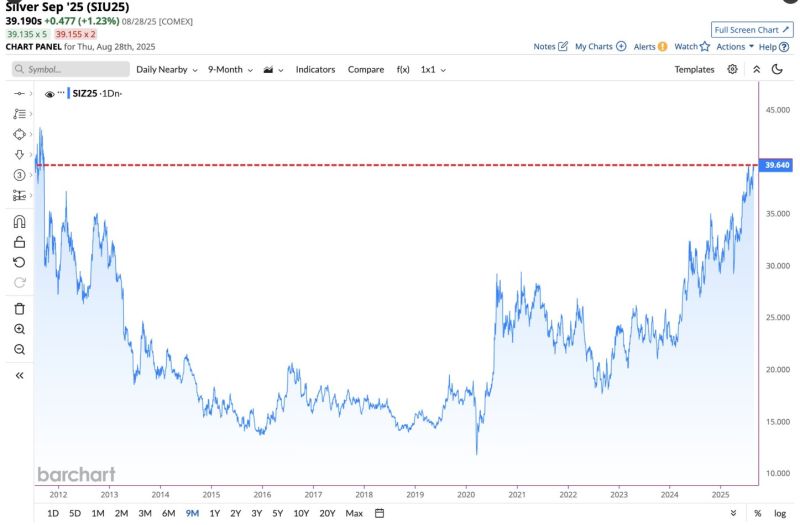

In case you missed it... silver hits highest closing price in almost 14 years 📈📈

Source: Barchart

Belated "Nixon closing the gold window anniversary" post

SPX priced in gold (blue) v. SPX priced in USD (red) since August 1971 when Nixon closed the gold window. Source: Luke Gromen @LukeGromen

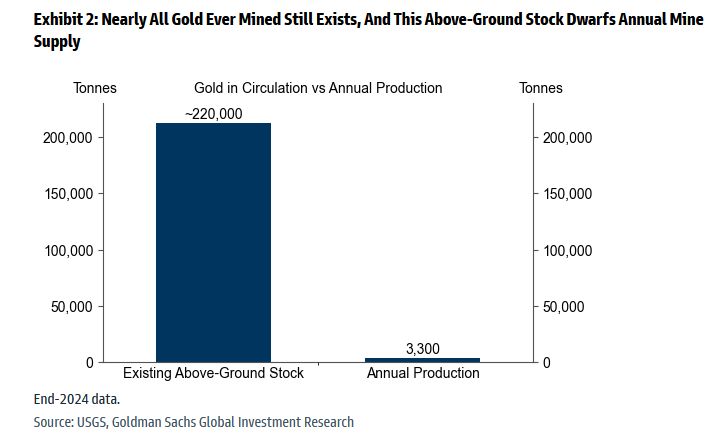

Gold is unlike other commodities – it is not consumed; it is stored.

Nearly all gold ever mined – about 220,000 tonnes – still exists, and this above-ground stock dwarfs annual mine supply. - From Goldman's primer on gold Source: zerohedge

Gold ETFs Breach 92 Million-Ounce Threshold

Bloomberg's measure of total gold ETF holdings jumped to a two-year high. At 92.7 million ounces on Aug. 15, my graphic shows this metric surpassing the 92 million threshold first reached in 2020, but with a big difference - stock market volatility was rising then. Source: Mike McGlone, Bloomberg

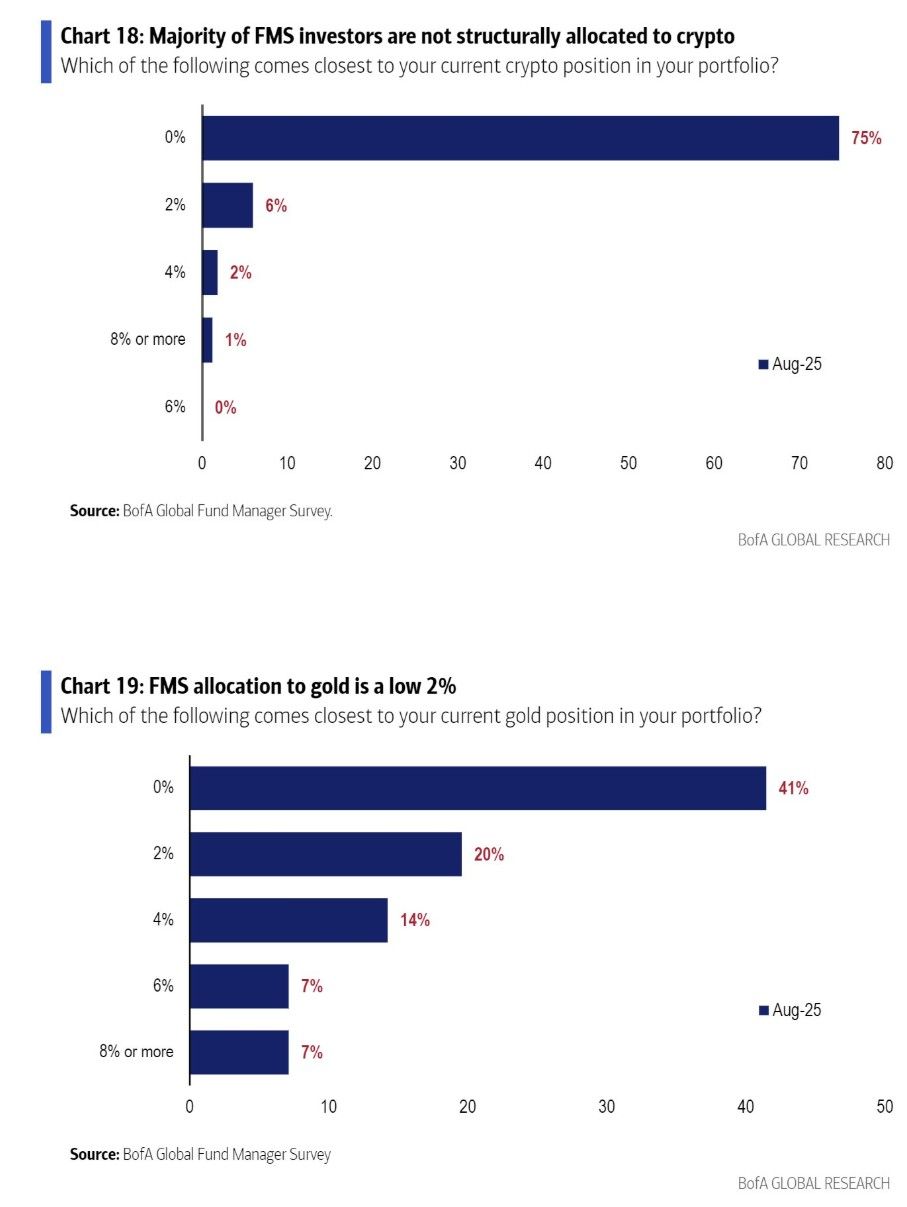

The average professional fund manager allocation toward crypto is 0.3% of AUM.

75% of Fund Managers have ZERO allocation. BofA's Hartnett: "Raise Allocations To Gold And Crypto Because Yield Curve Control Is Coming" Source: BofA

What looks like gold going up is really the dollar going down.

Source: Mr. Uppy @MisterUppy

It is often a very good sign when you see strong momentum & trend in a sector / segment of the market while fund flows are lagging.

This has been the case for gold miners (e.g VanEck Gold Miners ETF $GDX) - see chart below. We've seen the first significant inflow in the GDX in the last six months. Despite the great GDX performance of 45+% during this period, six-month net flows are still very negative at -$2.54B. 🪙👇 Source: Oliver Groß @minenergybiz

Incredible charts by BofA...

Bitcoin and gold are the two best best performing assets YTD and over the last few years... However, fund managers are massively under-exposed to those 2 store of values... Indeed, 75% of fund managers have no exposure at all to cryptos. And even more surprisingly, 41% of fund managers have no exposure at all to gold... The least we can say is that they don't look as crowded trades... Source: BofA thru Callum Thomas