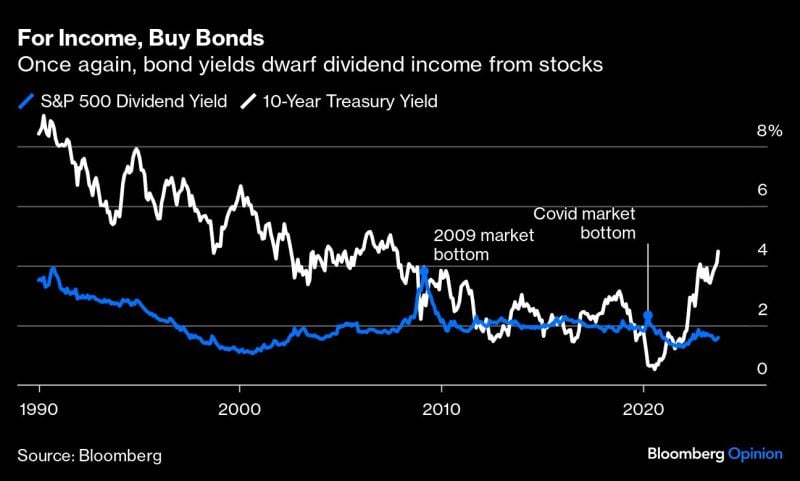

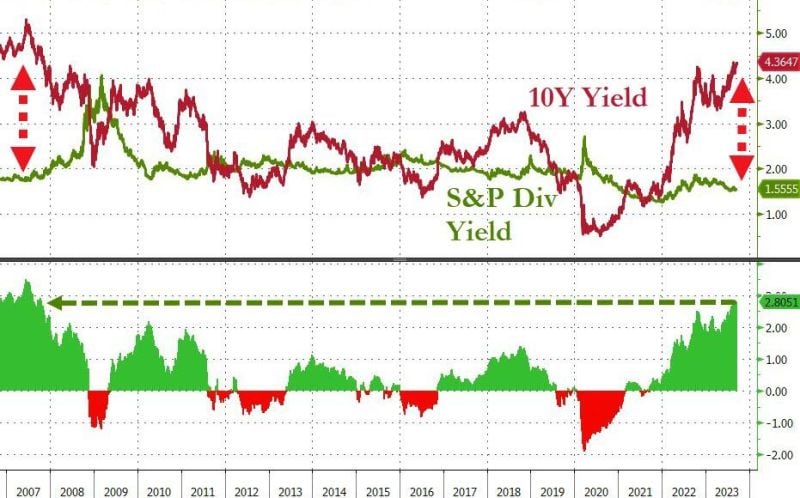

Treasury Yields now surpass Stock Dividend Yields by the widest margin since the Global Financial Crisis

Source: Bloomberg, Bar chart

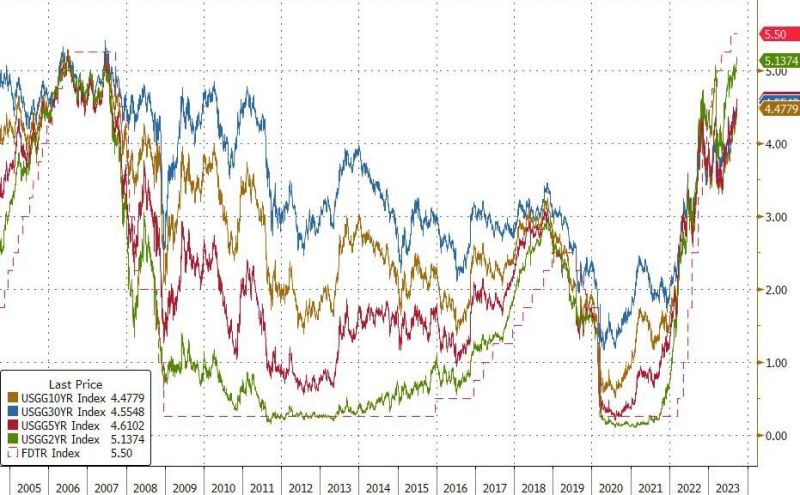

Yields pushing higher

US 2Y yields hit their highest since July 2006 US 5Y yields highest since Aug 2007 US 10Y highest since Nov 2007 US 30Y highest since April 2011 Source: Bloomberg, www.zerohedge.com

Inflation fear is NOT the driver of rising yields

Indeed, 10y real yields (10y nominal yields - 10y inflation expectations) jumped to 2.11%, the highest since 2009. In other words, investors are demanding higher REAL yields in the face of political chaos in Washington and high debt. Source: Bloomberg, HolgerZ

The longest duration bond ETF is now down 60% from its peak in March 2020

How is that possible? The 30-Year Treasury yield has moved from an all-time low of 0.8% in March 2020 up to 4.6% today. Long duration + Rising interest rates from extremely low levels = Pain $ZROZ Source: Charlie Bilello

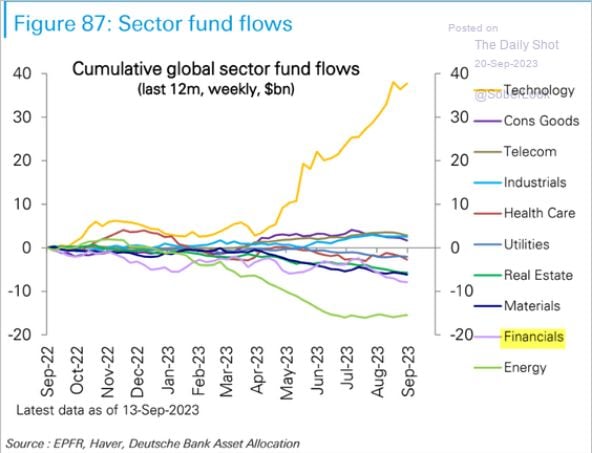

Sector fund flows

Long-only institutional & retail investors are all-in overweight tech and meaningfully underweight energy. Will elevated tech valuations, rising long-end yields, and rising oil prices trigger a squeeze in positioning? Source: The Daily Shot, EPFR, DB

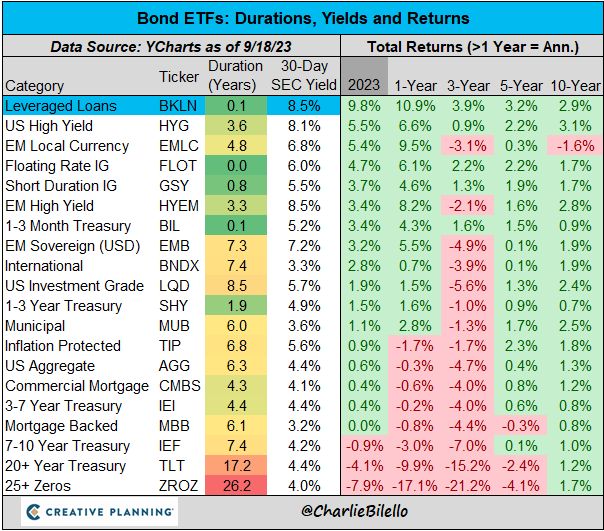

The best performing segment of the bond market this year? Leveraged Loans, up close to 10%. $BKLN

Source: Charlie Bilello

An ugly canadian CPI, surging crude oil prices and cautious positioning ahead of tomorrow's FOMC decision have pushed #us treasuries yields to their highest since 2007...

Bonds are now at their cheapest to stocks since Oct 2007... Source: Bloomberg, www.zerohedge.com

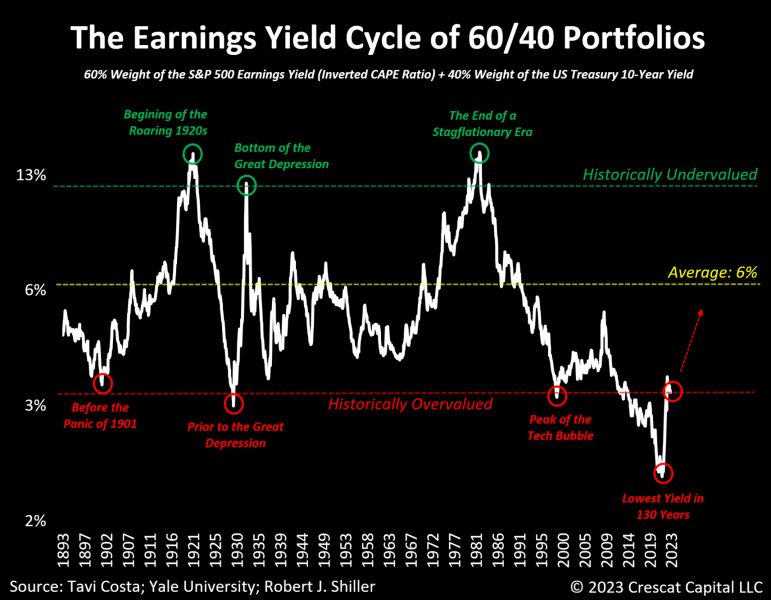

Is the 60/40 portfolio overvalued?

In August 2021, the combined valuation of overall equities and US Treasuries had reached its most expensive level in 130 years. To put the current valuation imbalance into perspective, its recent peak was a staggering 61% higher than its previous peak in the early 2000s. Although prices have corrected somewhat, particularly in the Treasury market, multiples are still elevated today. Source: Tavi Costa, Bloomberg