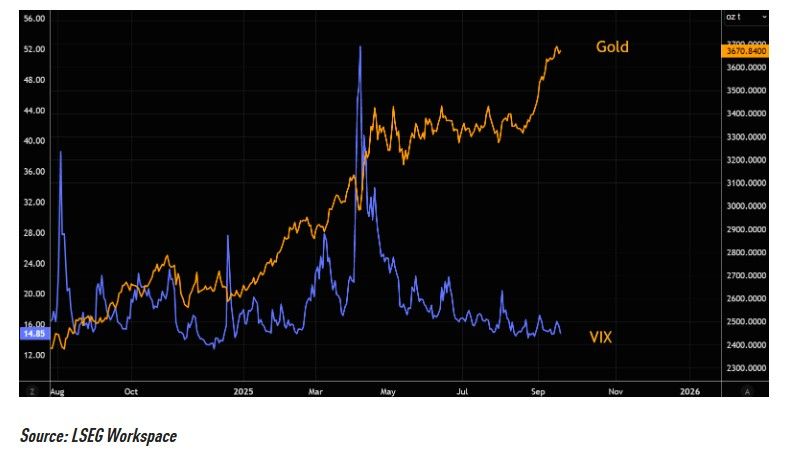

The hedge factor

Gold is the "everything hedge", but if you are looking for global equity hedges, then VIX looks relatively more interesting compared to chasing gold here. Source: TME, LSEG

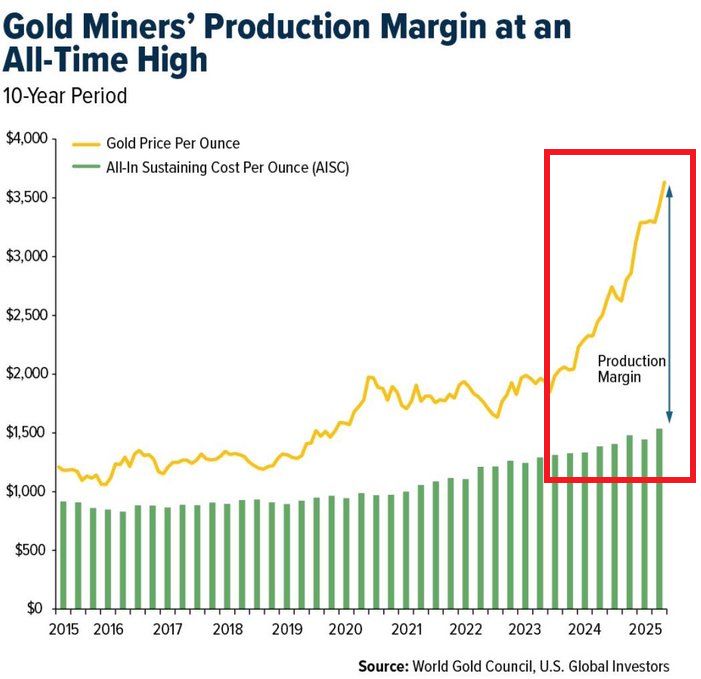

Gold miners are making record profits:

Production margins are at an all-time high as gold prices surge while costs rise much slower. Miners are now earning more per ounce than ever in the past 10 years. Meanwhile, gold miners ETF, $GDX, has skyrocketed 103% year-to-date. Source: Global Markets Investor

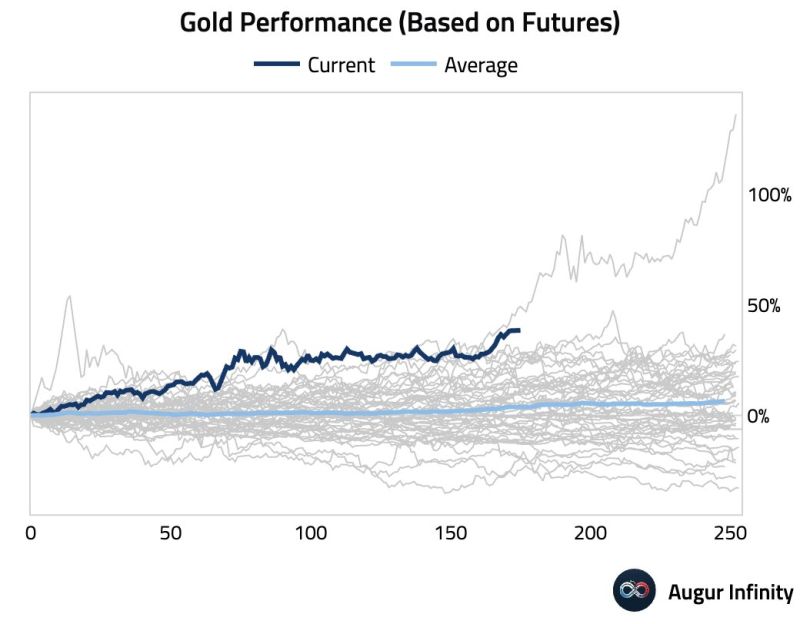

The YTD performance of gold is the best since 1979

Source: Augur Infinity

Interesting theory...

The Shanghai Gold Exchange (SGE) has activated two overseas vaults—one in Saudi Arabia, the other in Hong Kong—marking a direct expansion of RMB-denominated gold trading beyond mainland borders. This move represents a strategic move to enhance China’s gold trading infrastructure and strengthen the SGE’s role in global gold price discovery. These aren’t symbolic moves. They’re operational. They’re live. Source: Alasdair Macleod @MacleodFinance

A golden year so far...

Source: GoldSilver HQ

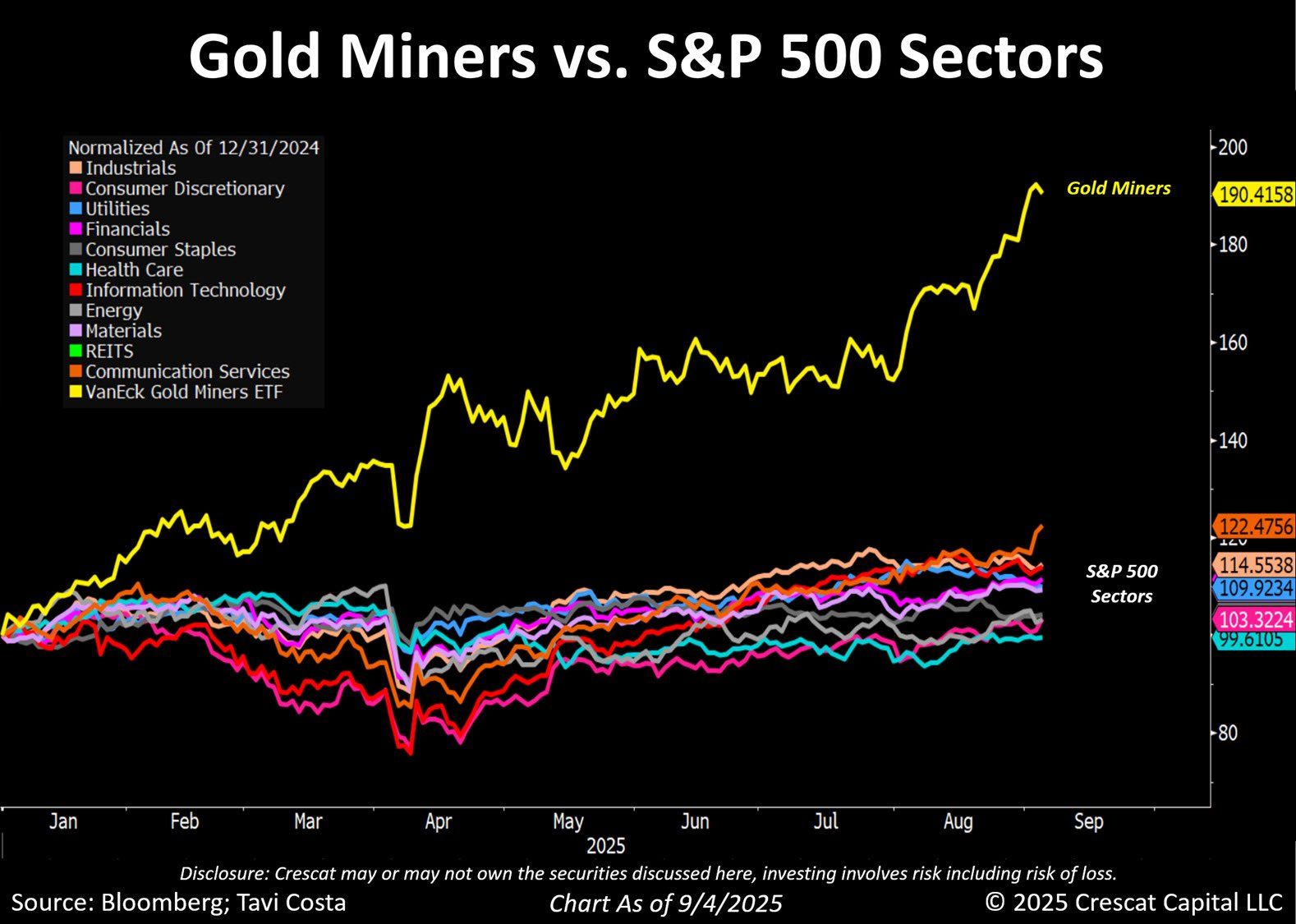

Gold stocks have crushed every sector of the S&P 500 this year

Source: Tavi Costa, Bloomberg

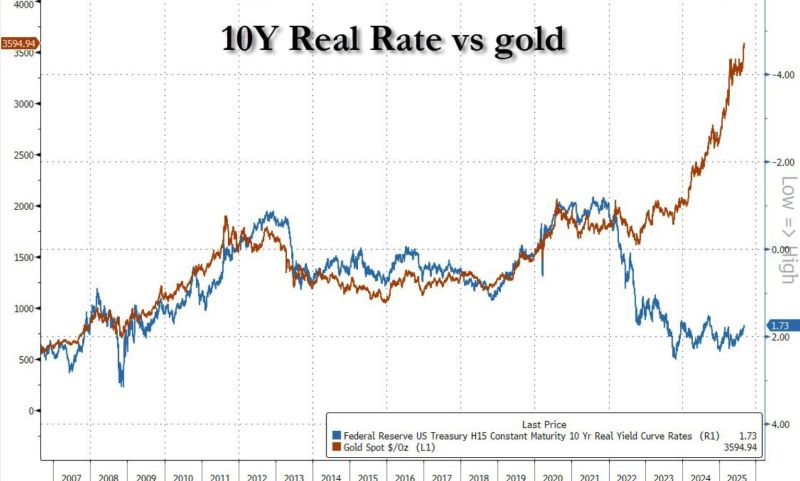

"The Ukraine war and the weaponization of the dollar was the straw that broke the camel's back"

Source: zerohedge

Will Silver be next?

Source: Trend Spider