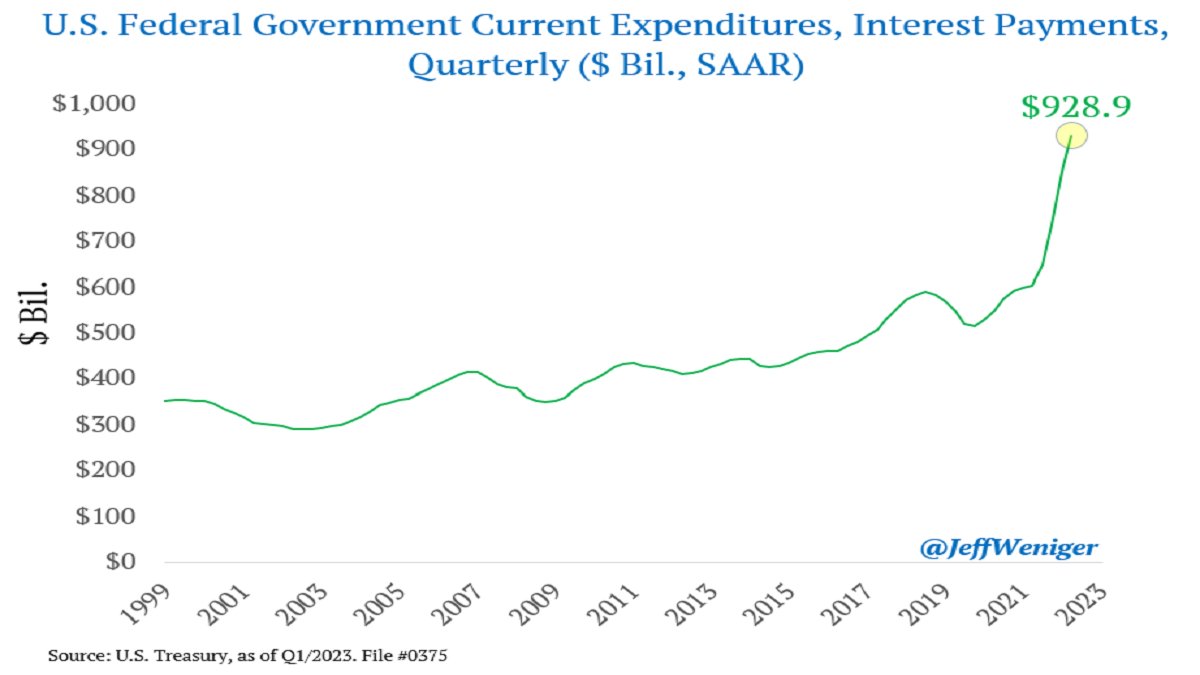

The U.S. government's interest expense is now an annualized $928.9 billion

Source: Jeff Weniger

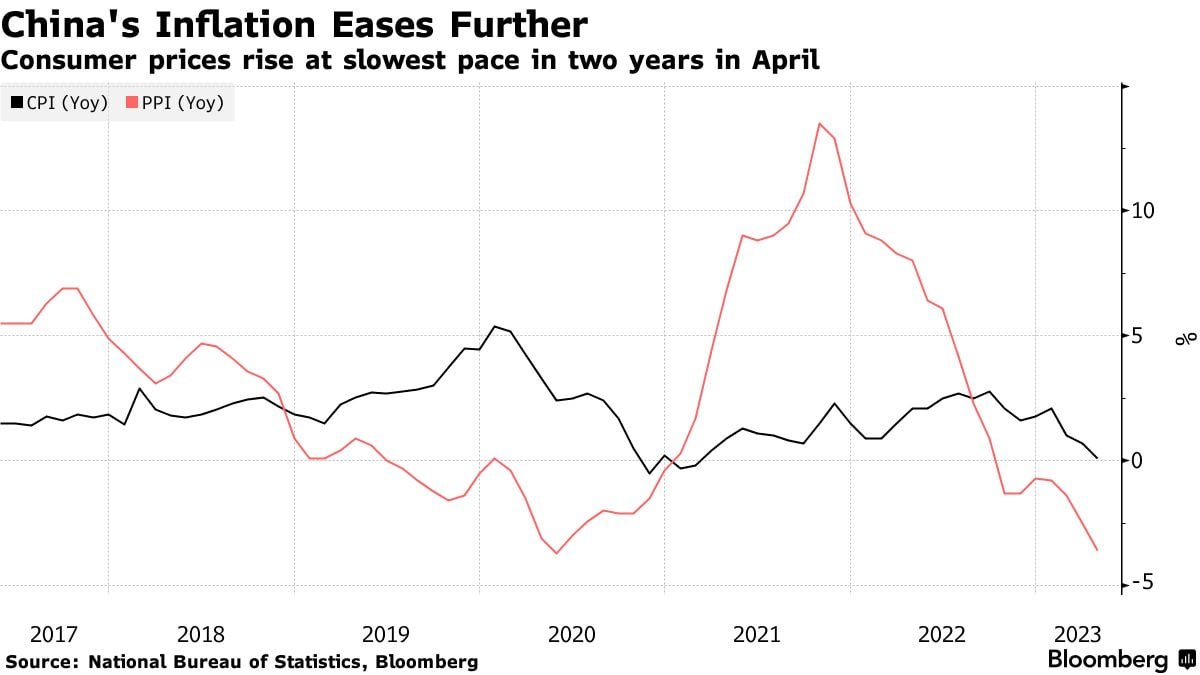

China Inflation Weakens to 2-Year Low on Uneven Recovery

China’s consumer inflation slowed to the weakest pace in two years in April while producer prices fell further into deflation, fueling debate about whether more policy stimulus is needed. The consumer price index rose 0.1% last month from a year earlier, the National Bureau of Statistics said Thursday, reflecting muted domestic demand as well as base effects from last April’s Shanghai lockdown. Core CPI, which excludes volatile food and energy costs, was unchanged at 0.7%. Producer prices fell 3.6% in April as commodity costs softened. The figure was more than March’s drop and deeper than economists had expected. Source: Bloomberg

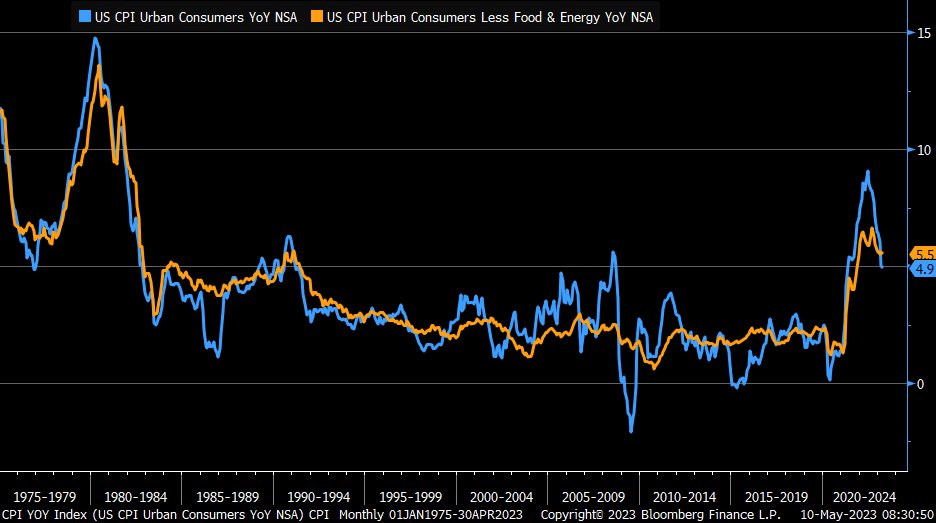

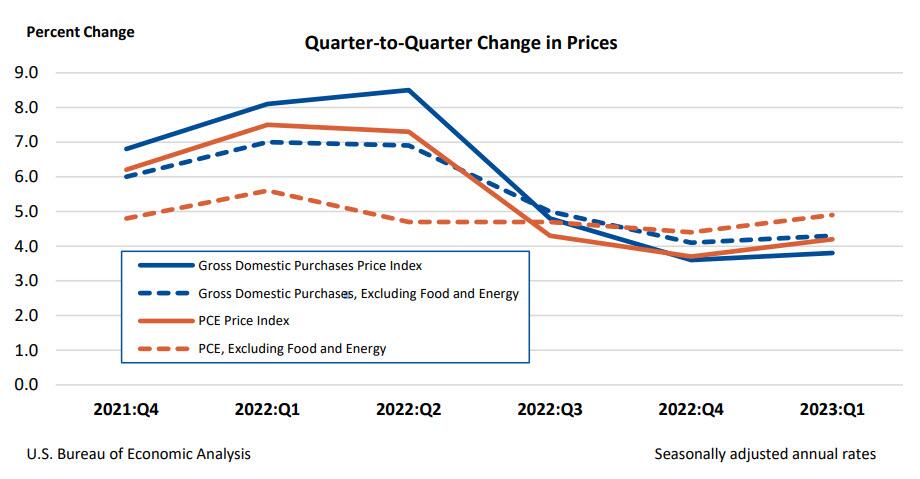

US inflation continues to cool down

US April CPI inflation +4.9% year/year vs. +5% estiated & +5% in prior month … Core CPI +5.5% year/year vs. +5.5% est. & +5.6% prior

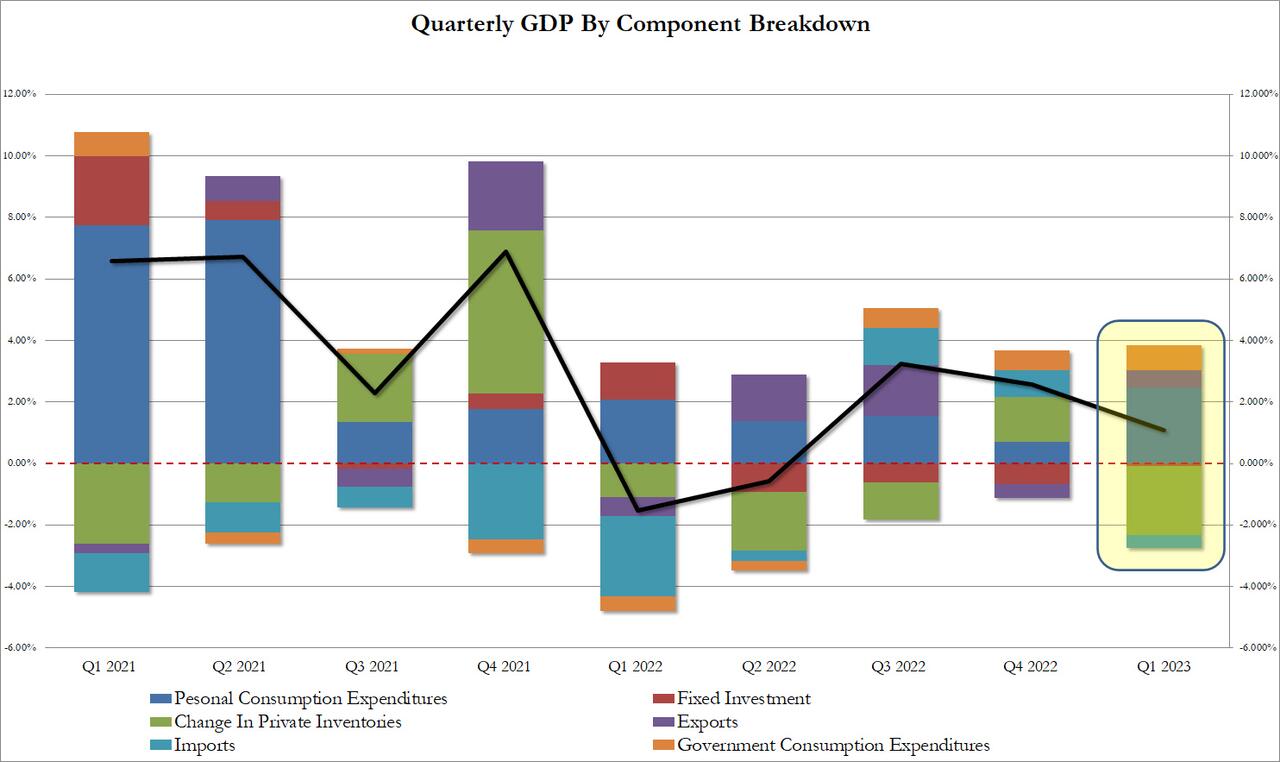

US real GDP rose just 1.1%, a big drop from the 2.6% GDP in Q4 and lower than estimates (1.9%)

It was the lowest GDP print since Q2 2022 when growth was negative to the tune of -0.6%... Personal Consumption added 2.48%, up from 0.70% in Q4. Fixed Investment subtracted -0.07%. The big hit was the change in private inventories, which subtracted 2.26% from the GDP print. Net exports were a modest contributor to GDP, adding 0.11%. Government consumption added another 0.81% to the bottom line number, effectively contributing more than 70% of the final print. Source: Bloomberg, www.zerohedge.com

Why are US bond yields moving higher despite GDP growth miss? US Q1 Core PCE is higher than expected

While US GDP Q1 growth rate came in well below expectations, PCE and core PCE prints were unexpectedly hot, the former coming in at 4.0% above the 3.7% expected and higher than the 3.9% in Q4, while core PCE came in at 4.9%, well above the 4.4% in Q4 and also hotter than the 4.7% expected. In fact, as shown below, this was the 5th consecutive "beat" of median core PCE expectations.

Germany will go from being a net exporter of electricity to a net importer of electricity in Europe

Germany will go from being a net exporter of electricity to a net importer of electricity in Europe after the nuclear power plants are shut down. Last week, electricity imports reached their highest level in one day since 2021. Source: HolgerZ, Bloomberg

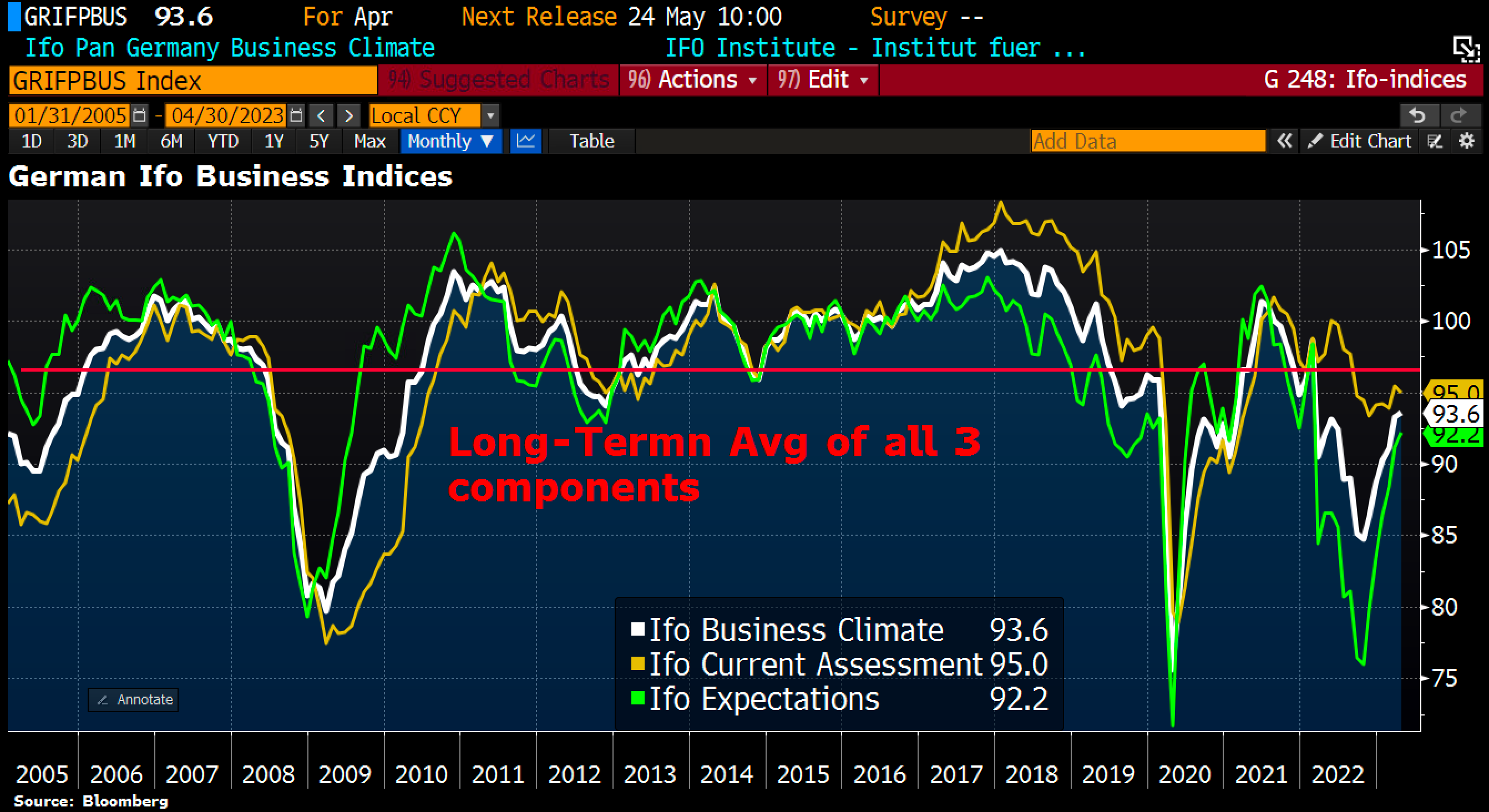

Ifo expectations index came out way better than expected

German Ifo Business Climate Index improves to 93.6 in April from a revised 93.2 in March. Ifo current assessment index fell to 95 (vs 96 exp. from 95.4 in March. BUT Ifo expectations index improves to 92.2 for the 6th month in a row from a revised 91.0 in March & way above 91.1 expected. Source: Bloomberg, HolgerZ

Houston we have a problem...

While equity markets seem complacent about the imminent debt ceiling crisis, the same can not be said of the rates market, where the "kink" in T-bills maturing around the X-date is turning spectacular... Bottom-line: The spread between 3-month (5.12%) and 1-month (3.40%) Treasury yields has never been higher: 1.72%. Indeed, the yield on US T-Bill which mature BEFORE June is much lower than it should be given the current level of the Fed Funds rate: below 4% vs. a Fed Funds rate already close to 5%. This premium is probably related to the fact that, for T-Bill maturing before the end of May, there is no uncertainty related to the debt ceiling, since the US Treasury will have the cash needed to meet principal redemptions. But from June onwards, the risk of the debt ceiling being hit increases; this triggers a jump in yield with T-bill yielding roughly the same than Fed Funds. Source chart: Charlie Bilello