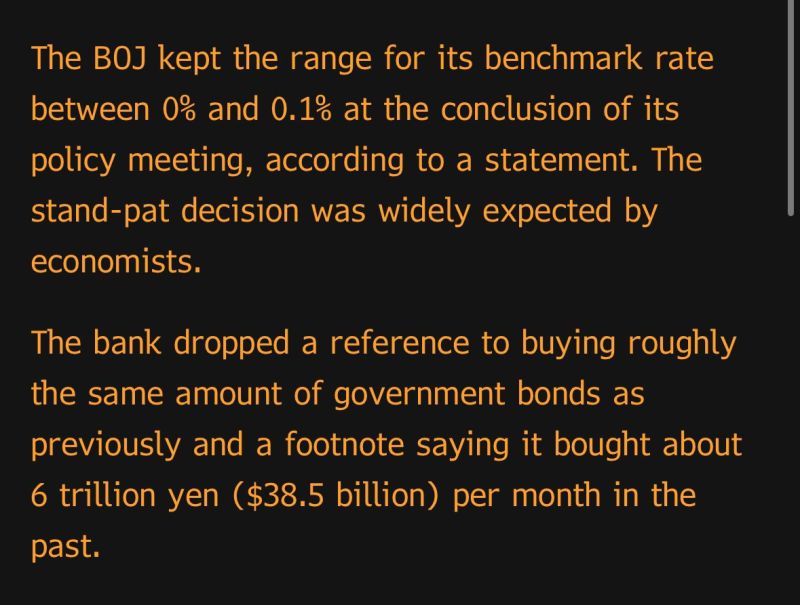

Bloomberg on the outcome of the BoJ Bank of Japan’s monetary policy meeting.

The Bank of Japan kept its policy rate unchanged Friday after its monetary policy meeting, holding its benchmark policy rate at 0%-0.1%. This is in line with expectations from economists polled by Reuters. While the move was expected, this comes after Tokyo’s April inflation came in lower than expected, with the core inflation rate at 1.6% compared to expectations of 2.2% from Reuters. The BOJ also said it will continue to conduct bond purchases. However, they dropped a reference to buying roughly the same amount of bonds as previously. No comment was made by the BOJ on the yen, which has steadily weakened since the BOJ ended its negative interest rate policy last month and abolished its yield curve control policy. The currency broke through the 156 mark against the U.S. dollar Friday after the decision, most recently trading at 156.11. Separately, the central bank also released its second-quarter outlook for Japan’s economy, raising its outlook for inflation in fiscal 2024. The BOJ now expects inflation between 2.5% and 3% for fiscal 2024, up from 2.2% to 2.5% in its January forecast. Inflation is then predicted to decelerate to “around 2%” in fiscal 2025 and 2026, the bank added. The BOJ also downgraded gross domestic product growth forecasts for fiscal 2024 to a range of 0.7% to 1%, down from January’s prediction of 1%-1.2% growth. Think of this as another small step in what the BoJ sees as a relatively long policy normalization journey. As mentioned by Mohamed El Erian, the length of this journey, both on a standalone basis and relative to the US, helps explain the weak Yen. Source: Bloomberg, CNBC

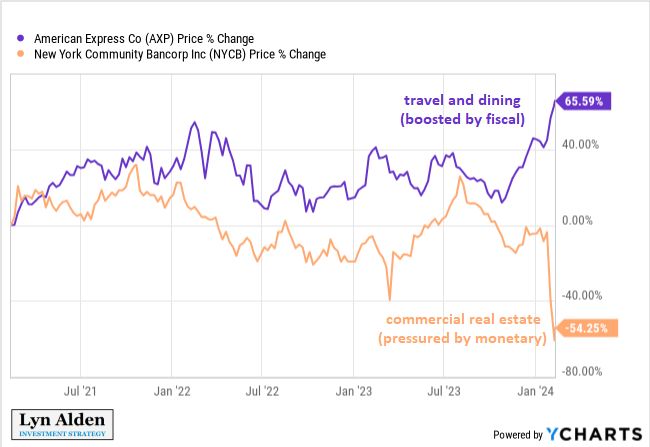

Great comment by Lyn Alden about the impact "FISCAL DOMINANCE" on sector performance divergence...

Bottom-line: go LONG Fiscal deficits receivers and go SHORT Fiscal deficit payers (i.e interest-rate sensitive sectors) "The wider-than-normal divergence between loose fiscal policy (which is stimulating) and tight monetary policy (which slows things down) contributes to wider-than-normal divergence between the performance of different economic sectors. It results in a wider-than-normal gap between sectors that are directly or indirectly on the receiving side of the deficits (eg business that rely on spending from upper and upper-middle class spenders) vs those that are the most sensitive to interest rates and thus are the most hurt by tight monetary policy (eg commercial real estate). And because some sectors of the economy are doing great partially due to the fiscal stimulus, it makes it unlikely that monetary policy or other assistance will arrive to the weaker areas any time soon. And ironically, because public debt levels are high, tight monetary policy *contributes* to looser fiscal policy by increasing the overall interest expense of the government, which goes to various entities in the economy and strengthens some of the sectors that are not sensitive to interest rates. This is a condition known as fiscal dominance". Lyn Alden