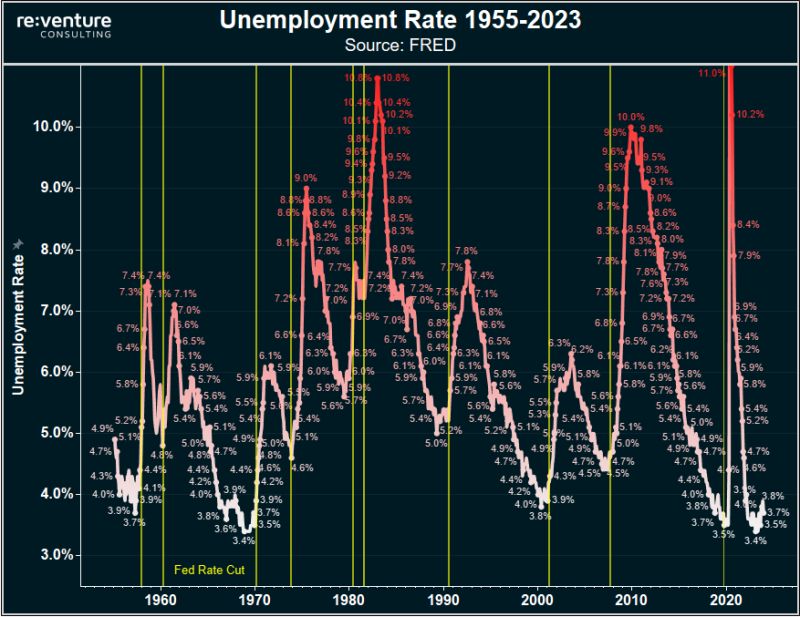

Unemployment rate in America from 1955-2023

Interesting how the unemployment rate tends to spike right after the Fed cuts rates. Suggesting that Fed policy easing is usually a negative signal for the economy. Not a positive one. Source: FRED, re:venture

What a journey for Ireland...

Ireland has experienced unprecedented growth in prosperity in recent years. GDP per capita is now almost $100k, which is more than twice as much as in Germany and three times as much as in Italy. The small country with a population of 5 million has benefited from the large investments made by tech giants, who have settled here b/c of the low tax regime. No other country in Europe has a meaningful budget surplus, can set up 2 sovereign wealth funds, (Future Ireland Fund (FIF) and a smaller Infrastructure, Nature and Climate Fund (INCF) and has a war chest of €2.5bn before 3 important elections. Source: Bloomberg, HolgerZ

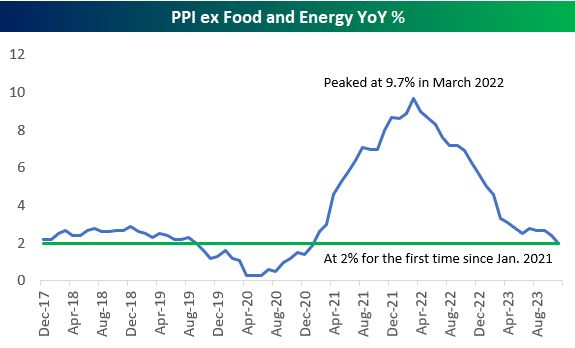

Up the mountain and back down in the valley

Here's a look at the year-over-year percentage change of PPI (producer prices) ex food & energy over the last five years. Core PPI is back down to 2% for the first time since January 2021 after topping out at 9.7% in March 2022. Source: Bespoke

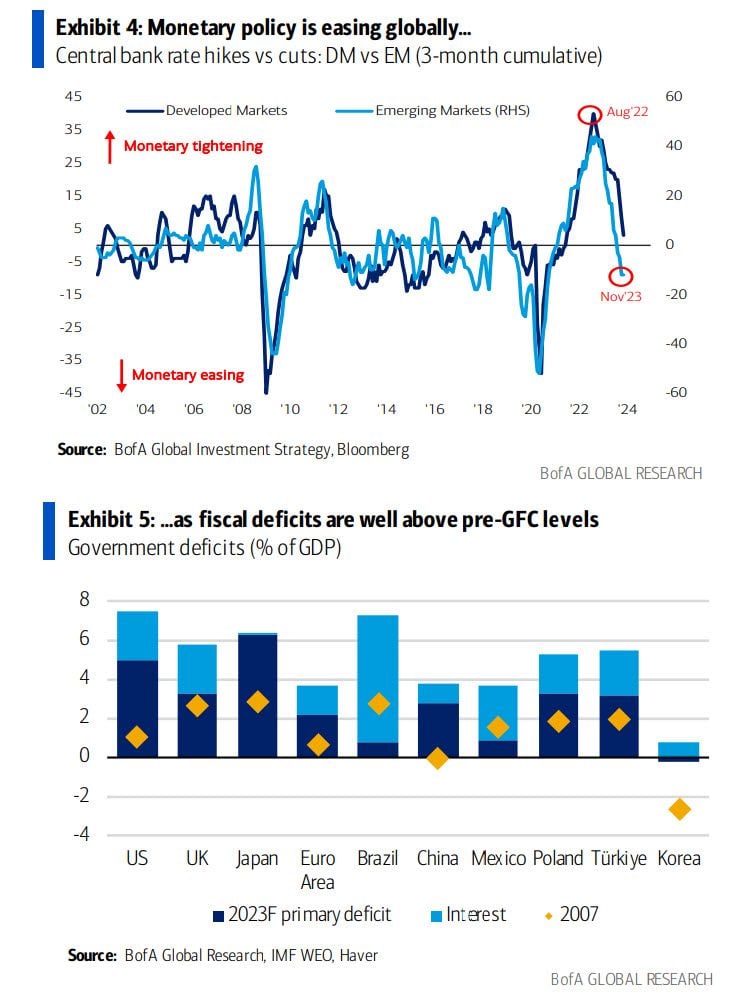

Monetary policy is now easing globally - and will ease much more in 2024/25 - at a time when fiscal deficits are far above the global financial crisis levels

Source: BofA

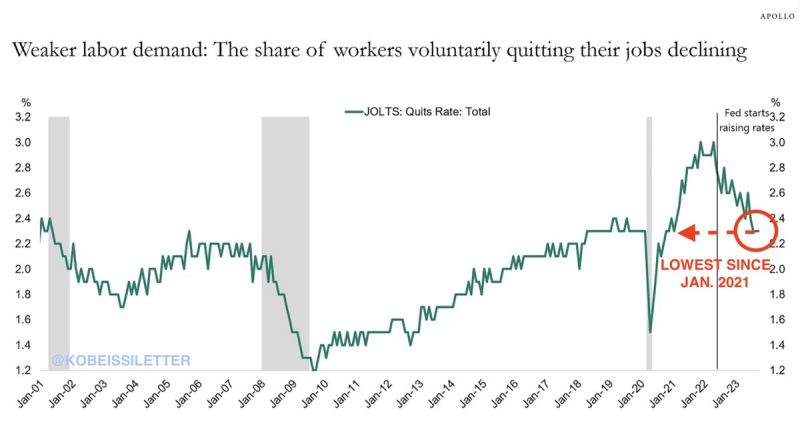

The share of workers voluntarily quitting their jobs is down to 2.3%

This is the lowest since January 2023 and down from 3.1% prior to the Fed started rate hikes. Weaker labor demand will be the theme of 2024 as job growth slows and rates stay higher for longer. Furthermore, as excess savings have now been depleted, consumers are more reliant on holding a job. Source: The Kobeissi Letter

A slightly disappointing US CPI inflation numbers for the markets...

US YoY CPI eased to 3.1% in November from 3.2% while the important core reading was unchanged at 4% YoY, despite seeing the MoM tick a bit higher. The so-called super-core, a measure watched by the Fed, meanwhile rose at one of the fastest monthly paces this year.

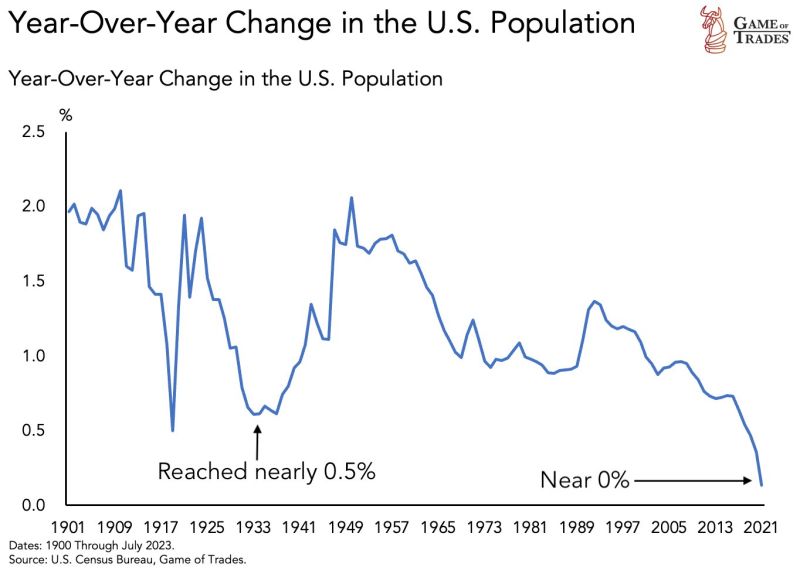

US population growth has fallen off a cliff. Nearing 0% levels indicating almost NO growth. Current levels have NOT been seen in 100+ years

Source: Game of Trades

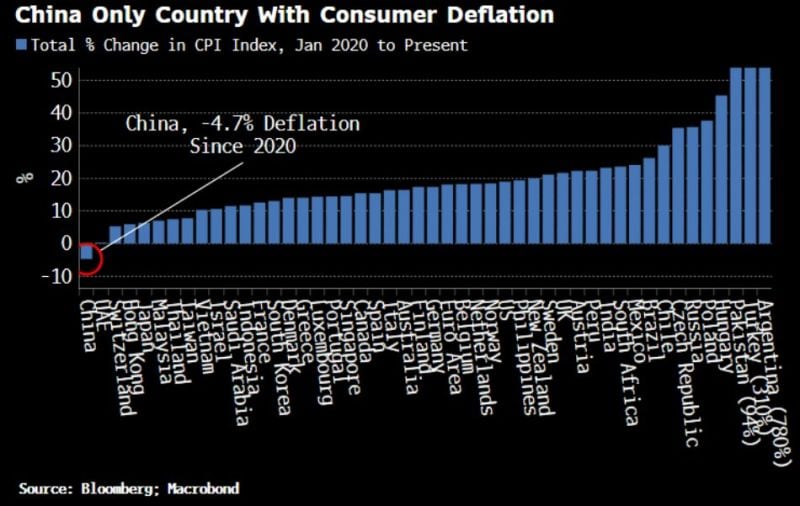

China is the only country experiencing deflation

CPI is down 4.7% since 2020 while every other country has experience inflation – some experiencing the highest in decades. Source: Genevieve Roch-Decter, CFA, Bloomberg, Macrobond