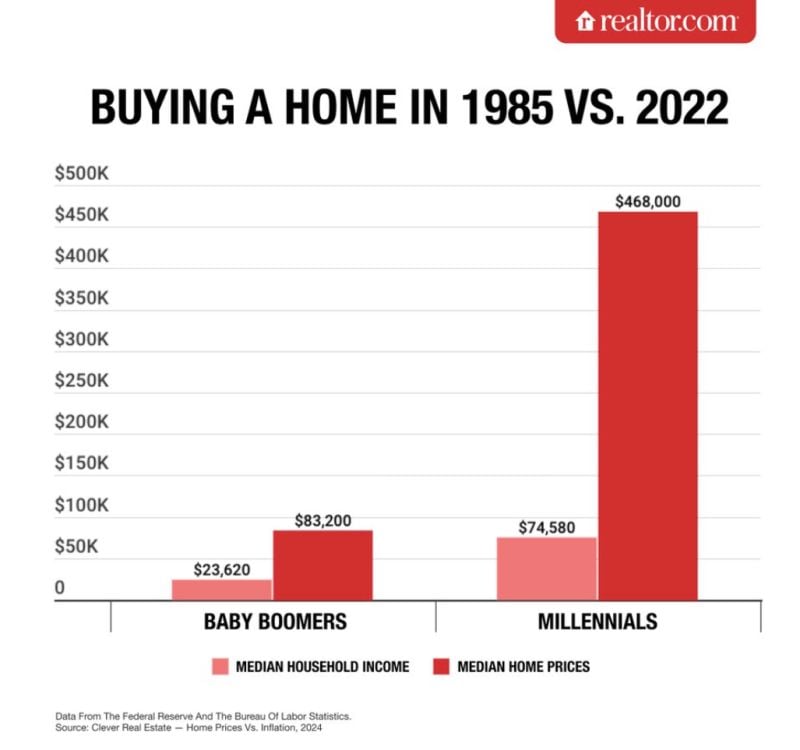

Want to buy a home?

1980: save for a couple years 2024: forget about it Source: Michael Burry Stock Tracker

The cost of servicing US government debt is on course to surpass defense spending

Source: Bloomberg, Michael McDonough

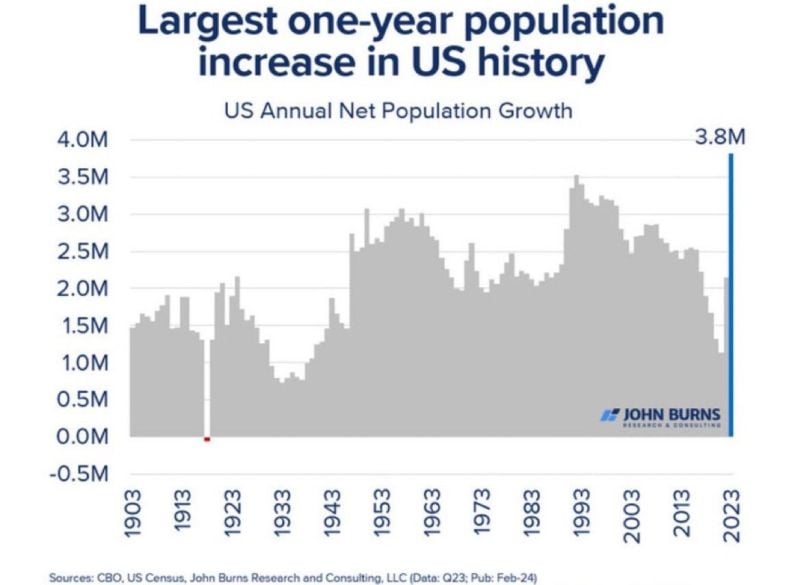

US Demographics

.

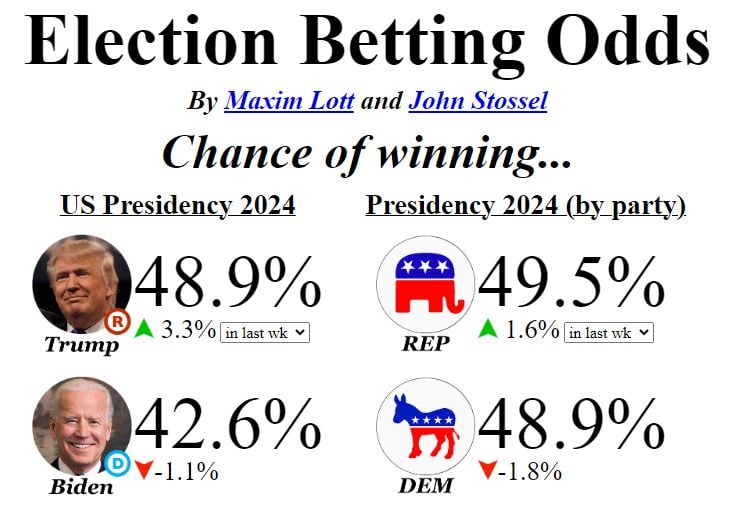

We've seen a pretty big move in Presidential betting odds over the last week

Trump now holds a 6.3 point lead on Biden and Republicans are now on top in the generic head to head. From @maximlott at https://lnkd.in/dT6EHQvp thru bespoke

SUMMARY OF FED CHAIR POWELL'S COMMENTS (5/14/24):

1. "Overall a good picture looking at US economic data" 2. Inflation was notable in Q1 for the lack of further progress 3. Housing inflation has been a bit of a puzzle for the Fed 4. Restrictive policy may take longer than expected to lower inflation 5. Unlikely the Fed's next move will be an interest rate hike 6. "Credibility is everything for central banks" Source: The Kobeissi Letter

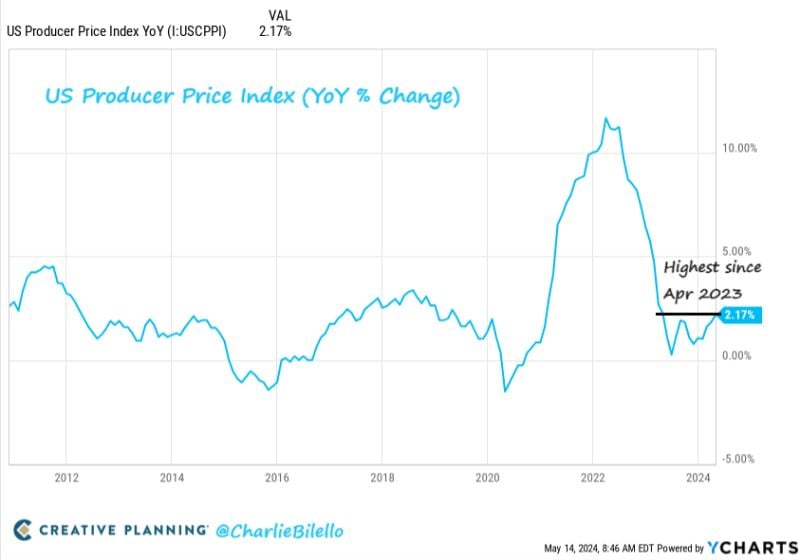

BREAKING: April PPI inflation RISES to 2.2%, in-line with expectations of 2.2%

Core PPI inflation was 2.4%, in-line with expectations of 2.4%. PPI inflation is now up for 3 straight months for the first time since April 2022. This is the highest PPI reading since April 2023. Note that revisions from last month’s PPI left people feeling it wasn’t as “hot” as initially thought on headline numbers. Source: Charlie Bilello

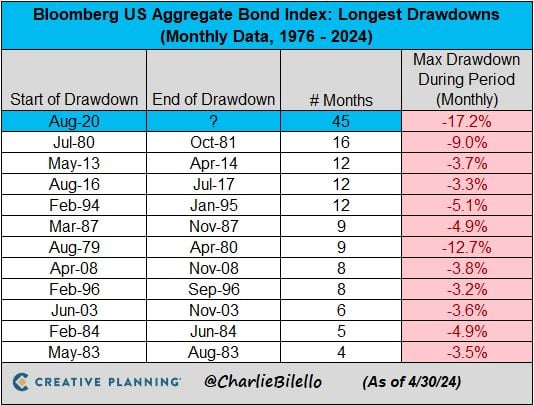

The US Bond Market has now been in a drawdown for 45 months, by far the longest bond bear market in history

Source: Charlie Bilello

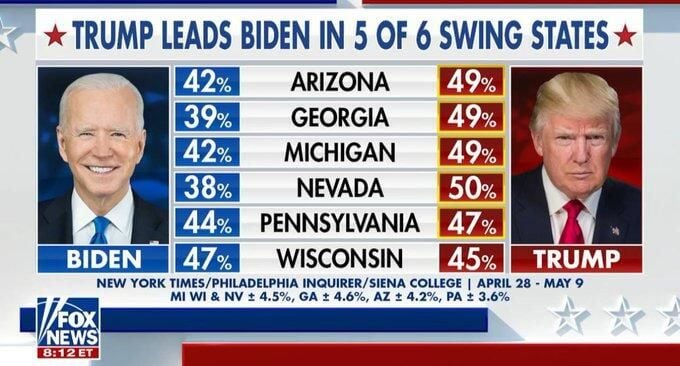

A new set of polls reveals that Donald Trump is leading President Biden in five out of six critical battleground states

as young and non-white voters grow increasingly dissatisfied with the current president. Source: www.zerohedge.com, FoxNews