The market is pricing in a 50 basis point rate cut next month.

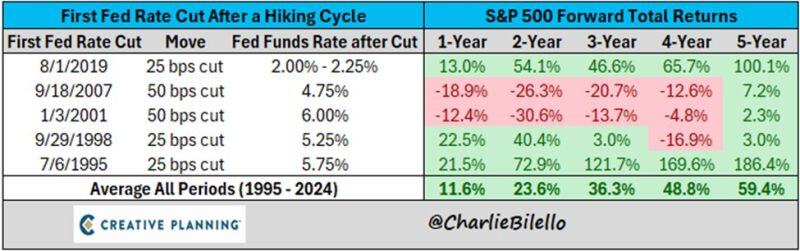

Market returns following rate cuts have been positive except for periods when the market is generally in crisis. Source: Charlie Bilello, Peter Mallouk

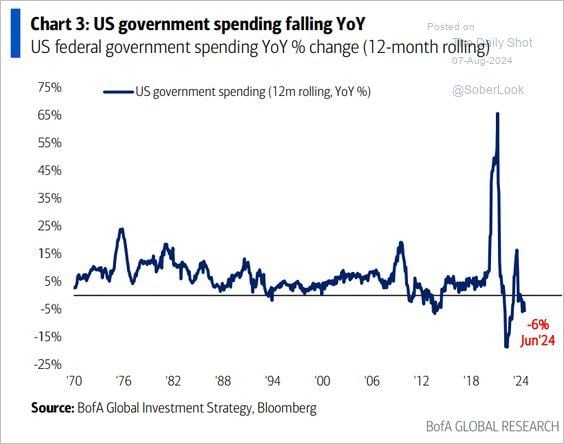

The main reason the economy has been able to avoid a recession over the last 2-years

was due to the massive spending from the inflation reduction and CHIPs Acts. However, the rate of that spending is declining which could potentially weigh on economic growth going forward. Source: BofA, The Daily Shot, Lance Roberts

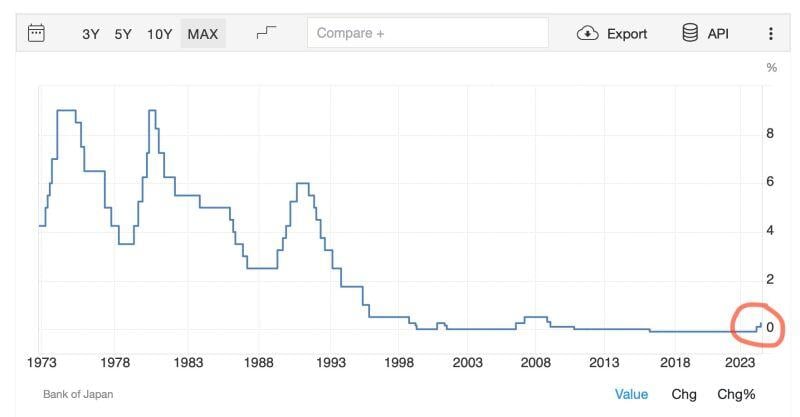

This is what triggered a global-scale sell-off of every major asset class...

A harsh remainder how shaky the global financial system is... Source: Bank of Japan, Sina 21st Capital on X

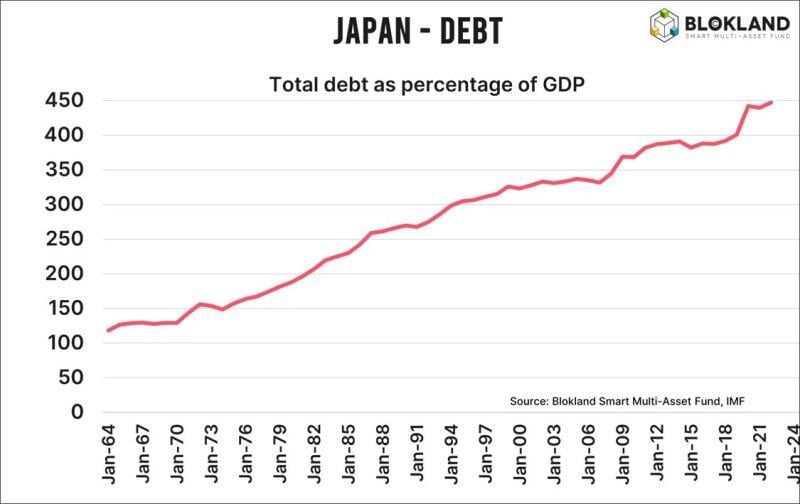

This is the ultimate reason why the Bank of Japan ‘needs to maintain monetary easing.’ DEBT

i.e the yen carrytrade is likely to resume sooner rather than later Source: Jeroen Blokland

It seems that many companies are in desperate need for rate cuts...

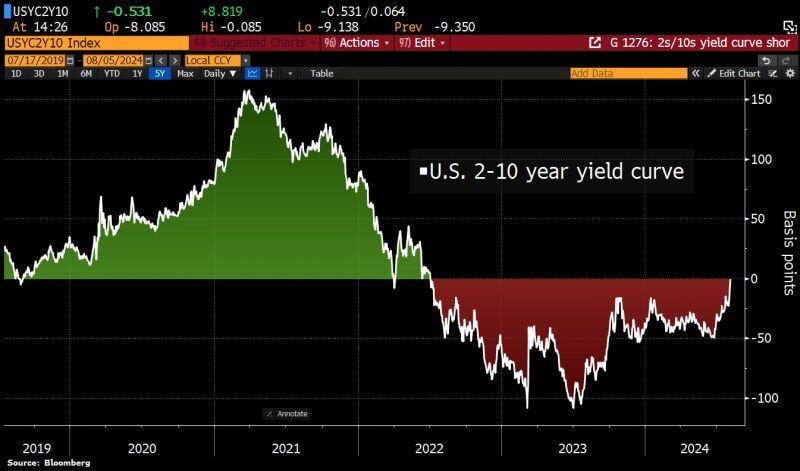

Source: Bloomberg

BREAKING: Is the BoJ capitulating?

The Bank of Japan Deputy Governor says they WON’T raise rates when the market is unstable. The Yen is getting absolutely destroyed…and the Nikkei is up nearly +3%, Nasdaq Futures is up +1.2% A wild start of August... Source: TradingView

US 2s/10s yield spread is now flat for the 1st time since 2022 on aggressive repricing of Fed rate cuts

US 2y yields have plunged by 70bps to 3.69% since last Wed while US 10y yields only dropped by 40bps in the same time. Source: Bloomberg, holgerZ

Fed's emergency rate cut never happened when the VIX was below 40.

It seems that we are getting there... Source chart: Yahoo finance