16 Jul 2026

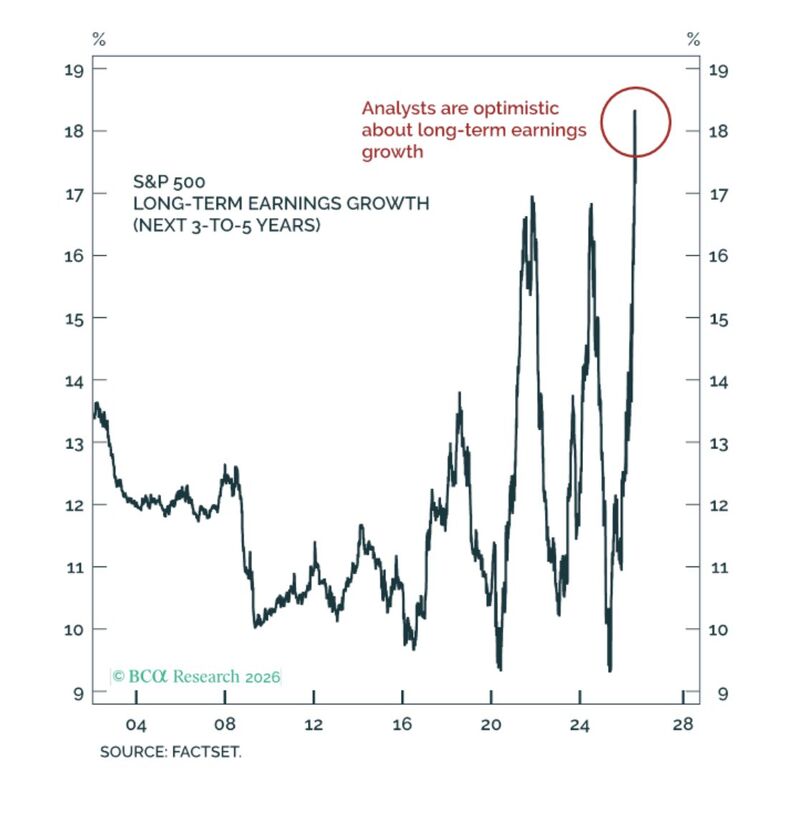

Peak optimism?

Source: Peter Berezin

16 Jul 2026

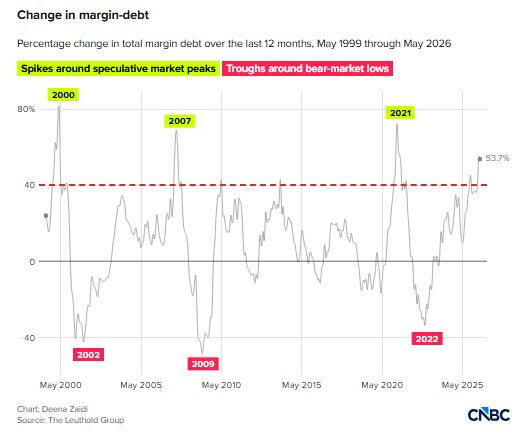

Total Margin Debt has increased by more than 40% over the last 12 months

A level only seen at prior market tops, including the Dot Com Bubble and the Global Financial Crisis Source: Barchart, CNBC

16 Jul 2026

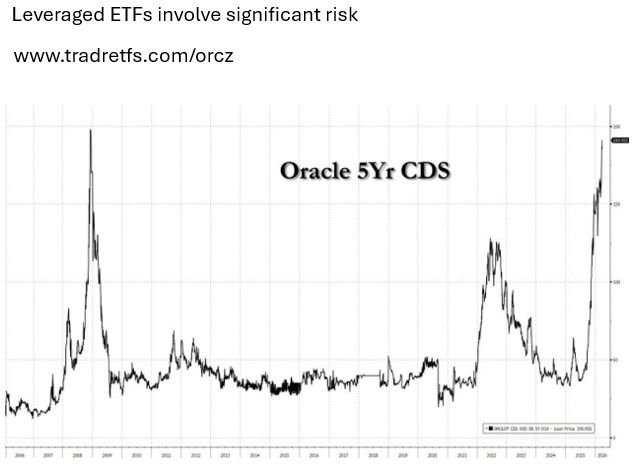

Oracle's credit risk soared earlier this year to its highest level since the Dot Com Bubble

Source. zerohedge, Barchart

15 Jul 2026

One-year inflation swaps fall below 2% for the first time since 2024 !!!

Source: Hedgeye

15 Jul 2026

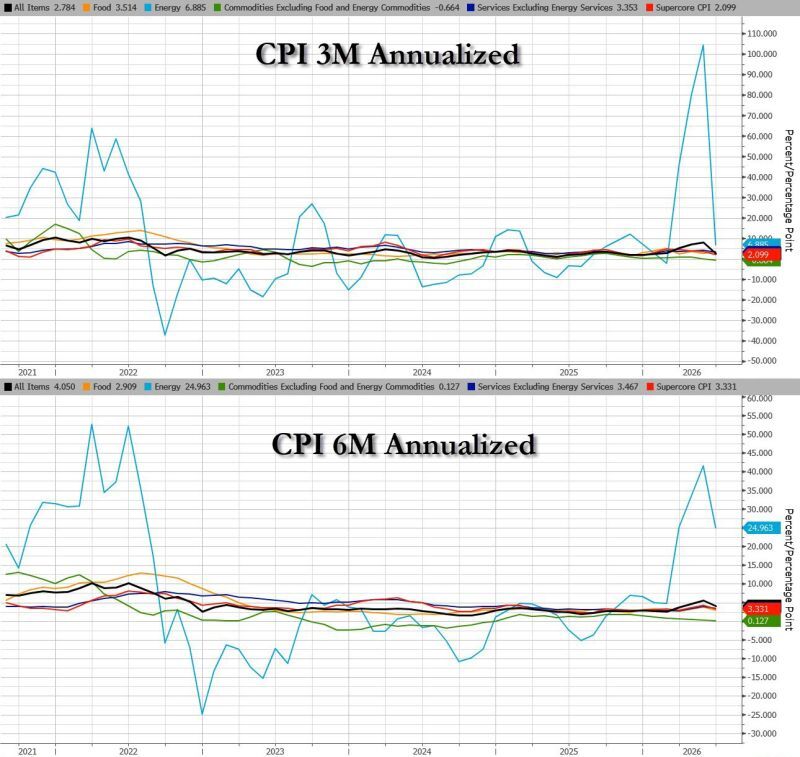

3M annualized US Headline CPI drops from 8.2% to 2.8%.

Source: zerohedge

15 Jul 2026

US small-cap stocks are bucking years of underperformance to enjoy their best year since 2003, helped by AI spending, tax changes and low valuations.

Source: FT

15 Jul 2026

Lucid $LCID is up 103% in the last 1.5 hours after the company denied bankruptcy rumors.

Source: Bull Theory

15 Jul 2026

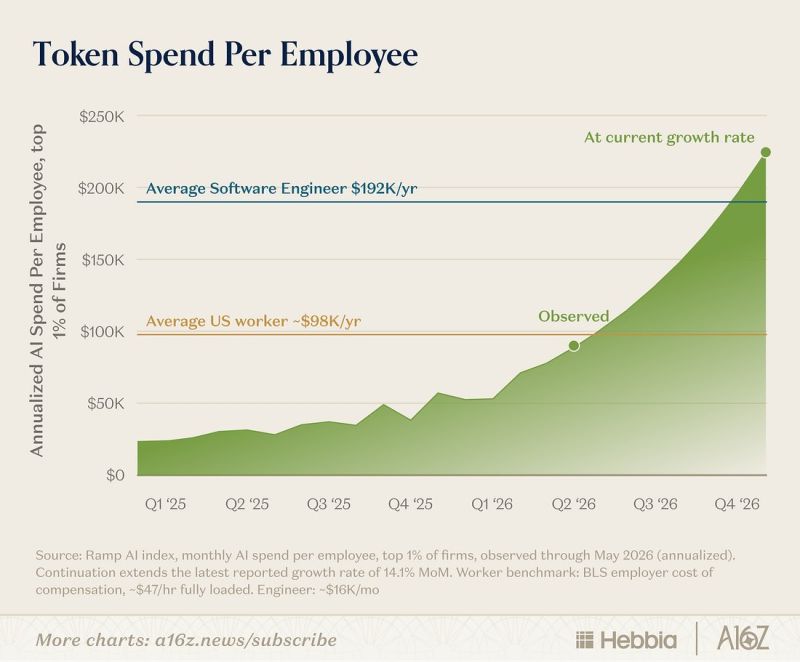

At the top 1% of AI-spending firms, AI spend per employee is on track to exceed average software-engineer pay by the end of the year.

Source: Hedgeye