Odds of a rate cut at Fed December meeting have increased again (70%+) but Fed officials remain divided on three questions that come down to judgment calls:

1. Will tariff-driven cost increases truly be a one-off? 2. Does weak hiring reflect a demand slump or reduced supply? 3. Are rates still restrictive?

BREAKING: U.S. Banks

FED just did it again! Another $24 Billion injection into the U.S. Banking system Make that $125 Billion over the last 5 days Source: zerohedge

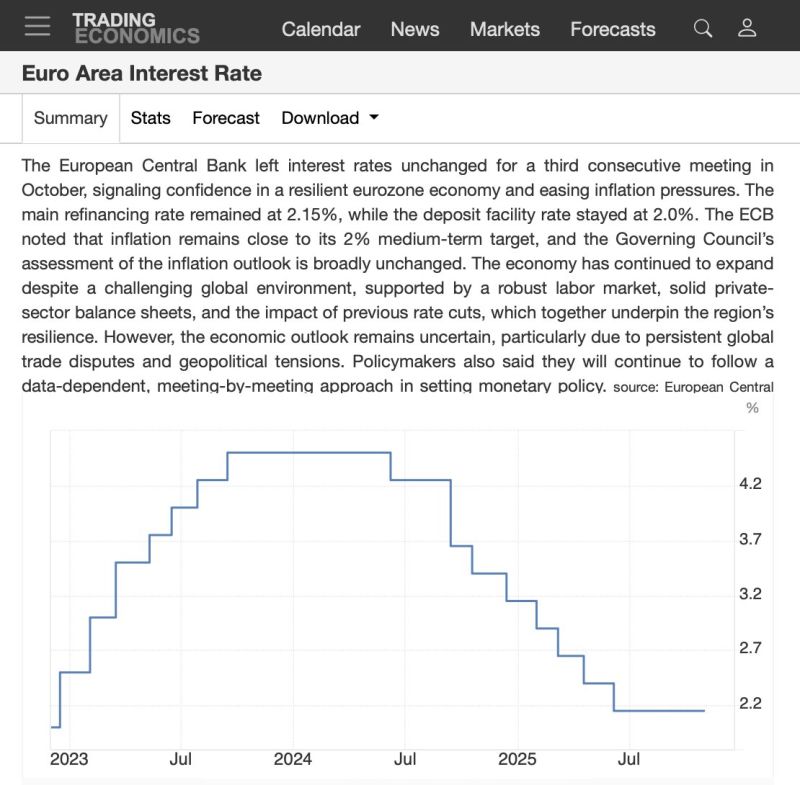

🚨 ECB hits pause again as economy shows resilience

The European Central Bank kept rates on hold at 2% for the third straight meeting. 💶 Inflation is right on target at 2% 📉 Rates down from last year’s 4% peak 💪 Growth still holding up The ECB says Europe’s economy is proving resilient — supported by strong labor markets and healthy private balance sheets. But beneath the calm? ⚠️ Uncertainty from global trade tensions and geopolitics still clouds the outlook.

For 35 minutes, today’s FOMC meeting was painfully boring

The Fed cut rates ✅ Ended QT ✅ A few dissenters ✅ Markets? Totally unfazed. S&P flat. Yields steady. Commodities and crypto asleep. And then — 2:35 PM. Powell drops one line that flips everything: “December cut is not for sure, far from it.” Boom 💥 Rate-cut odds crash from 95% → 65% in minutes. Stocks wobble. Yields jump. Traders scramble. Moral of the story? In markets, boredom never lasts long — and one sentence from the Fed can move trillions.

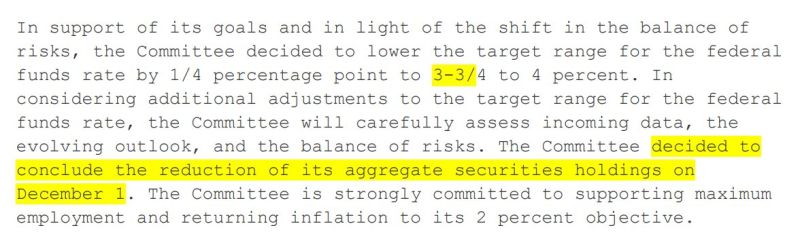

THE FED WILL END QT ON DECEMBER 1ST

Moving from restrictive → supportive balance sheet policy. This is not QE, but it is definitely a positive development that provides a mild liquidity tailwind for markets. Source: Joe Consorti @JoeConsorti

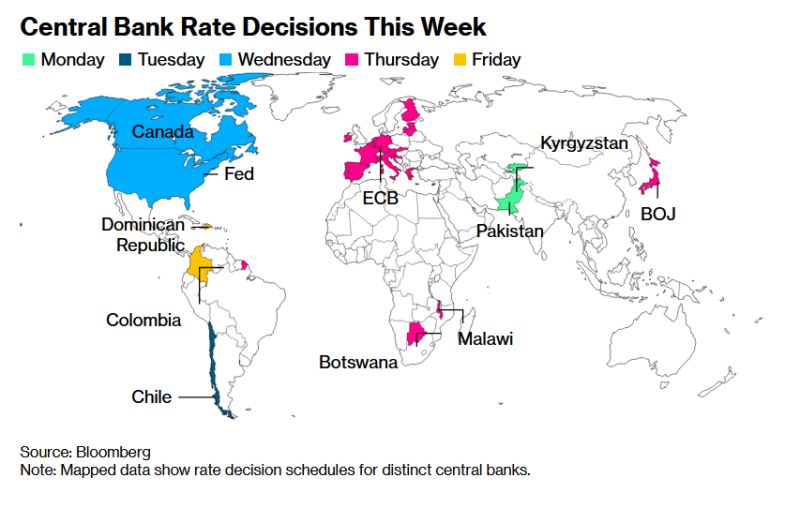

🚨 HUGE Week Ahead for Global Markets! 🚨

Four major central banks. One defining week. Here’s what’s coming 👇 💵 Federal Reserve — Expected to cut rates by 0.25% on Wednesday, and all eyes are on what comes next for its Quantitative Tightening (QT) program. 🇨🇦 Bank of Canada — Also forecasted to trim rates by 0.25%, signaling growing concern over slowing growth. 🇪🇺 European Central Bank — Likely to hold steady, keeping the focus on inflation trends across the Eurozone. 🇯🇵 Bank of Japan — Expected to stay the course, balancing yen weakness with cautious optimism. This week could set the tone for global liquidity, currencies, and market sentiment heading into year-end. 🌍.

Yesterday we saw another $3 billion FED pump into the banking system.

The use of the facility is now a daily occurrence; the regional banking sector obviously has a liquidity issue. That's a total of $21 billion in 4 weeks. Source: The Great Martin on X

Interesting comment on X by @Andreas Steno on X about a worrying development that took place yesterday.

As financials and regionals are getting hammered with signs of stress in USD money market, the SOFR - Fed funds spread keeps widening… Maybe the Fed will be involved earlier than they think on the QT ending stuff...