🚨 JUST IN: CANADA SLASHES RATES BY 50 BPS

Fifth cut in a row... Dropping the policy rate from 5% to 3.25% in 2024—150 bps total. But it’s not working fast enough: -Unemployment: 6.8% (highest in 8 years). -GDP per capita: Down 6 straight quarters. -Canadian Dollar $CAD at 4.5-year low -Former BOC Governor says “We’re already in a recession.” Market is pricing in another ~50bps of cuts by July 2025 ➡️ 2.75% overnight rate. Source: Genevieve Roch-Decter, CFA, Bloomberg

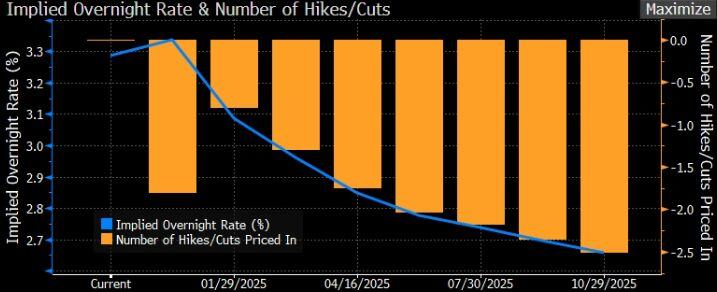

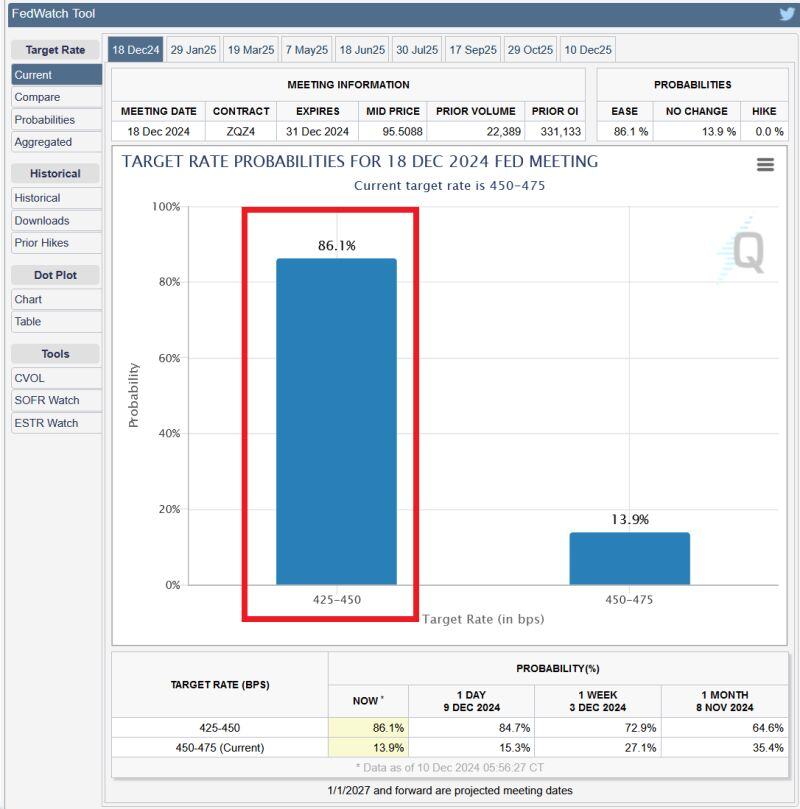

THERE ARE 7 DAYS TO THE LAST FED'S MEETING THIS YEAR

Market is pricing an 86% probability of a 0.25% rate cut, up from 73% last week. This comes after the November job report showed a lot of weakness under the surface. The Fed cut rates by 0.50% and 0.25% in Sep and Nov. Source: Global Markets Investor

‼️ BREAKING: This doesn't sound like a great mark of confidence...

The Bank of England will hide the identities of any pension funds, insurers or hedge funds bailed out under a new financial stability tool to prevent crisis contagion... Source: Radar @RadarHits - Bloomberg

🚨BIG WEEK FOR CENTRAL BANK DECISIONS AHEAD🚨

The European Central Bank, the Bank of Canada, the Swiss National Bank and the Reserve Bank of Australia will announce rate decisions. ECB and SNB are expected to cut by 0.25%, and BoC by 0.50%, while RBA to leave rates unchanged. Source; Global Markets Investor @GlobalMktObserv, Bloomberg

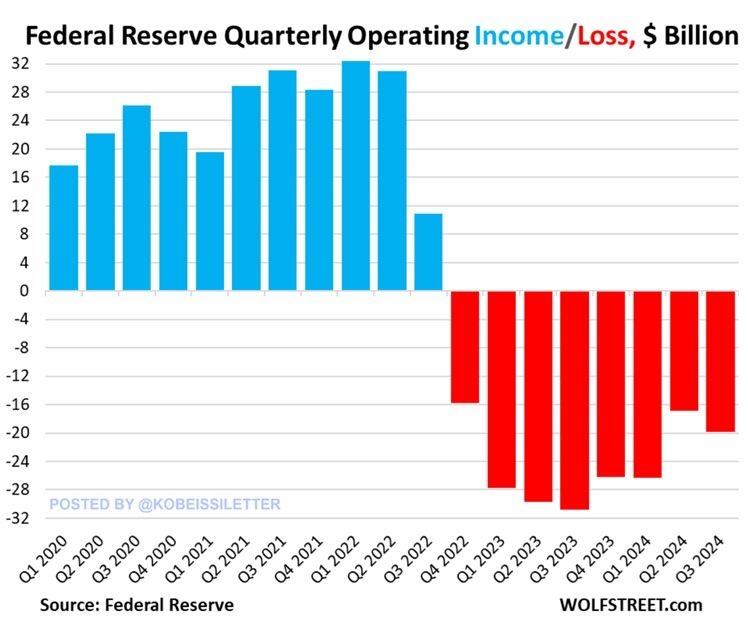

BREAKING: The Federal Reserve just reported a $19.9 BILLION operating loss in Q3 2024 up from $16.9 billion in Q2.

This marks the 8th consecutive quarter of operating losses for the central bank. As a result, cumulative operating losses reached a massive $210 billion over the last 2 years. This comes as the Fed has been paying hundreds of billions in interest to banks and money market funds. At the same time, income the Fed has earned on Treasuries and Mortgage-Backed-Securities has declined. Source: The Kobeissi Letter

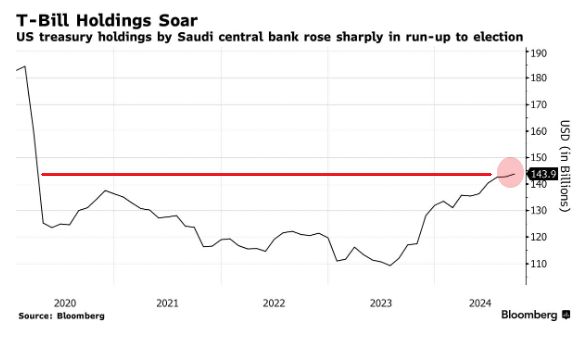

🚨 Saudi Arabia's U.S. Treasury Holdings are now the largest in more than 4.5 years

Source: Barchart, Bloomberg

US Fed officials see interest rate cuts ahead, but only ‘gradually,’ meeting minutes show - CNBC

Federal Reserve officials expressed confidence that inflation is easing and the labor market is strong, allowing for further interest rate cuts albeit at a gradual pace, according to minutes from the November meeting released Tuesday. The meeting summary contained multiple statements indicating that officials are comfortable with the pace of inflation, even though by most measures it remains above the Fed’s 2% goal. With that in mind, and with conviction that the jobs picture is still fairly solid, Federal Open Market Committee members indicated that further rate cuts likely will happen, though they did not specify when and to what degree.

It has been a very quiet year... Can we expect the same in 2025??? (Clone)

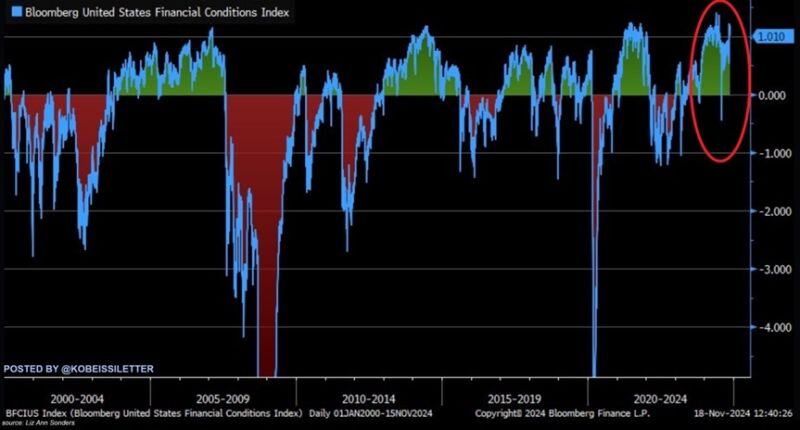

Financial conditions are now even easier than previous records seen in late 2020 and 2021. In fact, this makes financial conditions easier than when the Fed cut rates to near 0% overnight in 2020. Meanwhile, the market is pricing in a 59% chance of another 25 bps Fed rate cut in December. Source: The Kobeissi Letter, Bloomberg