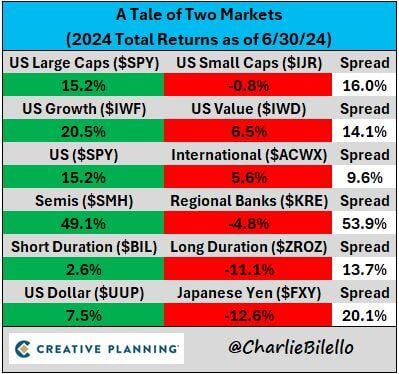

The first half of the year was a Tale of 2 Markets...

-Best of times: US large cap growth stocks, short duration bonds, US Dollar -Worst of times: Small caps, value, international, long duration bonds, Japanese Yen Source: Charlie Bilello

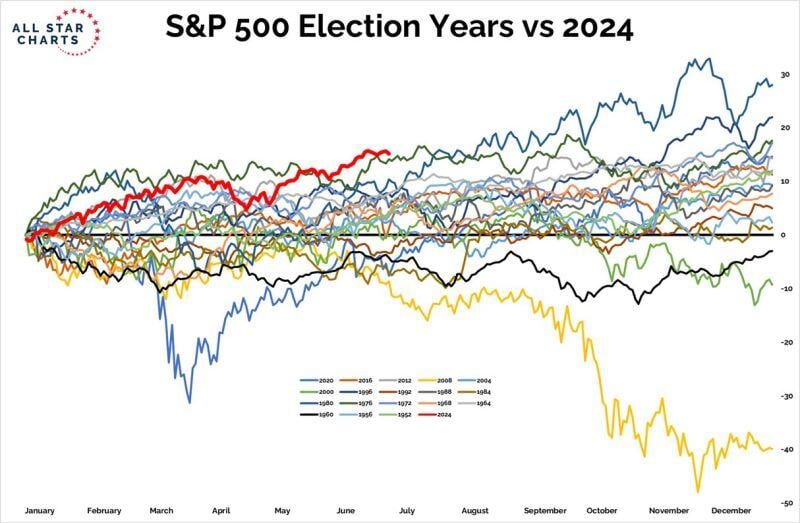

2024 has been the best H1 start out of all election years going back to 1952

Source: Grant Hawkridge

Hedgeye is unbeaten

.

APPLE IS EXPECTING BIG IPHONE 16 SALES, BASED ON CHIP ORDERS.

STOCK CLOSED UP NEARLY 3% Apple $AAPL has reportedly increased its chip order with TSMC $TSM, With the increased order in place, Apple is supposedly preparing to sell between 90M and 100M units of the iPhone 16 - Apple Insider

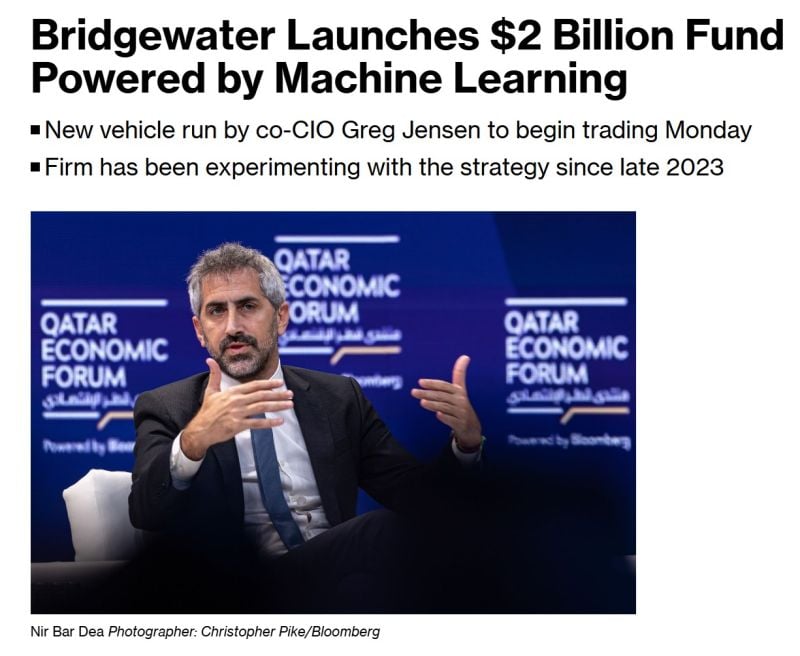

Bridgewater Associates is launching a fund that uses machine learning as the primary basis of its decision-making.

The vehicle will debut with almost $2 billion of capital from more than a half-dozen clients and begin trading Monday, according to people familiar with the matter, who asked not to be identified discussing the strategy. Source: Bloomberg

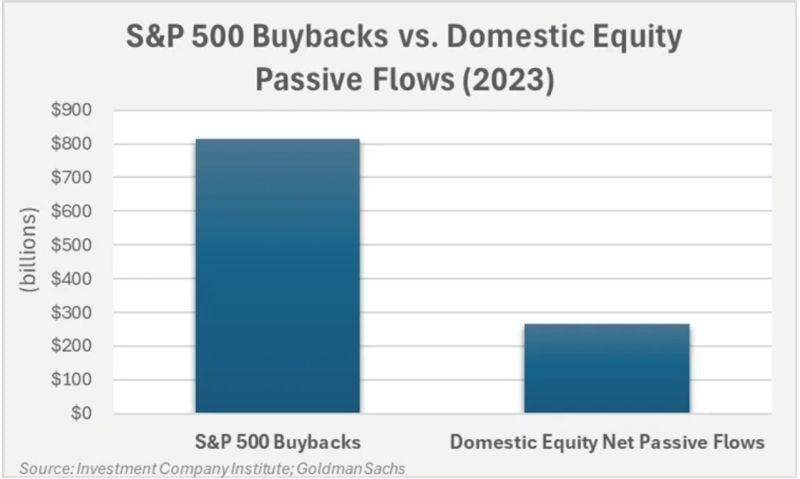

S&P 500 buybacks have been much more powerfuil than passive flows

Source: GS

The US Treasury market remains volatile

The 10-year note yield is now up over 20 basis points in since Friday's intraday low. That's 20 basis points in a matter of hours without any material news? Or is it a Trump effect? UST over-supply? Whatever the reason, for the first time in almost 5 weeks, the 10-year note yield is set to break above 4.50%... Source: The Kobeissi letter

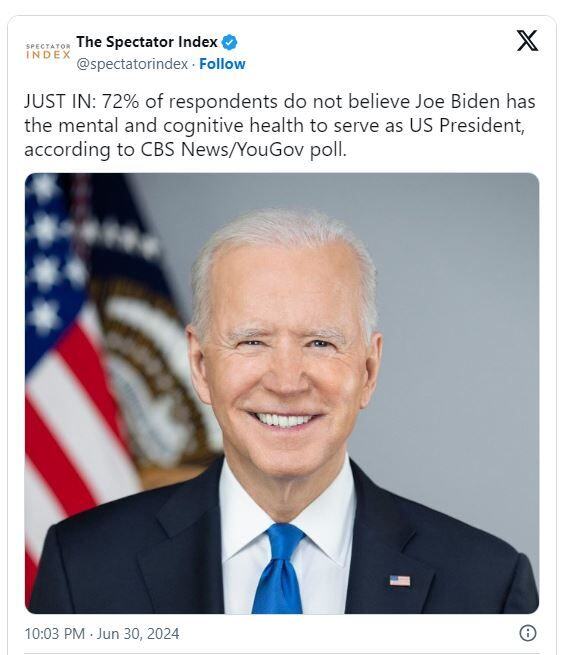

US Poll: Majority believe Biden's cognitive health doesn't qualify him for presidency

A new CBS News/You Gov poll reveals that 72% of Americans doubt Biden's "mental and cognitive health" meets the standards required for the presidency. Of those surveyed, 46% of Democratic voters believe Biden should consider withdrawing from the race due to health concerns. The poll also asked respondents about former President Donald Trump's fitness for office, with 50% expressing confidence in his mental and cognitive abilities, while 49% disagreed. Source: https://www.albawaba.com/