This is how leverage turns a pullback into a wipeout.

The 2x leveraged SK Hynix ETF listed in Hong Kong has plunged 64% from its June peak after SK Hynix shares fell more than 35%, including a record 15% one-day drop on Monday. Many South Korean retail investors rushed into these leveraged ETFs after their launch, expecting to amplify AI-driven gains. Instead, extreme volatility and daily rebalancing accelerated losses, with reports of forced liquidations already emerging. The lesson is simple: leverage doesn't just amplify returns—it magnifies mistakes. In volatile markets, it can destroy capital far faster than most investors expect. Source: Global Markets Investor

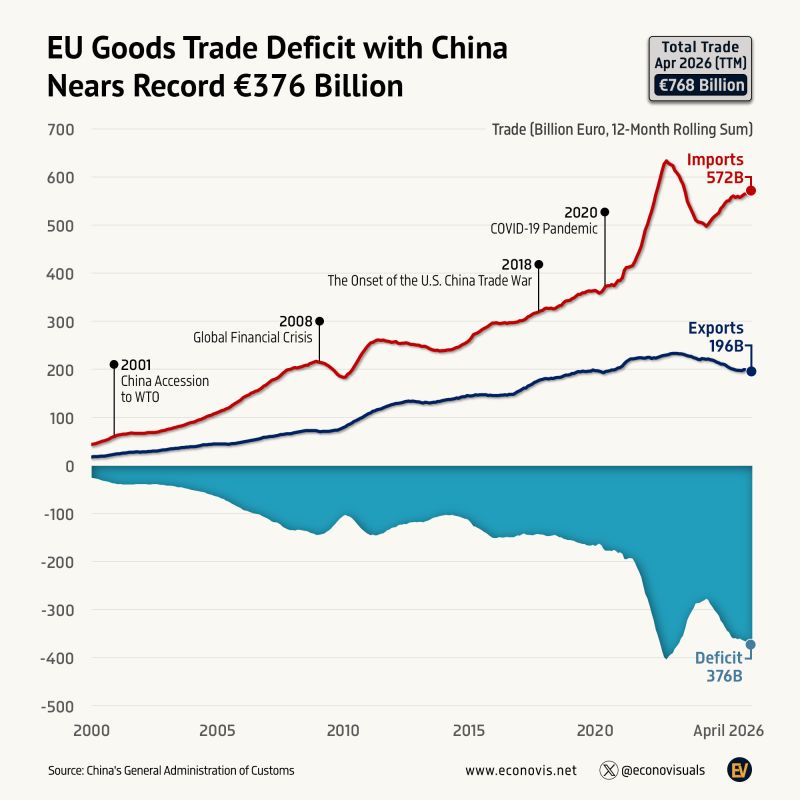

EU Goods Trade Deficit with China Nears Record €376 Billion

The European Union's goods trade with China totaled €768 billion in the twelve months ending April 2026, with €572 billion in imports and €196 billion in exports. The resulting €376 billion trade deficit was the second largest on record, underscoring Europe's continued dependence on Chinese manufactured goods despite efforts to diversify supply chains and reduce strategic vulnerabilities. Source: Econovis

Healthcare Stocks just formed a Golden Cross for the first time since October 2025

The last one sent prices higher by 10% over the next 10 weeks Source: Barchart

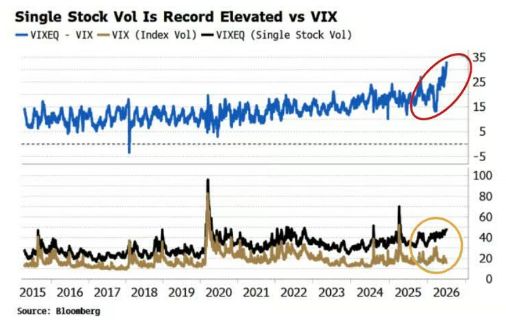

Single Stock Volatility relative to the CBOE Volatility Index $VIX has reached its largest gap in history

Source: Bloomberg, Barchart

Strait of Hormuz 🇮🇷 oil crossings (in white) have not recovered, yet oil prices (in blue) are near the levels they were pre-war.

Source: Gordon Johnson

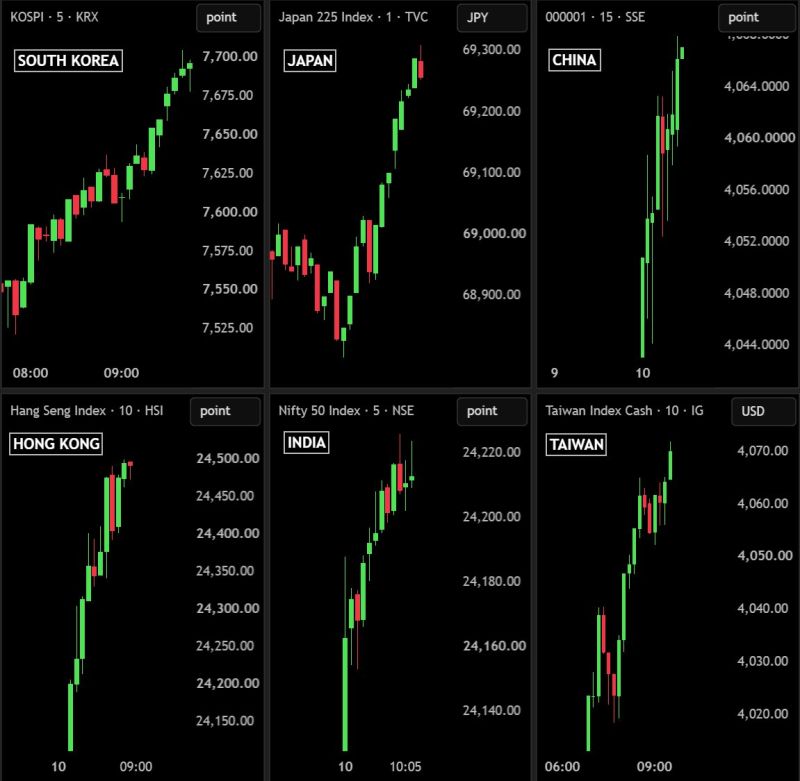

Massive Reversal in Asian Markets

Over $500 BILLION has been added to Asian stocks today as semiconductor and AI stocks rebounded after the recent sell-off, following a strong close on U.S. stocks. South Korea's KOSPI is up +4.6%, adding ₩280.6 trillion ($189B). Japan's NIKKEI is up +1.6%, adding ¥22.9 trillion ($139B). Taiwan is up +1.2%, adding NT4.1 trillion ($50B). China's SSE is up +0.8%, adding ¥520 billion ($73B). Hong Kong's HSI is up +1.5%, adding HK$131.6 billion ($17B). India's NIFTY is up +1.0%, adding ₹4.9 trillion ($57B). Source: Bull Theory

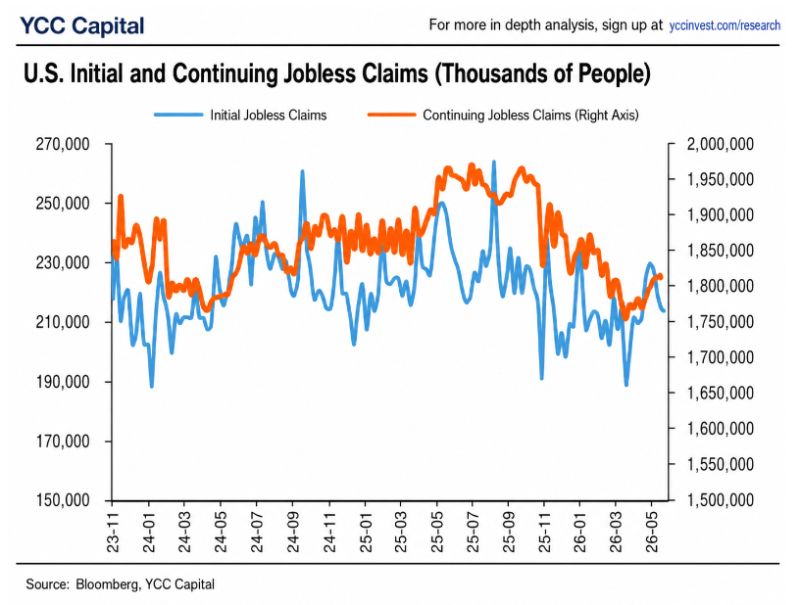

🚨 The labor market still refuses to crack.*

Initial jobless claims remain stuck in a remarkably stable range of 200,000–230,000, while continuing claims are hovering around 1.8 million. For more than two years, recession fears have dominated headlines. Yet the one indicator that typically flashes red before a downturn still isn't doing it. Yes, workers who lose their jobs are taking longer to find new ones, pushing continuing claims higher. But companies are not laying off employees at the pace you would expect ahead of a recession. That's the key distinction. 📌 The labor market is cooling, not collapsing. For the Federal Reserve, that's an important signal. As long as layoffs remain contained, policymakers can stay focused on inflation instead of rushing to support the economy. Jobless claims remain one of the strongest pieces of evidence that the U.S. economy is slowing—but not yet heading into an imminent recession. Source: YCC Macro

To put things into perspective: The Nasdaq 100 is currently trading at ~23x NTM P/E

which is broadly inline with its 10y average multiple and towards the lower end of its 3-4y range, Goldman says, Source: HolgerZ, Bloomberg