The U.S. Justice Department has launched a criminal mortgage fraud probe into Federal Reserve Governor Lisa Cook

It has issued grand jury subpoenas out of both Georgia and Michigan, according to documents seen by Reuters and a source familiar with the matter. The investigation followed a criminal referral from Federal Housing Finance Agency Director Bill Pulte, and is being conducted by Ed Martin, who was tapped by Attorney General Pam Bondi as a special assistant U.S. attorney to assist with mortgage fraud investigations involving public officials, along with the U.S. Attorneys' offices in the Northern District of Georgia and the Eastern District of Michigan, according to the person, who spoke anonymously since the matter is not public. Source: Reuters

🚨 Goldman Sachs has doubled down on its optimistic forecast for gold, maintaining a structural bullish view on the precious metal

The investment bank predicts gold will reach $3,700 per ounce by the end of 2025 in its base case scenario, with further growth to $4,000 by mid-2026. Goldman’s analysis indicates that a recession could accelerate ETF inflows and drive prices even higher to $3,880. More dramatically, extreme risk events such as challenges to Federal Reserve independence or shifts in U.S. reserve policy could potentially catapult gold prices to $4,500 by year-end 2025. Source: www.goldsilver.com https://lnkd.in/eCau26HP

With the Fed’s reverse repo facility nearly drained, the system now leans on reserves as the main buffer.

Right now, they sit at ~$3.2T, which the Fed still calls “ample.” Governor Waller has suggested ~$2.7T is a safe floor, while Barclays sees end-September reserves sliding closer to that line. The problem? Treasury bill issuance and QT are still pulling cash out each month. With no RRP cushion left, every dollar matters more and once reserves fall into the danger zone, stress tends to show up fast in repo markets, auctions, and short-term funding. Source: StockMarket.News @_Investinq on X

The US just sold $70 billion of 5-year Treasuries.

The Bid-to-Cover ratio was 2.36. Foreign buyers pulled back but US buyers stepped up in record size. Here's the breakdown: • Foreign accounts (called “Indirects”) bought 60.5%. • Domestic institutions (called “Directs”) bought a record 30.7%. • Dealers (big banks) bought only 8.8%, the lowest ever. Now here’s the twist: even though the auction was definitely a poor one, the bond market rallied afterwards. 10-year Treasury yields actually dropped. Why? Because traders were braced for worse. “Not awful” was good enough to spark a rally. Source: StockMarket.news

Trumps Fed power shift in play

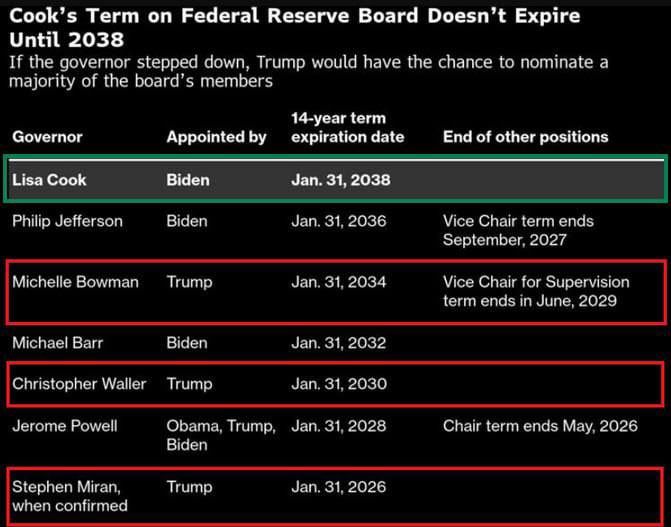

➡️ Trump’s push to remove Fed Governor Lisa Cook, could flip the balance of power inside the Fed. If Cook is out, Trump-appointed Governors would hold 4 of 7 seats (excluding Powell). That would give Trump the majority on the board for the first time in history. This shift could open the door to aggressive easing. Cook’s term runs until 2038, making this challenge unprecedented. The Fed has never faced a political reshuffle like this, and the outcome could define the next chapter for US rates and markets. Source: MartyParty @martypartymusic

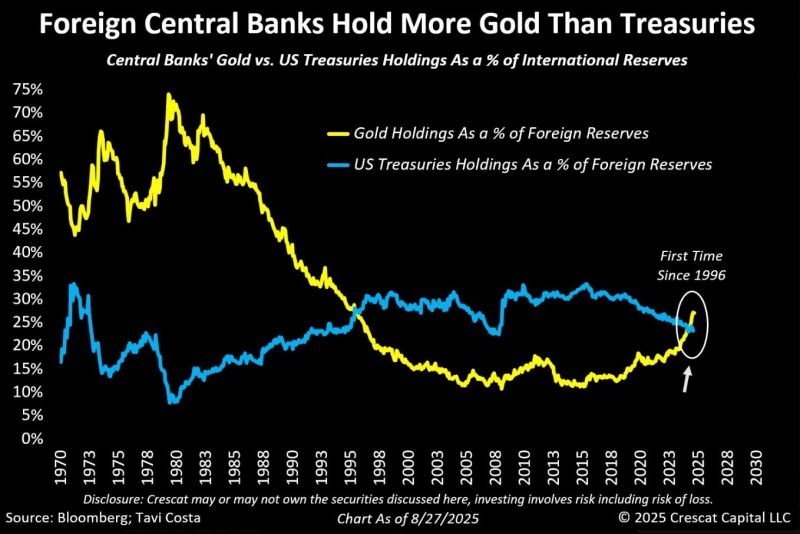

Foreign central banks now officially hold more gold than US Treasuries — for the first time since 1996.

We might be witnessing one of the most significant global rebalancing we've experienced in recent history, in my view. Source: Tavi Costa, Crescat Capital, Bloomberg

There are 3 sure things in life: 1) death; 2) taxes and; 3) printing money...

Source: Charlie Bilello

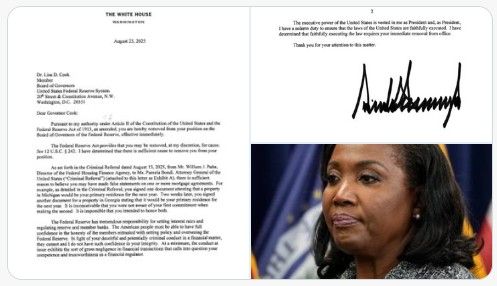

President Trump has officially FIRED Federal Reserve Governor Lisa Cook after Bill @Pulte exposed her for MORTGAGE FRAUD. Cook was appointed by Biden in 2022.

President Trump cited Article II of the Constitution and the Federal Reserve Act of 1913 to justify firing Cook over alleged mortgage fraud. He claimed, via a Truth Social post, that Cook’s dual declaration of primary residences and false statements on mortgage documents meet the broad, historically strict “cause” standard required for removal under the Federal Reserve Act. ➡️ The Federal Reserve Board is undergoing a transition and is increasingly influenced by Trump. If Cook’s removal stands and Powell steps down after his term as chair, Trump could appoint up to five of the seven governors, securing a lasting majority ➡️ “I will not resign,” said Cook, who hired high-profile attorney Abbe Lowell to challenge her purported termination; she says ‘he has no authority to do so. “President Trump purported to fire me ‘for cause’ when no cause exists under the law, and he has no authority to do so,” said Cook in a statement late Monday. “I will not resign.” Abbe Lowell, a lawyer for Cook, said Trump’s move “is flawed and his demands lack any proper process, basis or legal authority. We will take whatever actions are needed to prevent his attempted illegal action.” 👉 This development introduces significant uncertainty for markets regarding the Fed's independence, forward guidance, and interest rate policy. After the initial reaction, attention will likely shift to the nomination process. If Trump moves quickly to appoint candidates favouring looser monetary policy, the likelihood of earlier and steeper rate cuts could rise materially, though potential legal challenges and political pushback may moderate expectations