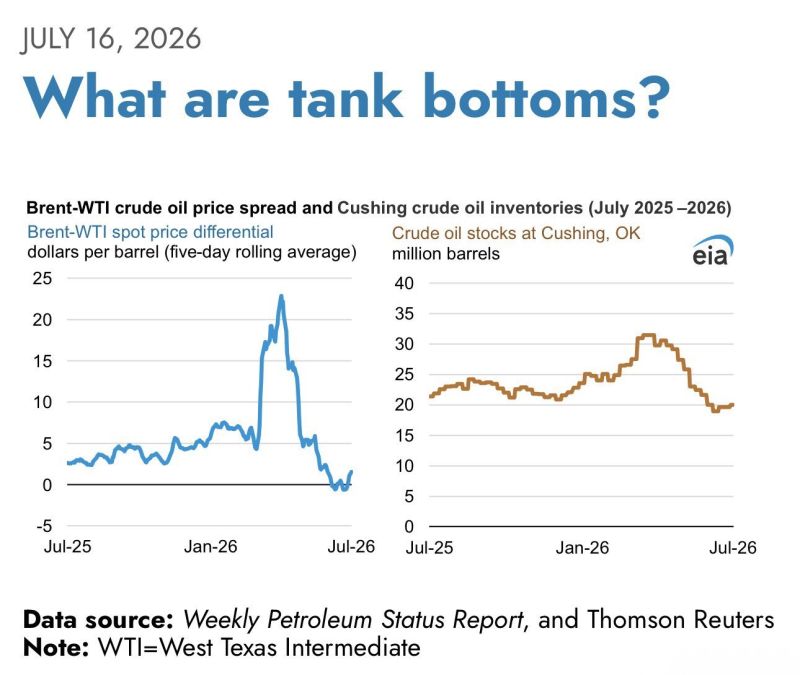

The EIA just published a warning today that reported Cushing inventory may overstate how many barrels are actually usable as stocks approach tank bottom levels.

This is the exact mechanism from the storage schematic covered in the below post. The suction line near the bottom of a tank means the last portion of reported inventory was never really accessible. If Cushing tightens further, the headline barrel count will look higher than what the market can actually draw on. Watch operationally accessible barrels. Source: Jack Prandelli on X

Lyn Alden's 'ORANGE JUICE' Raises $40 million to launch a permanent capital holding company backed by a BTC treasury

"It’s a company that acquires, improves, and permanently holds cash-flowing businesses, backed by a bitcoin treasury" - Lyn Alden Source: Bitcoin Magazine

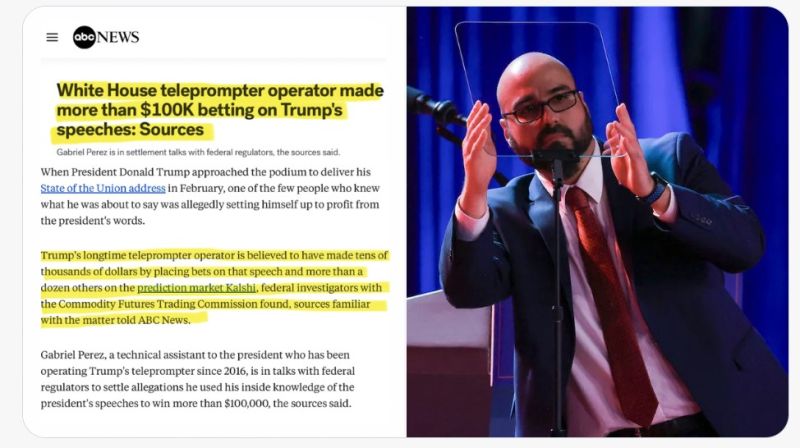

Trump's own teleprompter operator got caught betting on his speeches before he gave them, per ABC news.

Gabriel Perez, who has run Trump's teleprompter since 2016, made over $100,000 betting on Kalshi's "Mentions" market, where users bet on specific words or phrases said during a speech. CFTC investigators found he placed bets on more than a dozen speeches over three months, including the State of the Union, a Davos address, and a Medal of Honor ceremony. Kalshi flagged the activity itself and referred it to regulators. Perez is now in settlement talks with the CFTC, and he still holds his job today. Source: Bull Theory

JAPANESE STOCKS JUST ENTERED A TECHNICAL CORRECTION:

The Nikkei 225 dropped -4% on Friday, now more than -10% below its June 25 peak, marking a technical correction and its worst weekly loss since April 2025. The broader Topix fell -2.7%, with Tokyo Electron alone contributing the most to the decline after sliding -8.2%. Market breadth was weak, with 810 stocks falling versus 788 rising and 39 unchanged. This comes as investors grow increasingly concerned that AI-related capex is outpacing returns, after Taiwan Semiconductor, $TSM, fell despite raising both its spending and revenue targets, mirroring Samsung's selloff earlier this month despite beating earnings estimates. Kioxia Holdings led the losses, plunging -16%, its biggest one-day drop since November 2025. Its market capitalization has now been cut in half in just one month after briefly becoming Japan's most valuable company. AI euphoria across semiconductor sector is unwinding rapidly. Source: Global Markets Investor

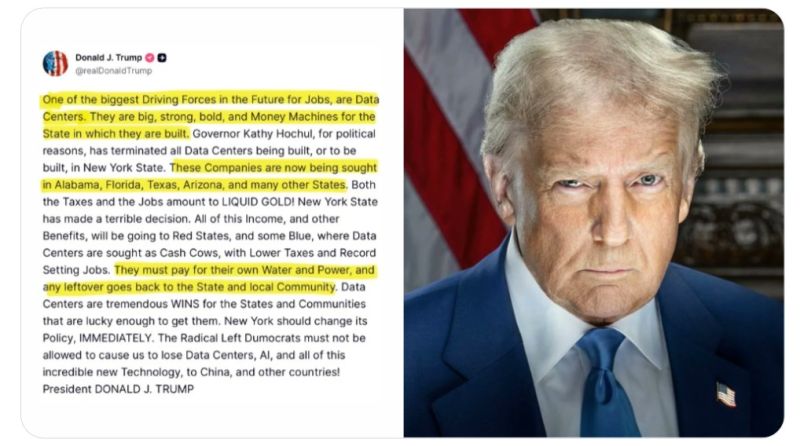

President Trump says New York is making a "terrible decision" by blocking data centers.

Trump says AI data centers are "money machines" that create jobs and generate massive tax revenue. He claims companies are now moving to states like Texas, Florida, Arizona, and Alabama instead. Trump also warned the US cannot afford to lose AI infrastructure and data centers to China and other countries. Source: Bull Theory Afficher la traduction

Goldman: "We are seeing a clear theme of buying Hyperscalers vs selling Semis as our Mag7 basket is outperforming NDX by nearly 3%.

Momentum (memory) drawdown continues with our pair basket (GSPRHIMO) down another -6.5% today despite the modest reprieve yday, taking MTD performance to -24% (worst month since April 2009)"

Semiconductor Stocks

Semis have entered a technical correction and are on the verge of a bear market after falling 16% from June's all-time high Source: Barchart

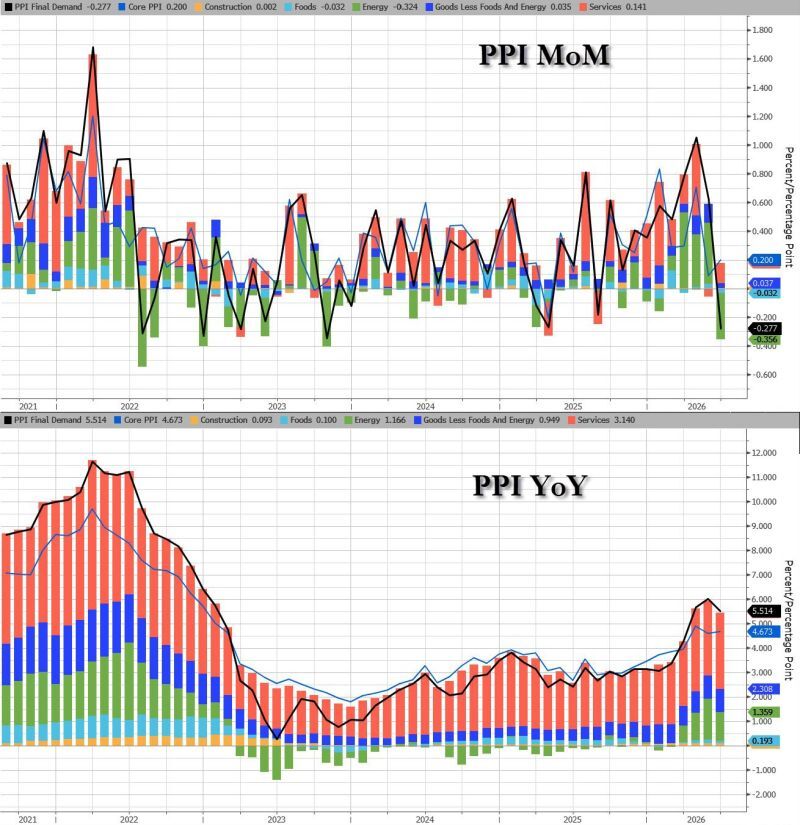

In case you missed it... Just like Tuesday’s CPI, US PPI inflation came in significantly softer than consensus forecasts, across the board.

Headline PPI moderated to 5.5% year-over-year (vs. 6.2% expected), driven by a -0.3% monthly decline (vs. 0.0% expected) The core rate fell to 4.7% yoy (on a 0.2% monthly increase). These much better-than-expected figures are set to further temper market expectations for upcoming interest rate hikes. Source: zerohedge