JACKSON HOLE: A RISK MANAGEMENT SPEECH

FACTS: The overall tone of Chair Powell’s Jackson Hole speech was relatively hawkish but not as hawkish as some feared on the back of recent strong data. It was also less hawkish than last year. The main message is that The Fed is definitely on hold but leaning on a more hawkish stance should data don’t show more progress in inflation / growth cooling down. OUR TAKE: The big event is now behind us, and we didn’t learn anything new. Powell believes that monetary policy is tight, but he opens the door to an even tighter one. With regards to macro data, they are going into the right direction but there is a risk of further upside, i.e interest rates path remains very data dependent which means that markets will now turn its attention to PCE inflation and US jobs data (next week). The Fed is likely to stay nervous as long as they see evidence of a serious break in job growth below the 200K pace. We are not there yet, which means that in the coming weeks, we will likely see macro volatility leading to market volatility. Our view remains that central bankers want first and foremost to avoid the big mistake (rather than targeting a pre-defined target). In the previous decade, central bankers wanted to avoid the deflation trap, hence the over-printing. This time, they want to avoid the risk of another round of inflation. Hence the temptation of over-tightening. MARKET REACTION: Rate-hike expectations initially moved lower but then reverted higher after investors actually read and listened to his speech. 2Y yields are back to July highs and equity markets are whipsawing.

Going into Jackson Hole, the probability of a September hike is just 20%, well below 50%, so not likely. But, as shown below, the probability of a hike in November (see below) is now 50/50

What will it be when Jay is done? Source: Jim Bianco

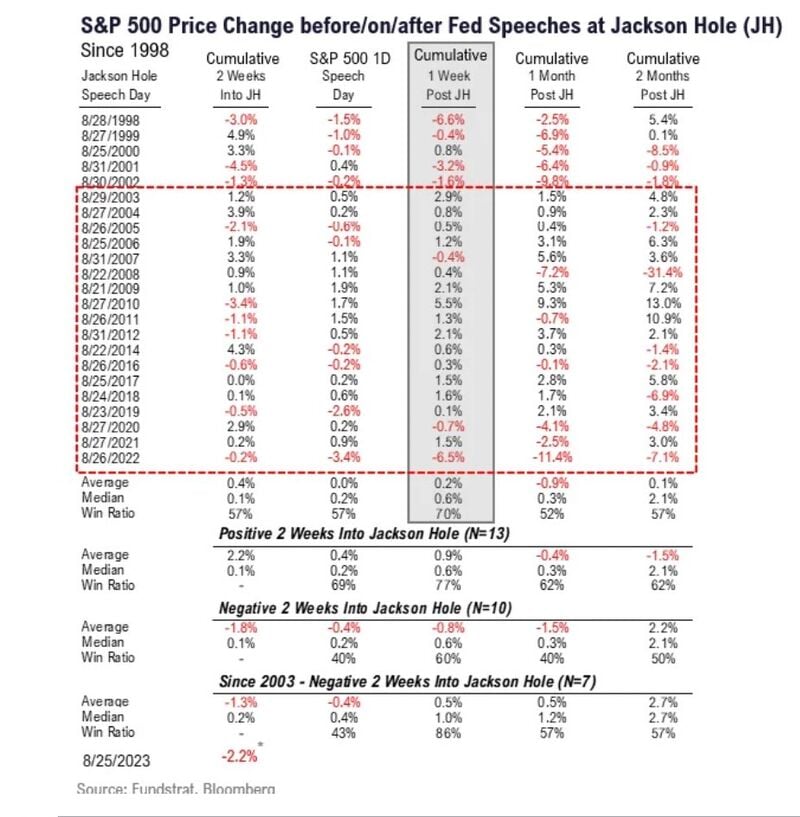

Price changes before/on/after FED speeches at Jackson hole " since 2003, there are 7 instances $SPX down 2 weeks prior to #JacksonHole .. 6 of 7 instances, equities rose in the week post-JH ..”

Source: Fund Strat thru Carl Quintanilla

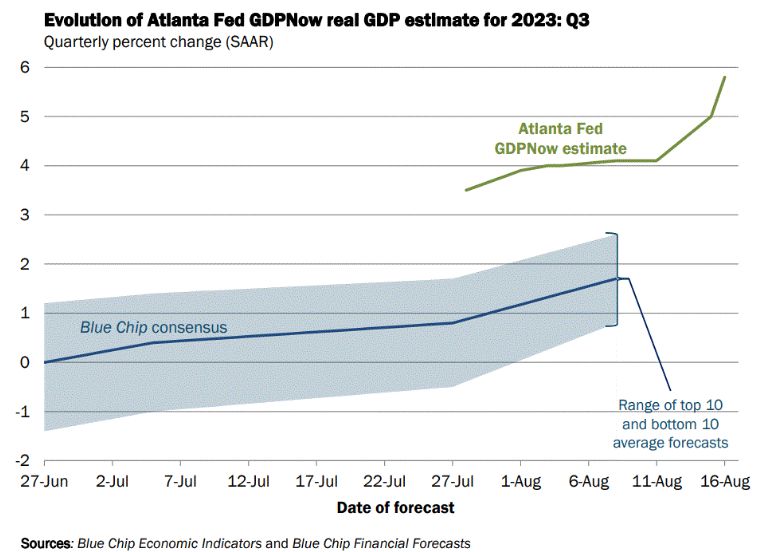

Ahead of Jackson Hole this week, Atlanta Fed GDP Now for US real GDP in 3Q is at 5.8%...

Way ahead of Street consensus and with a clear acceleration since early August...

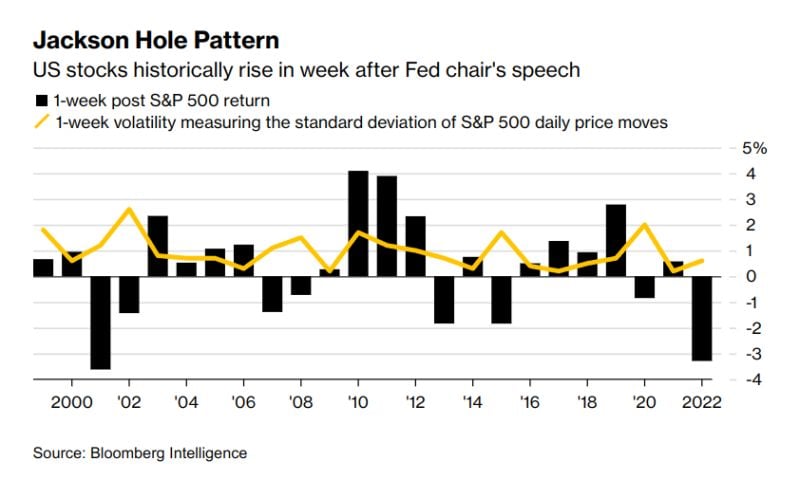

More often than not, stocks rise the week after Jackson Hole Will this year follow the pattern, or will it be one of the outlier years with a sell-off?

Source: Markets & Mayhem, Bloomberg

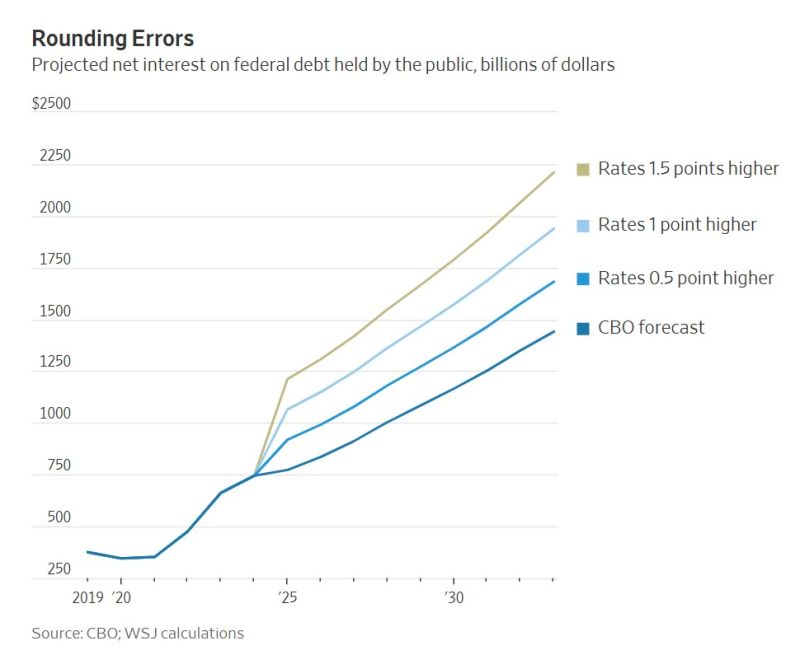

Very interesting WSJ article: "The Scary Math Behind the World’s Safest Assets. Washington has laid the seeds of a crisis that Wall Street can no longer ignore"

Here's an extract: "Consider that around three-quarters of Treasuries must be rolled over within five years. Say you added just 1 percentage point to the average interest rate in the CBO’s forecast and kept every other number unchanged. That would result in an additional $3.5 trillion in federal debt by 2033. The government’s annual interest bill alone would then be about $2 trillion. For perspective, individual income taxes are set to bring in only $2.5 trillion this year. Compound interest has a way of quickly making a bad situation worse—the sort of vicious spiral that has caused investors to flee countries such as Argentina and Russia. Having the world’s reserve currency and a printing press that allows it to never actually default makes America’s situation far better, though not consequence-free. Just letting rates rise high enough to attract more and more of the world’s savings might work for a while, but not without crushing the stock and housing markets. Or the Fed could step in and buy enough bonds to lower rates, rekindling inflation and depressing real returns on bonds".

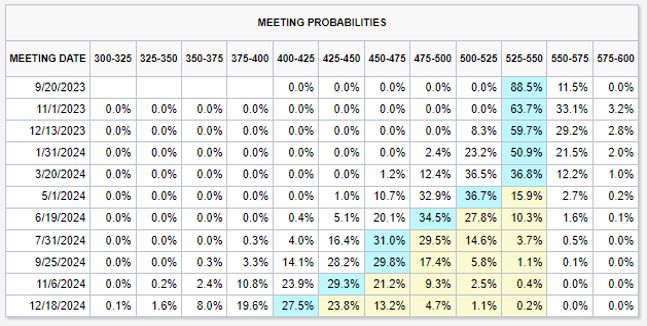

What are the latest moves when it comes to market expectations on Fed rates ?

A Fed HIKE of 25 bps by NOVEMBER moved from 30% to 33%. It is still below 50%. So not priced in. But a 3% increase (30% to 33%) is the biggest up move in a month. Furthermore, odds of rate CUTS are dropping. Markets now do not see any rate cuts until May 2024 in the base case. 3 months ago, markets expected 4 rate cuts in 2023. Markets seem to be bracing for a long Fed "pause." Source: The Kobeissi Letter, Bianco Research

Fed QT accelerates. Fed balance sheet shrank $91bn in July, -$759bn from peak, biggest drop ever to $8.2tn, lowest level since July 2021

Fed has now shed 22.3% of the Treasury securities it bought during pandemic QE. Fed's total assets now equal to 30.6% of US's GDP vs ECB's 53%, BoJ's 130%. Source: HolgerZ, wolfstreet.com