16 Jul 2026

A tiny group of Americans now owns wealth equivalent to nearly 12% of all the national income generated in the United States in a single year

Source: FT

15 Jul 2026

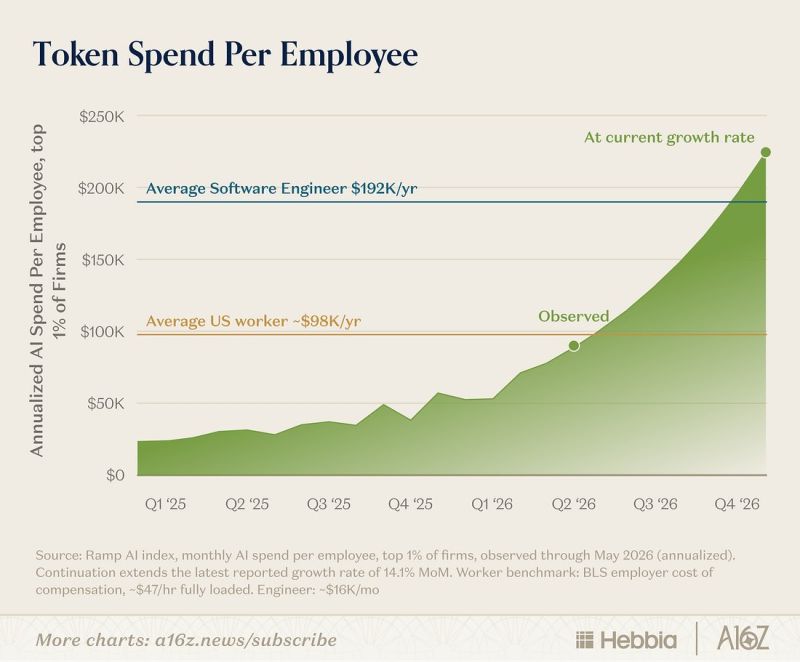

At the top 1% of AI-spending firms, AI spend per employee is on track to exceed average software-engineer pay by the end of the year.

Source: Hedgeye

15 Jul 2026

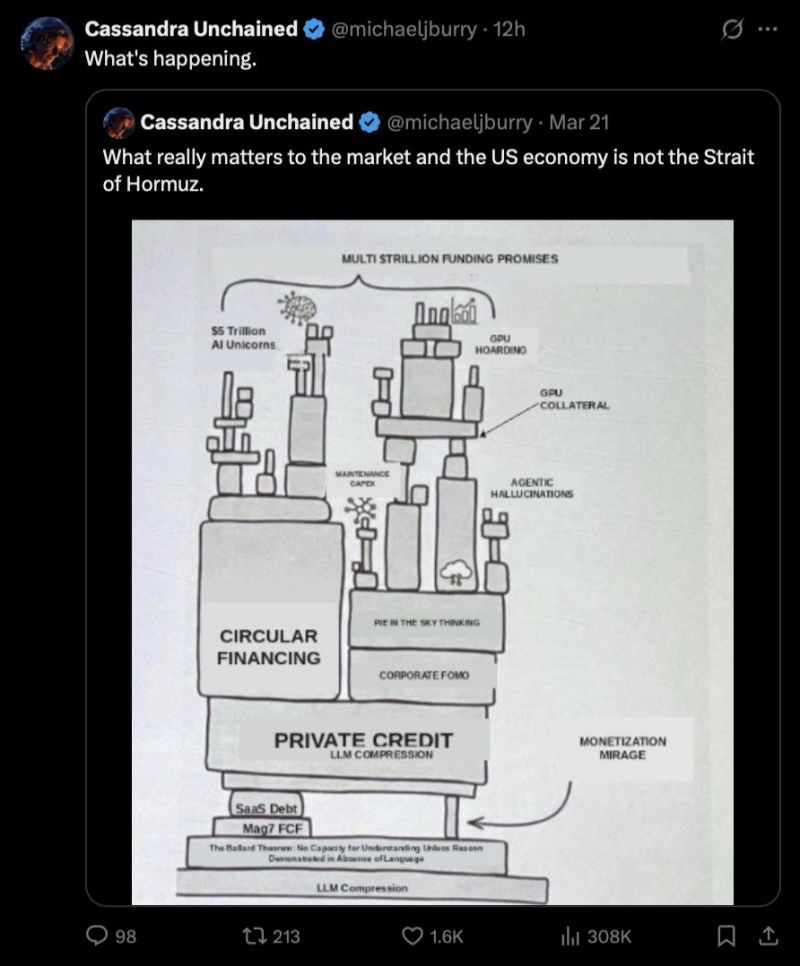

Michael Burry says the AI boom isn't funded by real demand

It's a loop cycle: borrow money, buy GPUs, use GPUs as collateral, borrow more money, repeat. Source: Michael Burry Stock Tracker ♟ @burrytracker

15 Jul 2026

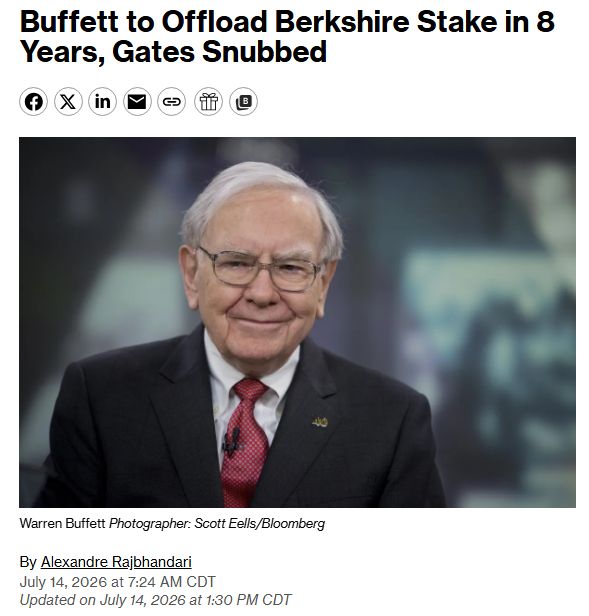

Warren Buffett will no longer be gifting shares of Berkshire Hathaway to the Bill Gates Foundation 🚨 🚨

Source: Barchart

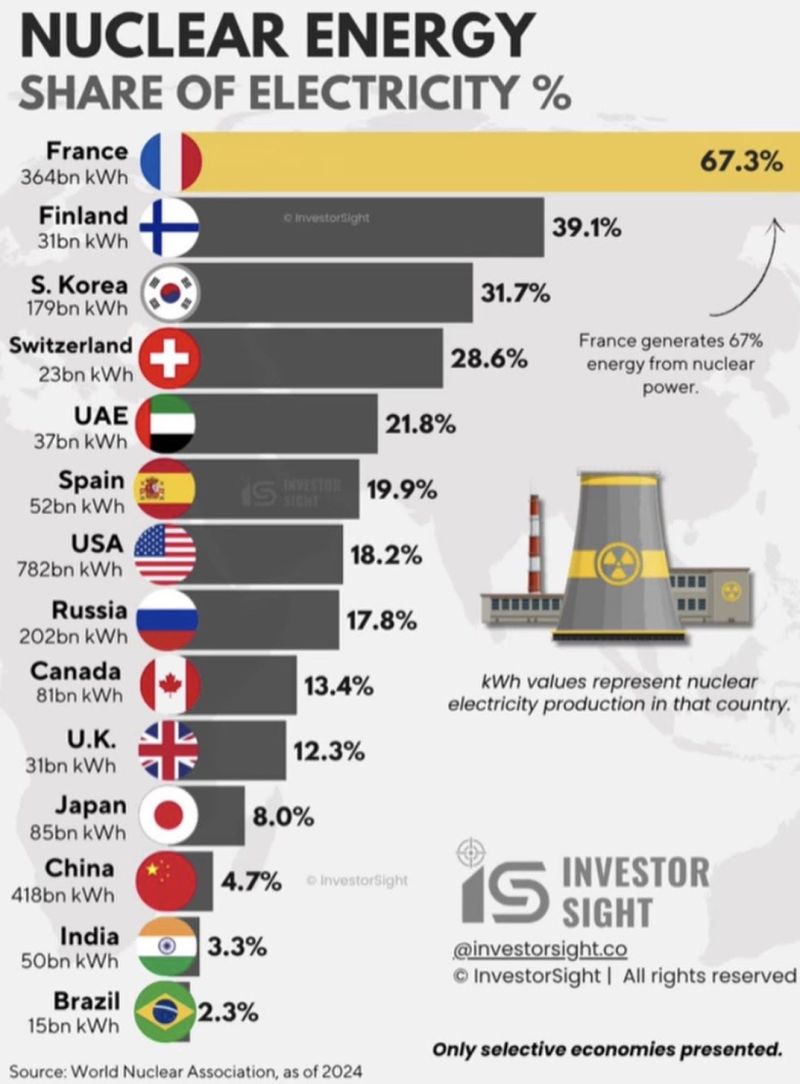

13 Jul 2026

France generates 67% of its electricity from nuclear power, the highest share of any major economy.

Extreme heat just forced 3 reactors offline and cut output at 8 more. That gap gets filled by gas. Right when European gas markets are already stretched. Source: Jack Prandelli on X

13 Jul 2026

VAR intervention rate per 100 fools

Source: The Footy Feed

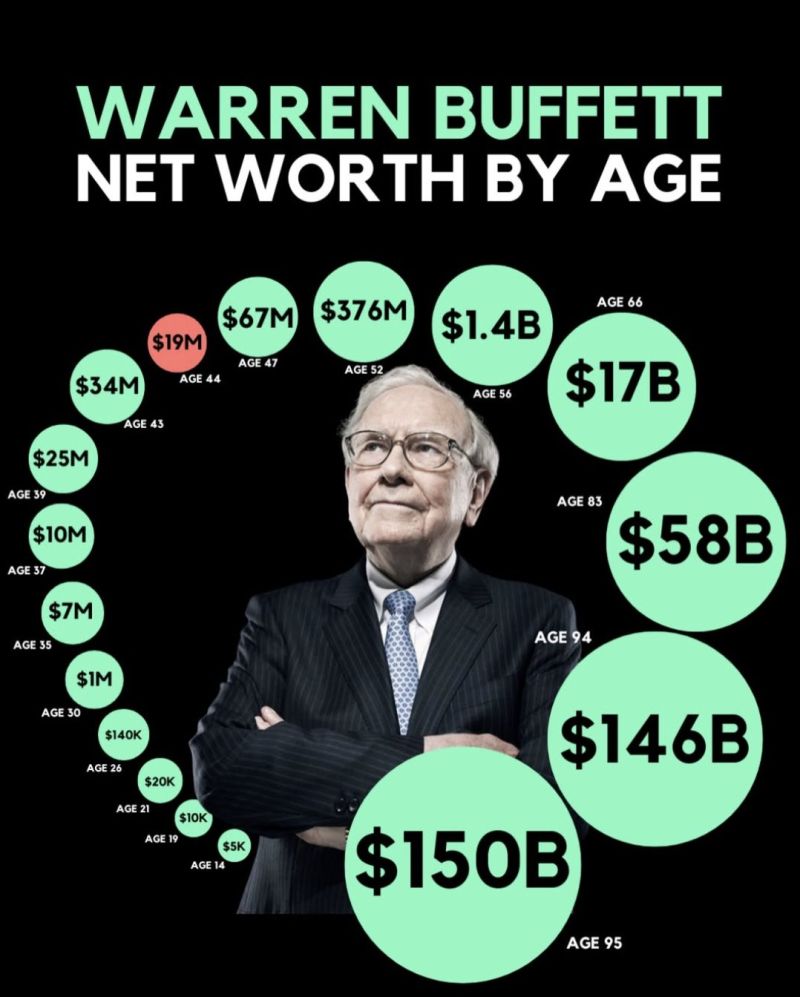

10 Jul 2026

Buffett never caught a 100x.

His whole 60 year record averages 19.9% a year. The most boring number on this chart built on of the richest investors alive. Source: Rand Group

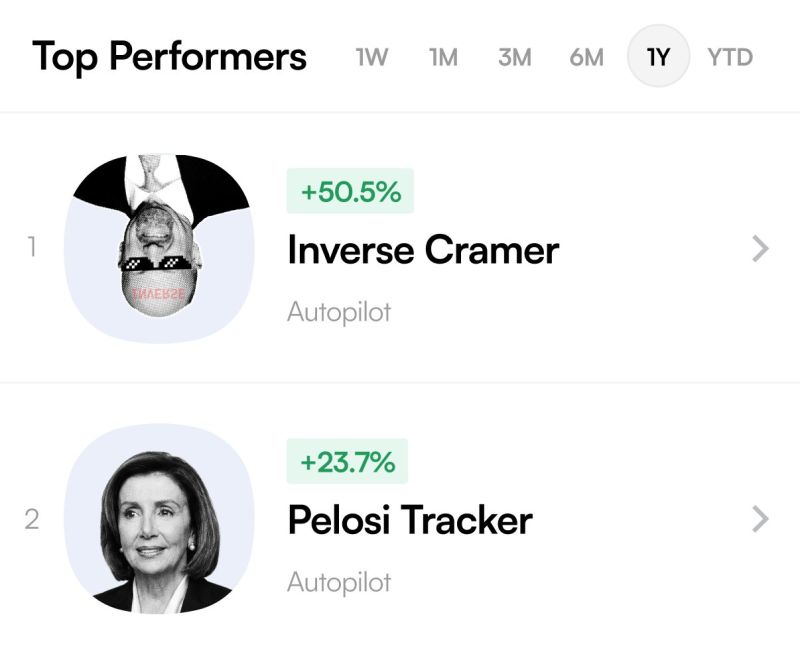

9 Jul 2026

What a legend

Source: Nancy Pelosi Stock Tracker ♟ @pelositracker