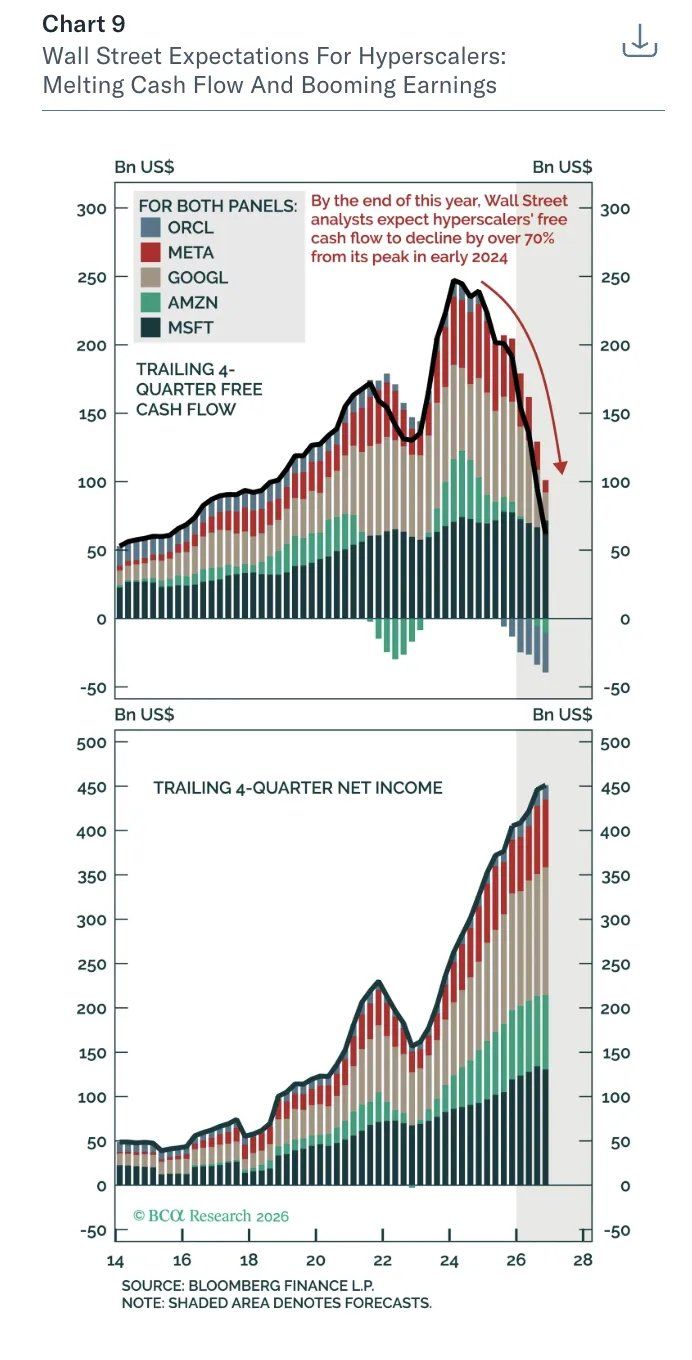

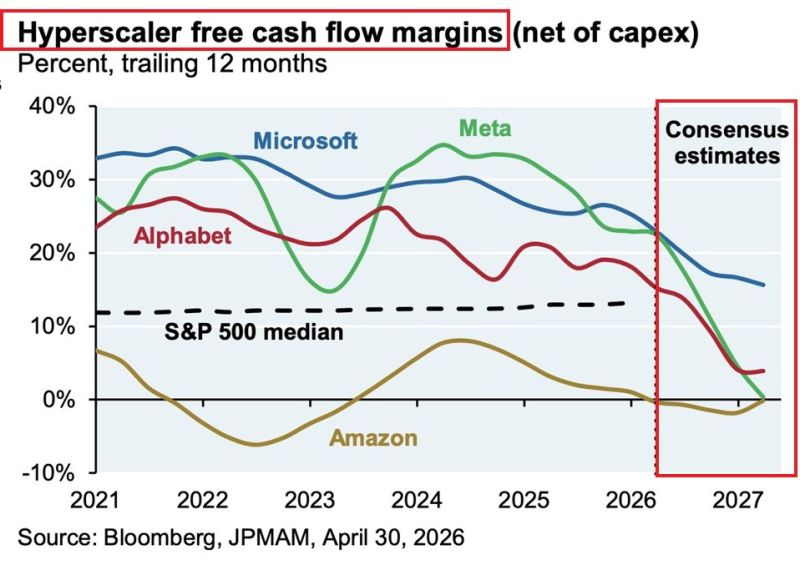

Wall Street projects hyperscalers’ free cash flow to fall by over 70% from its peak by the end of 2026, even as earnings keep climbing

Source: Christophe Barraud, Bloomberg

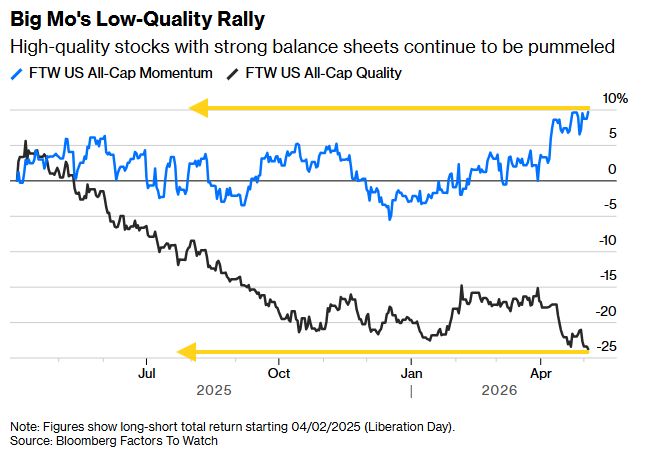

BBG's Authers: "It might be unfair to call this a dash for trash. "

But nobody seems to care about quality. This is from Bloomberg’s Factors To Watch service, showing the results of buying the top 20% of stocks by a factor while shorting the worst 20%. "Since Liberation Day, buying quality stocks has been a one-way ticket to losses." Meanwhile, Momentum has been performing strongly. Source: Bloomberg, Neil Sethi

🔴America's valuation premium over Europe is historically WIDE:

The S&P 500 trades at a forward price-to-earnings (P/E) ratio of ~21 times, while the Stoxx Europe 600 trades at ~14 times. This brings the valuation gap up to ~7 points, the widest since at least the 2008 Financial Crisis. This comes as the Middle East war exposed Europe's structural vulnerability to energy shocks, turning what looked like attractive valuations into a value trap. At the same time, the US benefited from its relative energy independence and surging tech sector. Source: FT, Factset, Global Markets Investor

President Trump is flexing on his gains on $INTC...

Source: Donald Trump on Truth Social

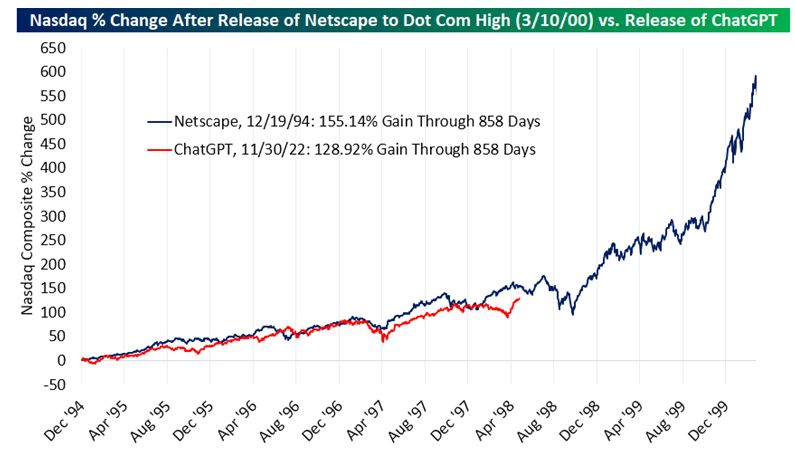

At 858 days since ChatGPT's release, the Nasdaq is currently up 129%.

858 days after Netscape's release, the Nasdaq was up 155%. "History doesn’t repeat itself, but it still rhymes. If this chart has any merit we might only be in the middle innings of this buildout." - Bespoke Source: Negligible Capital

⚠️ The AI gold rush has a hidden cost… and Big Tech is footing the bill.

Here’s the reality no one wants to say out loud: • Big Tech free cash flow peaked at ~$300B in 2024 • By 2026… it’s heading toward ZERO Why? Because AI isn’t just innovation… it’s a capital black hole. → ~$715B in capex (2026) → +70% YoY increase → Nearly ALL cash flow consumed Margins are collapsing fast: • Microsoft → ~16% • Meta → ~3% • Alphabet → ~0% • Amazon → ~-2% So what’s happening behind the scenes? They’re borrowing. Aggressively. • ~$175B in new debt expected in 2026 • Buybacks slowing across the board • Key equity support disappearing Translation: The AI boom isn’t being funded by profits… It’s being funded by leverage. And that changes everything. Less cash flow + more debt + fewer buybacks = ⚠️ Fragile market structure The uncomfortable truth: AI may define the future… But it’s draining the present. And the bill is just getting started. Source: Global Markets Investor, JPM, Bloomberg

THE G.O.A.T...

Source: Stocks World

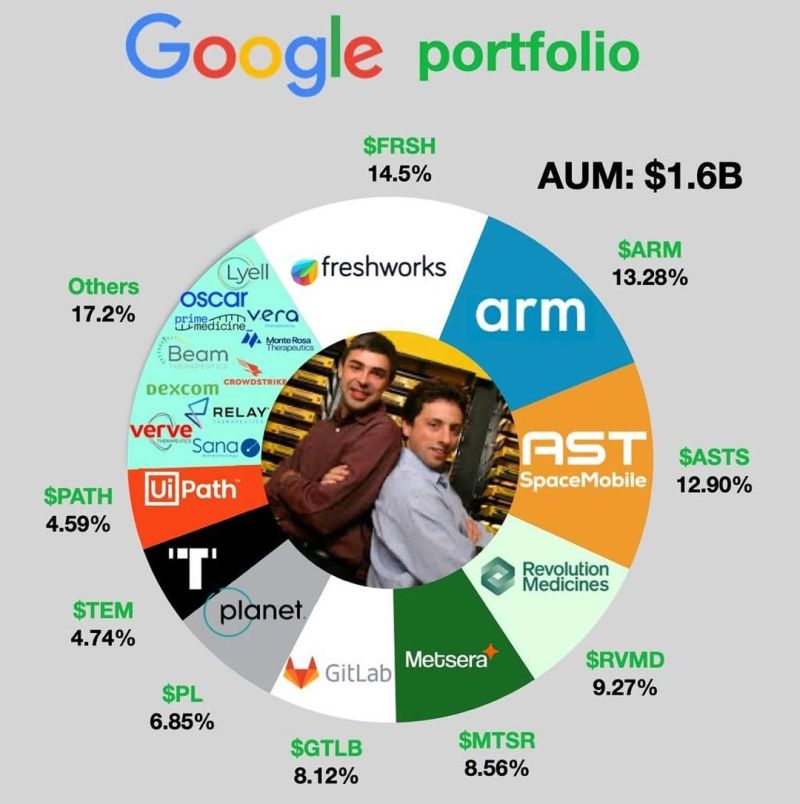

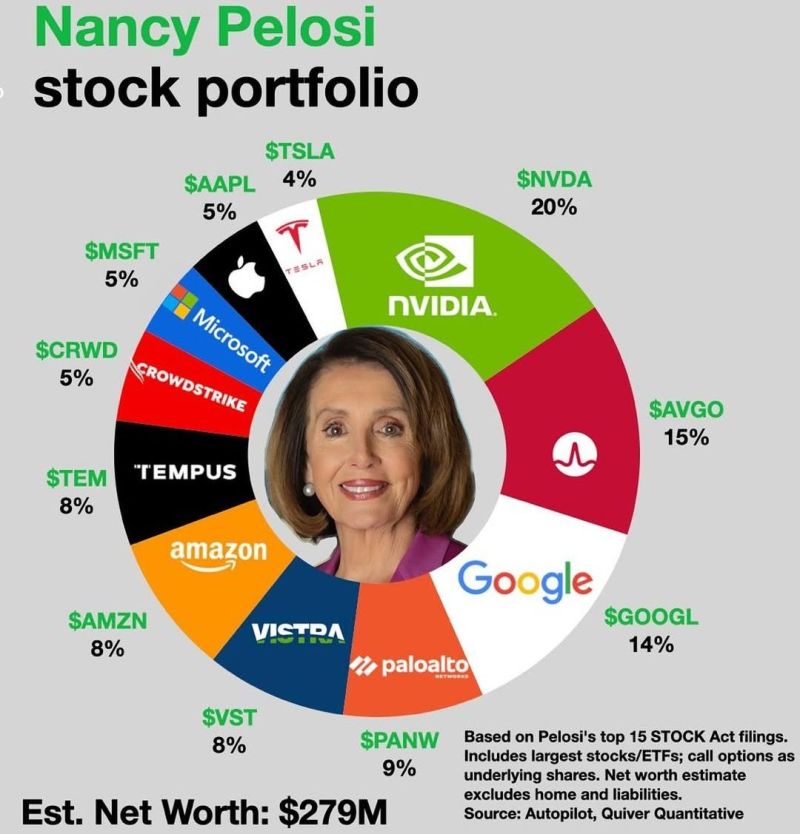

Google portfolio

Source: Stocks World