Trend Spider

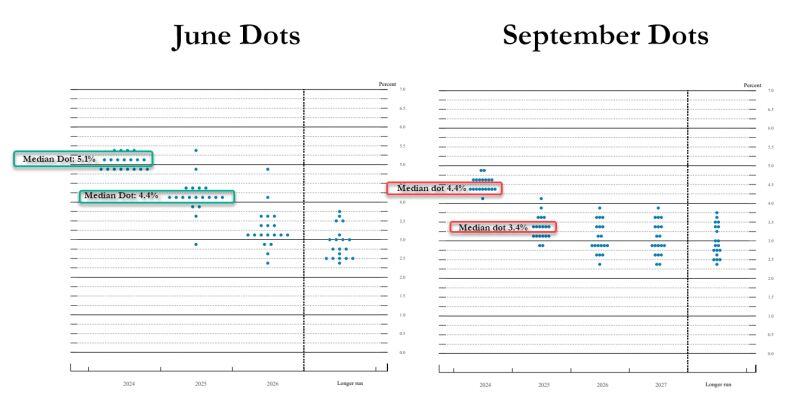

Amazing to see the effect of 818K downward jobs revision on the fed dots...

Source: www.zerohedge.com

Among the reasons why the Fed cut 50bps this week:

1) Inflation risk is LOWER than Employment and Consumer risk 2) The sticky component of inflation is shelter. For shelter inflation to go down we need to see more housing supply and for this we need to get lower mortgage rates = jumbo rate cut does help 3) They MUST get front-end rates lower as this colossal wall of debt matures (source: Lawrence McDonald, Bloomberg)

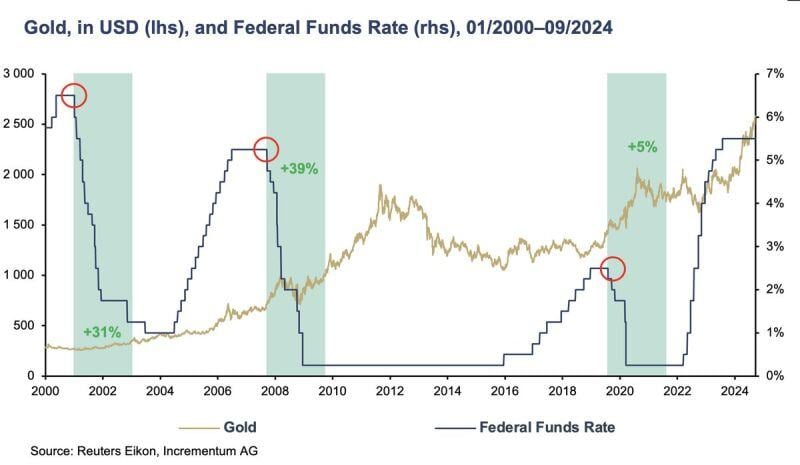

gold after Fed rate cuts

Source: Incremetum AG

Here she is...

Source: Barchart

The former president had in February said Federal Reserve chair Jay Powell, a registered Republican, would cut interest rates to 'help the Democrats'.

https://on.ft.com/3B5Eg0O

BlackRock just put out a nine-page white paper that makes case for bitcoin ETF as a "unique diversifier" that can hedge against fiscal, monetary and geopolitical risks

also including section called "bitcoin's path to $1 trillion market cap". Read whole thing here: https://lnkd.in/e8XVW9gG Source: Blackrock