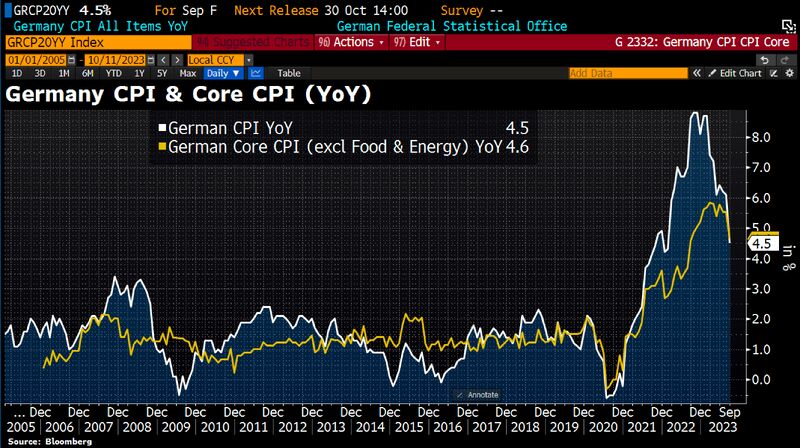

German inflation in September fell to its lowest rate since outbreak of war in Ukraine, confirming prior estimates

CPI slowed to 4.5% in September YoY from 6.1% in August. Headline CPI is now lower than Core CPI BUT food prices are already on the rise again. Compared to previous month, food has become 0.4% more expensive. Source: Bloomberg, HolgerZ

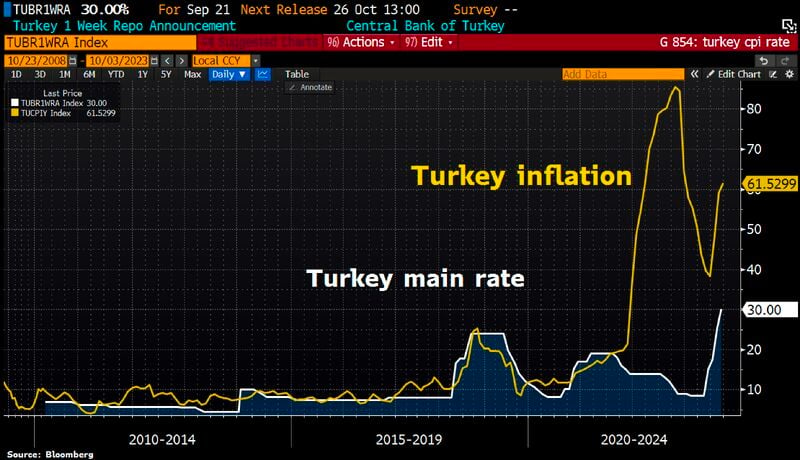

Turkey’s Inflation tops 60% despite massive interest rate hikes as oil surge worsens outlook

Source: HolgerZ, Bloomberg

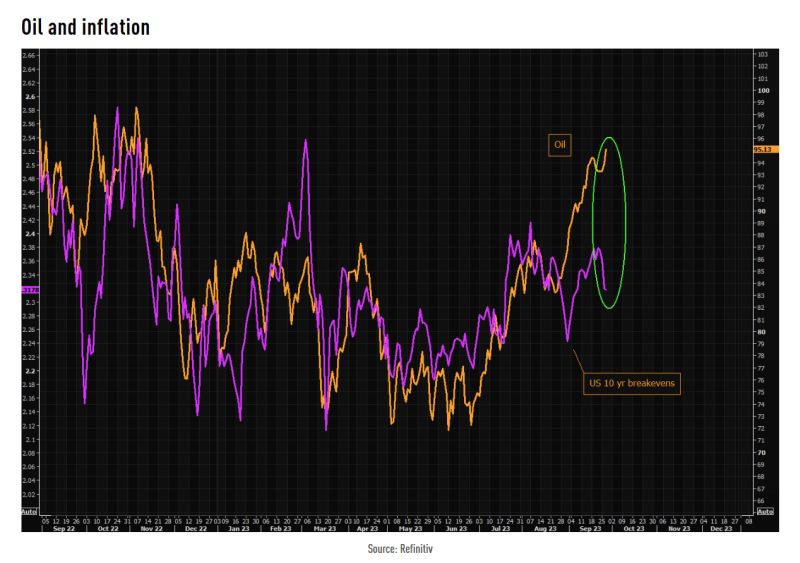

The gap between oil and 10 year breakevens is huge...

Does it mean that the market sees higher oil prices as a "growth killer" and thus disinflationary at some stage? Source chart: TME, Refinitiv

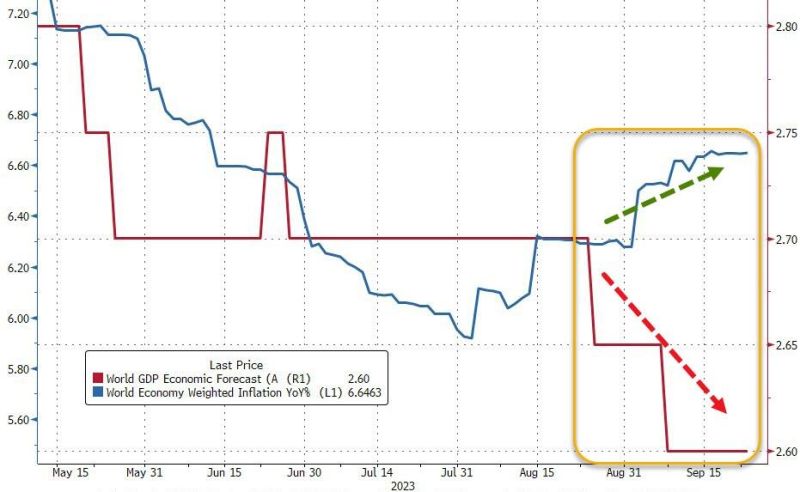

This chart explains by itself why the market mood has been deteriorating over the last few weeks:

Growth forecasts moving down / world inflation going up. What else? Source: www.zerohedge.com, Bloomberg

Inflation fear is NOT the driver of rising yields

Indeed, 10y real yields (10y nominal yields - 10y inflation expectations) jumped to 2.11%, the highest since 2009. In other words, investors are demanding higher REAL yields in the face of political chaos in Washington and high debt. Source: Bloomberg, HolgerZ

Turkey CenBank raised main interest rate to 30% from 25%, but w/inflation at ~60%, real rates are still very heavily negative

The hike continues what many see as a return to more orthodox monetary policy under Governor Hafize Gaye Erkan, a former executive of First Republic Bank & Goldman Sachs, who was appointed in June after President Recep Tayyip Erdogan won a close-fought re-election. Erkan now hiked rates by a cumulative 2150bps. Source: Bloomberg, HolgerZ

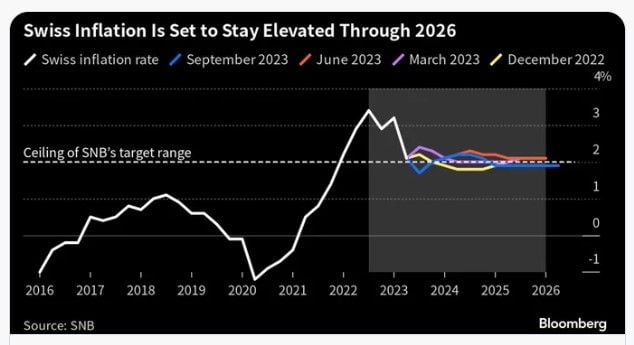

The Swiss National Bank pauses its monetary tightening, defying expectations of another interest-rate hike to avoid adding constriction on a stalled economy

- The SNB left today its key rate unchanged at 1.75%, debunking market expectations of an additional 25bp hike - The slowdown in inflation, the magnitude of the monetary policy tightening already implemented (CHF short term rates were still negative a year ago) and rising risks surrounding the global outlook underpin this decision. - Indeed, as inflation is within the SNB target (1.6%, in the 0%-to-2% target), economic activity is slowing down (0% GDP growth in Q2 2023) and the Swiss franc remains firm, the case for further tightening had turned much less compelling in the past few weeks. Unlike the ECB, forced to hike last week due to an inflation rate still much above its target, the SNB had very good reasons to pause today and adopt a cautious stance. - The SNB doesn’t rule out additional hikes in the future if warranted, but the combination of slowing growth in Europe (likely to dampen underlying price pressures) and of the strength of the currency are highly likely, in our view, to keep Swiss inflation dynamics in check in the months ahead.

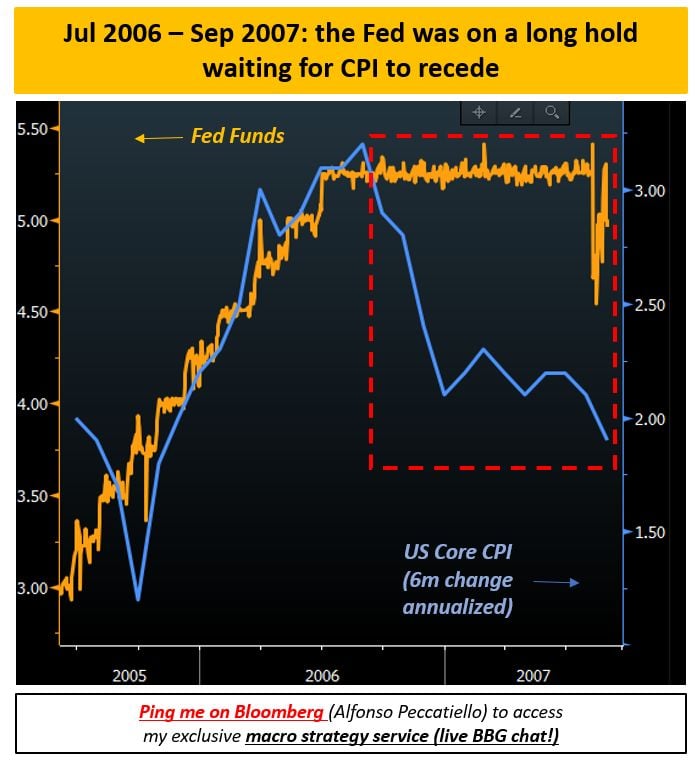

Can be the second half of 2007 be a good parallel for today's market?

As highlighted by MacroAlf, back in 2007, the FED kept rates at 5.25% (orange) despite core inflation was trending around 2% (blue) for quarters already. That ''higher for longer'' stubborness kept policy unnecessarily tight - as we figured out in 2008... Source: Alfonso Peccatiello