U.S. Bank losses on held-to-maturity assets have soared to an ALL-TIME HIGH of $400 Billion

Source: Barchart

US Q3 GDP numbers summarized in one cartoon

Source: Elizabeth Oliveira Fonseca

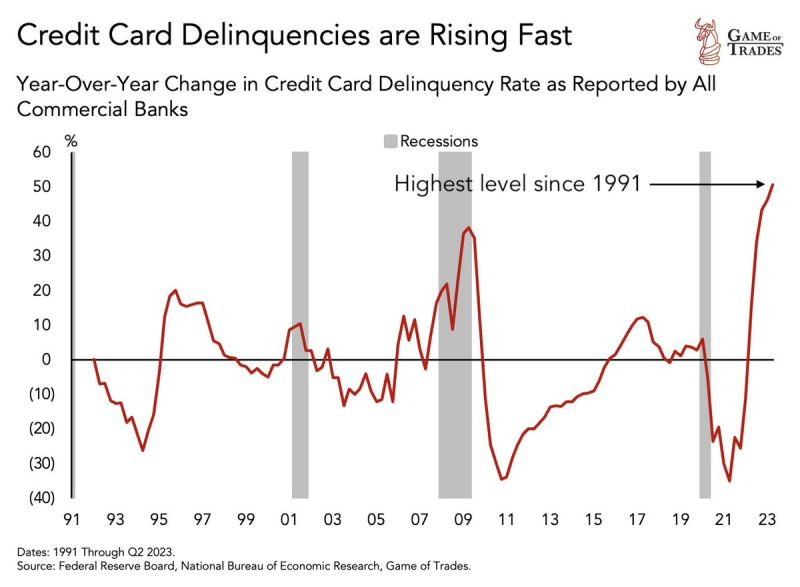

This is WORSE than the 2008 Financial Crisis. Credit card defaults are rising at levels NEVER seen in 3 decades

Source: Game of Trades

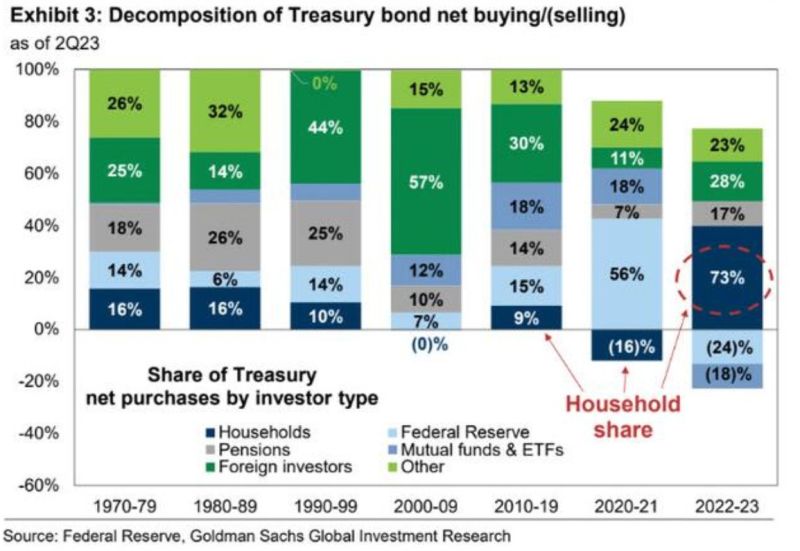

Adding to that Great Rotation theme is this chart

US households account for 73% of Treasury bond buying in 2022-2023 (so far) A lot of pain being experienced for those not willing to hold to maturity amid this bond blood bath... Source: Markets & Mayhem, Goldman Sachs

P/E Forward for the largest US companies - Magnificent 7

$TSLA Tesla 62 $AMZN Amazon 58 $NVDA NVIDIA 40 $MSFT Microsoft 30. $AAPL Apple 28 $GOOGL Alphabet 24 $META Meta 23 Source: Vlad Bastion

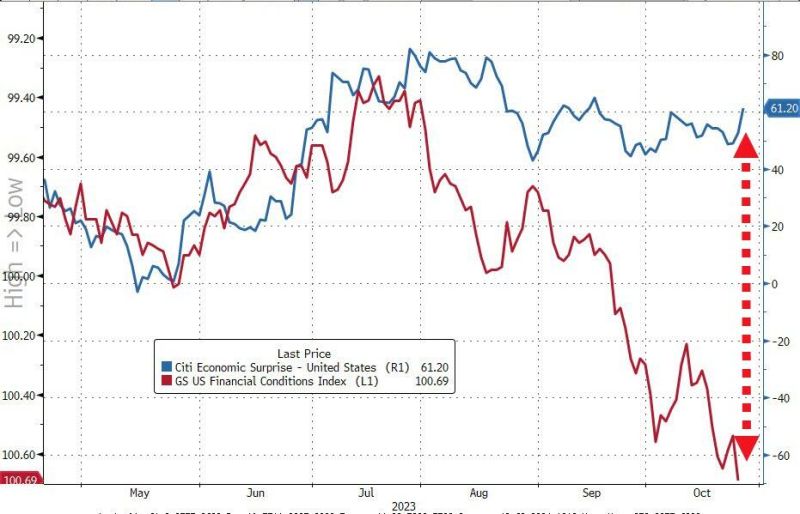

For now, the monetary policy transmission route of tightening US financial conditions are NOT reaching the economy...

Indeed, an avalanche of US macro data on Thursday presented a positive blend of updates across growth (better), inflation (lower), and labor markets (looser/worse). - Economic Growth: Real GDP rose 4.9% in 3Q (consensus 4.5%) driven by strong demand across consumer and federal/state government, and inventories. However, a major contribution from inventories could in turn weigh significantly on growth in 4Q - Manufacturing: Orders for Durable and core capital goods also grew by more than expected... thanks to a massive surge in non-defense aircraft orders (so don't expect it to last). - Housing: Pending home sales rose 1.1% month over month in September, above expectations for a decline... but brace for October to be a bloodbath as mortgage rates re-accelerated. - Inflation: Core PCE prices component of the GDP report rose less than expected. - Labor: Initial and continuing jobless claims both increased by more than expected -- a positive for markets which are focused on labor market re-balancing (i.e., could benefit from less wage inflation).

US GDP grew 4.9% in Q3 QoQ annualized, way faster than +4.3% expected

However, bond yields dropped in the afternoon session. This Bloomberg US GDP chart shows why. Indeed, US GDP growth in Q3 was mainly driven by private consumption & inventories. This may not last. Source: Bloomberg, HolgerZ

US stocks now account for 61% of the $60 Trillion MSCI All-Country World Index, the highest level in history

Source: FT, Barchart, Bloomberg